Research Edge Portfolio Position: Long Chinese equities via CAF

July Trade and Industrial Output data released last evening by national Bureau of Statistics disappointed some observers looking for continued sequential year-over-year improvement spurred by the massive stimulus injection earlier this year. On the news, the Chinese equity market closed higher on the day for the 1st day in the last 5.

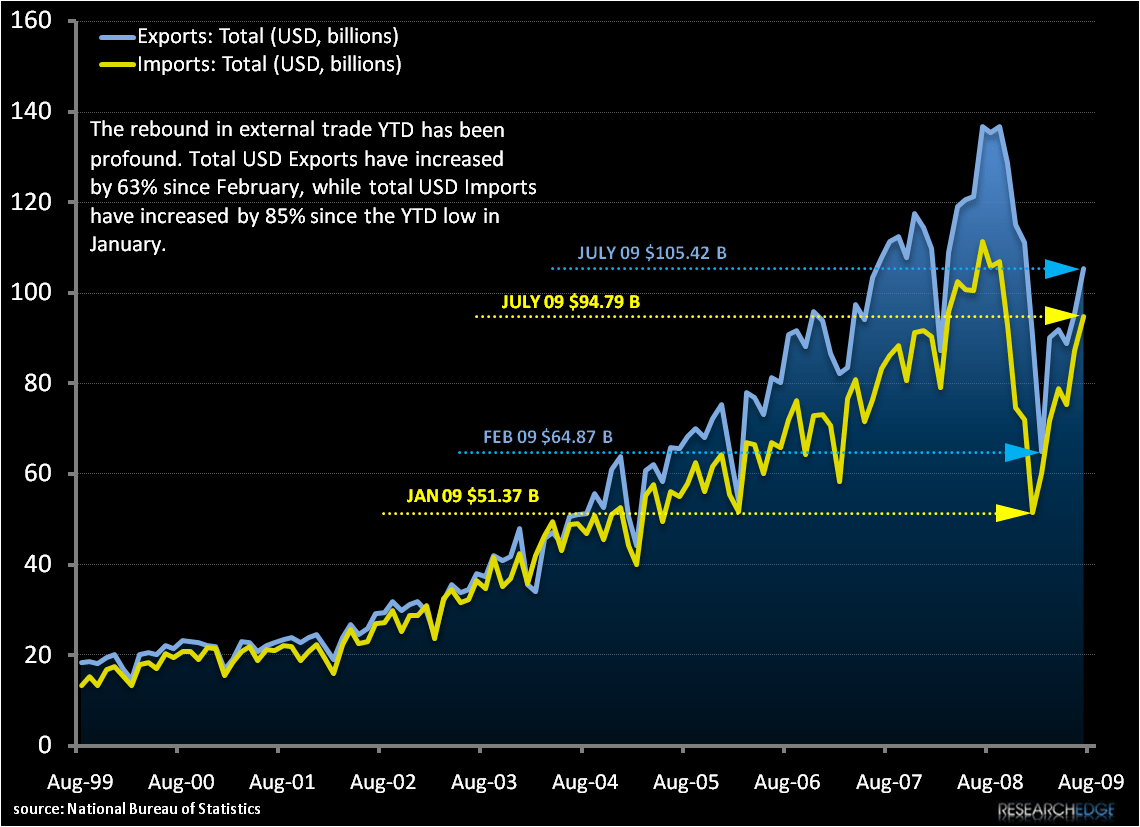

On a year-over-year basis, July trade data is mildly disappointing, but should be taken in context. For starters, viewing last month’s figures this way creates obvious distortion since it is a comparison against the final frantic month of activity last summer before the massive disruption of the Olympic Games in Beijing. Viewed on an absolute basis however, the actual trajectory and power of the rebound since the beginning of the year remains arresting (see chart below).

(discussion continued after chart)

Although Industrial Output data for July registered at a respectable 10.8% Y/Y, the third consecutive month of acceleration, the glass half empty crowd looking for signs of fatigue in the recovery cycle may attempt to find one in this number since the rate of sequential improvement appears to be moderating. We do not subscribe to this view. The data shows continues strength, with heavy industry and domestic demand driven components like automotive continuing to expand at double digit Y/Y rates.

We continue to be positive on China’s economic recovery cycle, with focused stimulus programs driving internal demand in the near term while developing broader consumer demand patterns for the long term. This will not completely offset lost external demand, nor will it happen fast or smooth: China is a poor nation in many ways and has a consumer base still in an early developmental stage and, as such, it would be absurd to think that the emergency measures enacted in late 2008 by the government there will return the patient to full health with no side effects or recuperation time.

What we do believe however is that all data continues to suggest that the operation has been a major success and the patient is well on the way to recovery. We remain focused on the negative impact of monetary loosening on asset valuation and other risk factors, but for now the data continues to provide us with confidence on our thesis on the recovery and development of the real economy.

We bought more CAF on a red tape today as some investors flee because the news is merely great and not perfect.

Andrew Barber

Director