TODAY’S S&P 500 SET-UP – June 24, 2014

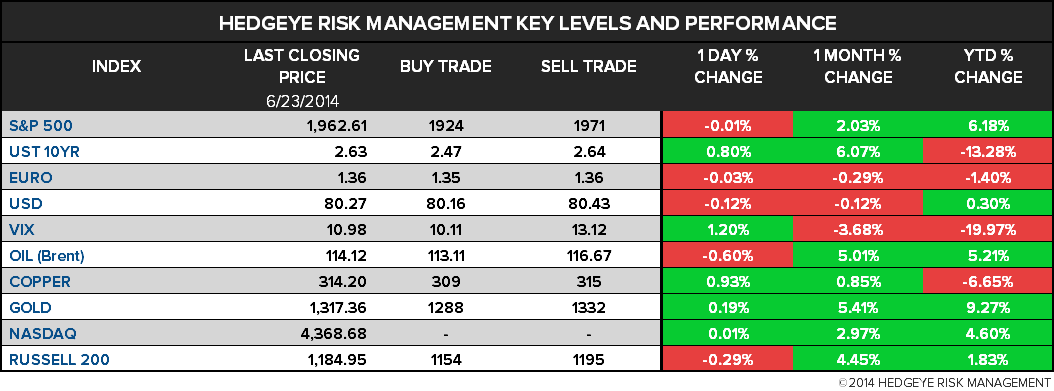

As we look at today's setup for the S&P 500, the range is 47 points or 1.97% downside to 1924 and 0.43% upside to 1971.

SECTOR PERFORMANCE

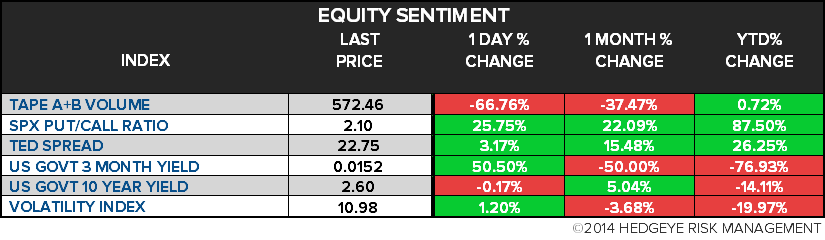

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.15 from 2.16

- VIX closed at 10.98 1 day percent change of 1.20%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:05am: Fed’s Plosser speaks in New York

- 8:55am: Redbook weekly sales

- 9am: FHFA House Price Index, April, est. 0.5% (prior 0.7%)

- 9am: S&P/Case-Shiller 20 City m/m, April, est. 0.8% (prior 1.24%)

- 10am: Consumer Confidence Index, June, est. 83.5 (prior 83)

- 10am: Richmond Fed Manufacturing Index, June, est. 7 (prior 7)

- 10am: New Home Sales, May, est. 439k (prior 433k)

- New Home Sales, m/m, May, est. 1.4% (prior 6.4%)

- 2pm: Fed’s Dudley speaks in New York

- 4:30pm: API weekly oil inventories

- 6:30pm: Fed’s Williams speaks in Stanford, Calif.

GOVERNMENT:

- Primaries held in N.Y., Colo., Md., Okla., Utah; Miss. GOP runoff between Sen. Thad Cochran, state Sen. Chris McDaniel

- 9:30am: House Oversight Cmte hearing on IRS’s missing e-mails

- 10am: Senate Appros subcmte marks FY15 Homeland Security bill, then at 11am FY15 fin svcs, general govt spending bill

- 10am: Senate Finance Cmte examines how tax code can be leveraged to reduce student debt

- 2pm: Senate-House conf. cmte on veterans’ health-care bill

- *U.S. ELECTION WRAP: Primaries to Watch; Sen. Warren for Tennant

WHAT TO WATCH:

- German IFO business confidence drops more than est.

- Iraq forces regain control of Baiji refinery

- Kerry lands in Erbil to urge Iraqi Kurds to help form govt

- AT&T CEO to tell Congress DirecTV takeover means lower prices

- Merkel expects tough sanctions on Russia from EU summit: Bild

- Gazprom says Europe gas shipments via Ukraine uninterrupted

- Targa said to abandon sale to Energy Transfer after share spike

- Apple’s larger iPhones said to start mass output next month

- Lew defends council’s work to guard against U.S. financial risk

- KKR pays $567m for stake in Acciona’s foreign renewables

- NYC rent board sets 1% apartment-rate rise as freeze rejected

- Ex-Goldman currency trader Cho said to start macro hedge fund

EARNINGS:

- AGF Management (AGF/B CN) 8:00am, C$0.18

- Apogee Enterprises (APOG) 4:30pm, $0.26

- Carnival (CCL) 9:15am, $0.02

- Walgreen (WAG) 7:30am, $0.94 - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Climbs to Two-Month High on Iraq to U.S. Economy Outlook

- Brent Trades Near One-Week Low as Iraq Supply Stable; WTI Slips

- Gold Euphoria Won’t Last With Yellen’s Rally Fading: Commodities

- Copper Premium in Europe Said to Decline With Demand Slowing

- Nickel Reaches One-Week Low as Speculators Cut Bullish Wagers

- Raw Sugar Declines Before Brazil’s Unica Report; Cocoa Falls

- MORE: CME Sees Asia as ‘Right Market’ to Invest in Gold Products

- China Copper Bonded Stockpiles Seen by CRU Down to 775,000 Tons

- Crop Futures Decline as Report Shows U.S. Fields in Good Shape

- China Seen Bolstering Oil Security as Stockpiles Swell to Record

- Indonesia Seeks Tin-Export Rules to Avoid Inaccurate Declaration

- Rooftop Solar Leases Scaring Buyers When Homeowners Sell: Energy

- Congo’s Gecamines Needs $160 Million to Cut 6,000 Mining Jobs

- Platinum Union to Sign Deal With Producers to End 5-Month Strike

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team