Darden is due to report 4QF14 EPS tomorrow before the open and we’re confident that the news coming out of the quarter will be nothing short of a disaster.

With that in mind, we’d like to offer up some key thoughts:

- The 4QF14 consensus EPS estimate of $0.94 is $0.05 to $0.10 too high.

- The current FY15 consensus EPS estimate of $2.54 is $0.30 to $0.40 too high.

- The earnings implications are that the company will be unable to sustain its $2.20 dividend in FY15.

- There will be little, if any, legitimate visibility in regards to the attempted turnaround of the Olive Garden.

- Management will give guidance that will be too optimistic.

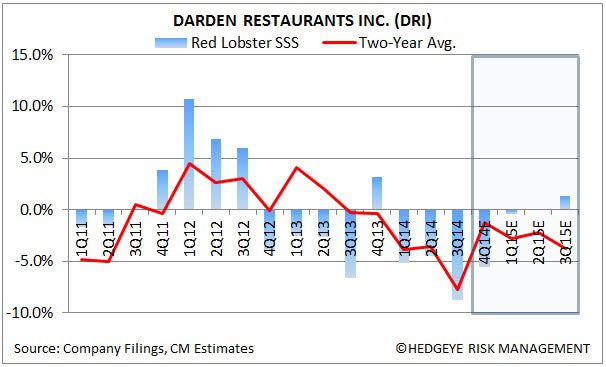

We suspect that very few analysts have updated the earnings power of the company to properly reflect the recent sale of Red Lobster to Golden Gate Capital for $2.1 billion ($1.6 billion net). Additionally, we believe that analysts are currently too optimistic about current trends and what the future holds for FY15. As we see it, changes to the Street’s models should include lower revenues, continued restaurant margin erosion, modest G&A reductions, lower interest expense and a lower share count from the use of proceeds.

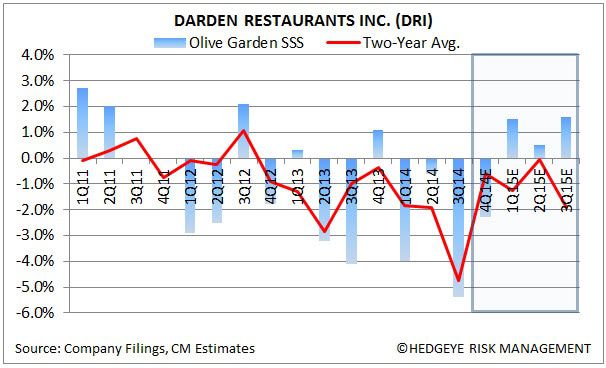

As you can see in the charts below, the Street generally believes that Olive Garden is fixed and should see improved trends next quarter. We’d note, however, that this has been the case for the last five years. As such, it has become typical to hear something along the lines of “Don’t worry; the turnaround at Olive Garden is just one quarter away!”

We’ve repeatedly stated our view that current management headlines the bear case for DRI as they continue to destroy shareholder value. Their actions during this past quarter simply reinforce our belief. While there is a core group of shareholders that are working diligently to correct the issues, there is little that can be done between now and the annual meeting.

In the short-run, we have little reason to believe the stock will outperform. Further out, we believe Darden’s cavalier attitude toward shareholders will result in wholesale changes at the company when the annual meeting comes around later this year.

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst