TODAY’S S&P 500 SET-UP – June 30, 2014

As we look at today's setup for the S&P 500, the range is 25 points or 0.86% downside to 1944 and 0.41% upside to 1969.

SECTOR PERFORMANCE

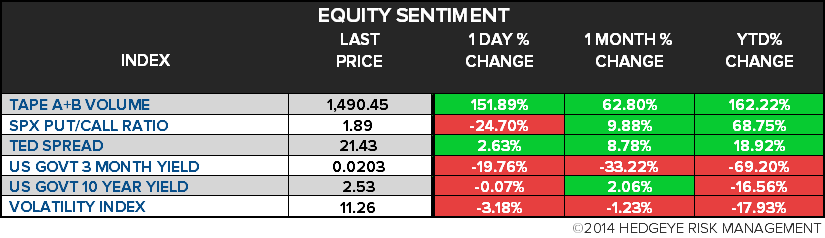

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.06 from 2.07

- VIX closed at 11.26 1 day percent change of -3.18%

MACRO DATA POINTS (Bloomberg Estimates):

- 9am: ISM Milwaukee, June est. 60.0 (prior 63.49)

- 9:45am: Chicago Purch. Mgr Index, June., est. 63 (prior 65.5)

- 10am: Pending Home Sales m/m, May, est. 1.2% (prior 0.4%)

- 10:30am: Dallas Fed Mfg Activity, June., est. 10.0 (prior 8.0)

- Noon: USDA quarterly grain inventories

- 1:10pm: Fed’s Williams speaks in Sun Valley, Idaho

GOVERNMENT:

- President Obama welcomes Chilean president Michelle Bachelet to White House

- House, Senate on recess until July 8

- 10am: Supreme Court issues last decisions of term; likely to hand down decision on Hobby Lobby case

- 10am: Kenneth Feinberg, a victims compensation lawyer hired by General Motors, holds news conf. on details of program to compensate victims or family members of victims killed in accidents connected to faulty ignition switch that prompted recall of 26m vehicles

WHAT TO WATCH:

- BNP dollar-clearing ban said to start in 2015 as plea looms

- ‘Transformers’ debut of $100m sets high mark for 2014

- Aereo halts service after Supreme Court loss to broadcasters

- Al-Qaeda offshoot declares Islamic caliphate as Iraq fights back

- Tencent to buy $736m stake in Craigslist-like 58.com

- Japan output rebounds in sign companies enduring tax rise

- Hollande, Merkel urge Ukraine talks to Putin, Poroshenko

- Former P&G CEO McDonald is Obama’s pick to head Veterans Affairs

- American Apparel adopts stockholder rights plan

- GM compensation fund details to be released

- Caesars vies w/ Genting as bids due for N.Y. casino licenses

EARNINGS:

- No earnings expected from S&P 500 cos.

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Daily Iron Ore Mine Closures in China Mean Citigroup Is Bullish

- Brent Pares Biggest Monthly Gain Since August on Iraq; WTI Falls

- Wheat Bears Multiply as Prices Slump Most Since ’11: Commodities

- Rebar Posts Longest Quarterly Slump Since 2011 on Ore, Property

- Tin Seen Rising 21% by ICDX as Indonesian Exports Reach 8-Yr Low

- Palm Oil Posts Biggest Quarterly Decline Since September 2012

- Gold Holds Below 2-Month High as Prices Head for Quarterly Gain

- Hedge Funds Boost Gasoline Bets as July 4 Holiday Nears: Energy

- China Iron Ore Port Inventory Falls From Record: Steelhome

- Japan Refiners May Cut Capacity to Meet New Efficiency Rules

- Zinc-to-Lead Balance Flips by Most Since 2010: Chart of the Day

- Second Asia-Bound VLCC Since April Heads for Hound Point: Track

- ARA Gasoil Stockpiles Hold at Record for Fourth Week: Genscape

- Chinese Steel Mill Protesters Lay on Rail Tracks as Pays Frozen

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team