TODAY’S S&P 500 SET-UP – July 3, 2014

As we look at today's setup for the S&P 500, the range is 29 points or 1.35% downside to 1948 and 0.12% upside to 1977.

SECTOR PERFORMANCE

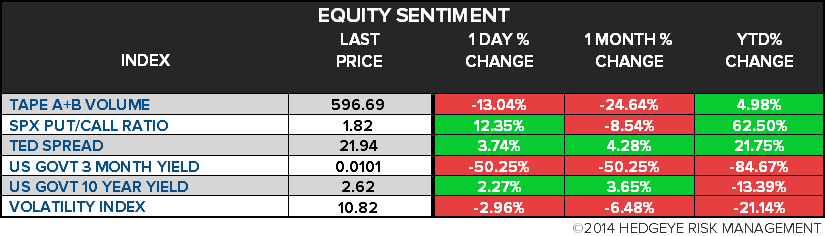

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.14 from 2.16

- VIX closed at 10.82 1 day percent change of -2.96%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Initial Jobless Claims, June 28, est. 313k (prior 312k)

- Continuing Claims, June 21, est. 2.560m (prior 2.571m)

- 9:45am: Bloomberg Consumer Comfort, June 29 (prior 37.1)

- 9:45am: Markit US Services PMI, June final, est. 61 (prior 61.2)

- Markit US Composite PMI, June final (prior 61.1)

- 10am: ISM Non-Manufacturing Composite, June., est. 56.3 (prior 56.3)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 1pm: Baker Hughes rig count

GOVERNMENT:

- House, Senate on recess until July 8

- 6am: Quinnipiac releases public opinion survey of Iraq troops, background

- checks for gun purchasers, stricter gun laws

- 12:30pm: Transportation Secretary Anthony Foxx, holds news conf. with Gov.

- Lincoln Chafee, D-R.I., on Highway Trust Fund

- U.S. ELECTION WRAP: Incumbency Worth $500k

WHAT TO WATCH:

- ECB watchers seek Draghi illumination on path from low rates

- Obama decries trader bonus system as risky even after Dodd-Frank

- Arthur becomes hurricane off U.S. East Coast

- VW rejects comments by Daimler’s Bernhard of possible Paccar bid

- U.K. services employment rises at record pace as demand jumps

- Ackman’s Pershing Square fund Is said to gain 25% in 1H

- Occidental talks for Middle East unit stake sale said to falter

- Dimon’s cancer has 90% cure rate with demanding therapy

- Amazon plans to fight FTC over unauthorized mobile-app purchases

- ‘Transformers’ shows worldwide appeal with China outdrawing U.S.

- Siemens CEO chasing U.S. gas boom has ‘firepower’ for deals

- Qualcomm buys Wilocity to step up challenge to Broadcom in Wi-Fi

- Tesla approved by Pennsylvania assembly to add company stores

- Salesforce considers acquisitions in Germany to spur growth

- U.S. equity markets close 1pm ahead of July 4 holiday

EARNINGS:

- International Speedway (ISCA) 7:30am, $0.48

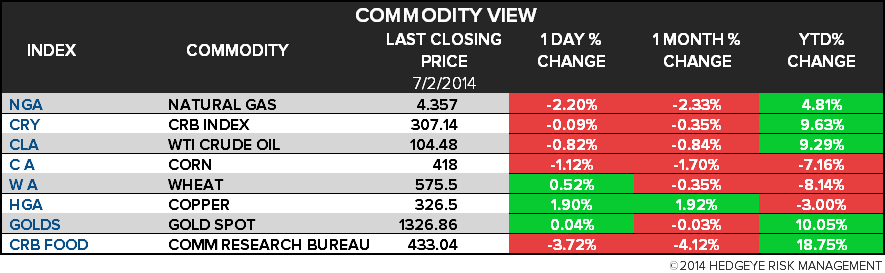

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Chinese Trader Said to Pledge Metals Three Times Over for Loans

- World Food Prices Fall for Third Month as Grains Lead Decline

- Cotton Boom Goes Bust as Texas Rains Revive Surplus: Commodities

- Libya Reopening Two Oil Ports After Taking Control From Rebels

- Arthur Strengthens to Become First Atlantic-Season Hurricane

- Gold Retreats From Three-Month High Before U.S. Payrolls Report

- Nickel Climbs to Highest Since May as U.S. Data Boosts Demand

- Steel Rebar Falls From 1-Week High on Chinese Mills Supply Glut

- Palm Oil Declines as Drop in Crude May Ease Demand for Biodiesel

- Coffee Gains for Second Session; Sugar Drops as Surplus Raised

- Sugar Millers in Thailand Urge Market Prices to Avoid Smuggling

- Rupture-Prone Oil Trains Keep Rolling a Year After Quebec Crash

- Conditions Not ‘Ripe’ to Decide Weda Bay Project in ’14: Eramet

- Corn Nears Bear Market on Outlook for Biggest Ever U.S. Harvest

CURRENCIES

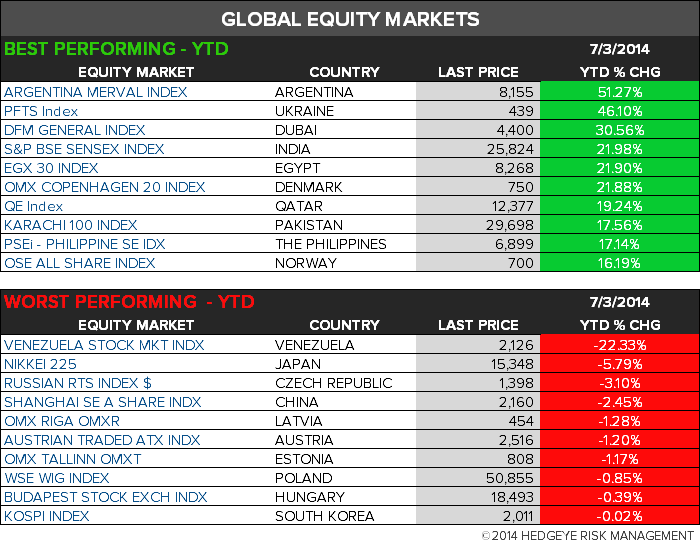

GLOBAL PERFORMANCE

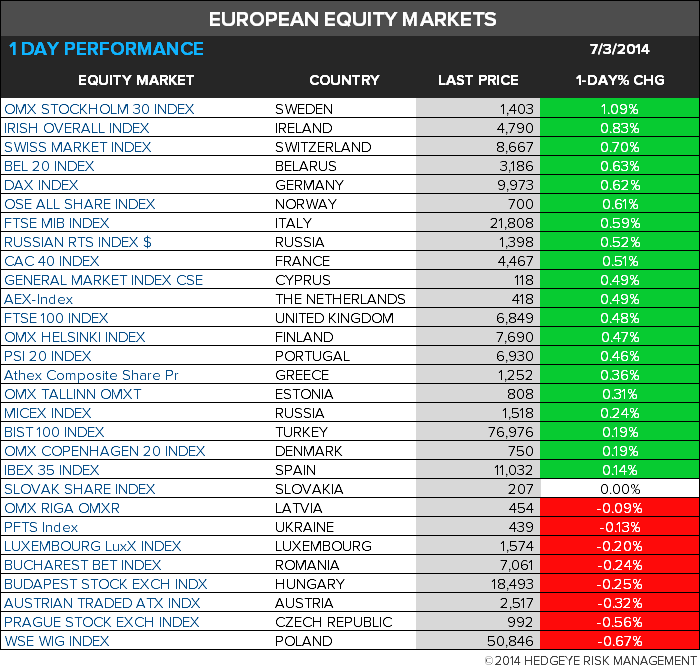

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team