Our 1Q14 Macro Investment theme #InflationAccelerating called for ~100 bps increase in reported CPI into the easiest inflation comps in 3Q14. With inflation running just above 1% into 2013 year-end, a +100 bps increase was effectively a call for a doubling in the rate of price growth.

With the May reading of +2.13% YoY that doubling of inflation growth has largely manifest. What hasn’t accelerated, unfortunately, is earnings growth (more on that below).

Headline CPI accelerated for a 3rd consecutive month in May, hitting its highest rate of growth since October 2012, while Core CPI accelerated 20bps to +2.0% YoY.

Shelter inflation (~31% weight), which almost singularly supported the headline number most of the last year, accelerated +10bps to +2.9% YoY while protein (meat, poulty, fish, eggs) price growth accelerated another +130 bps sequentially to +7.7% YoY.

Notably, while shelter inflation has buttressed the headline number over the TTM and food/energy inflation have been the outliers YTD, the rise in prices has been increasingly broader based the last several months.

Indeed, the percentage of components registering sequential acceleration made a new multi-year high in May and is looking similar to the commodity price cycle catalyzed acceleration in 2011.

So, where to from here?

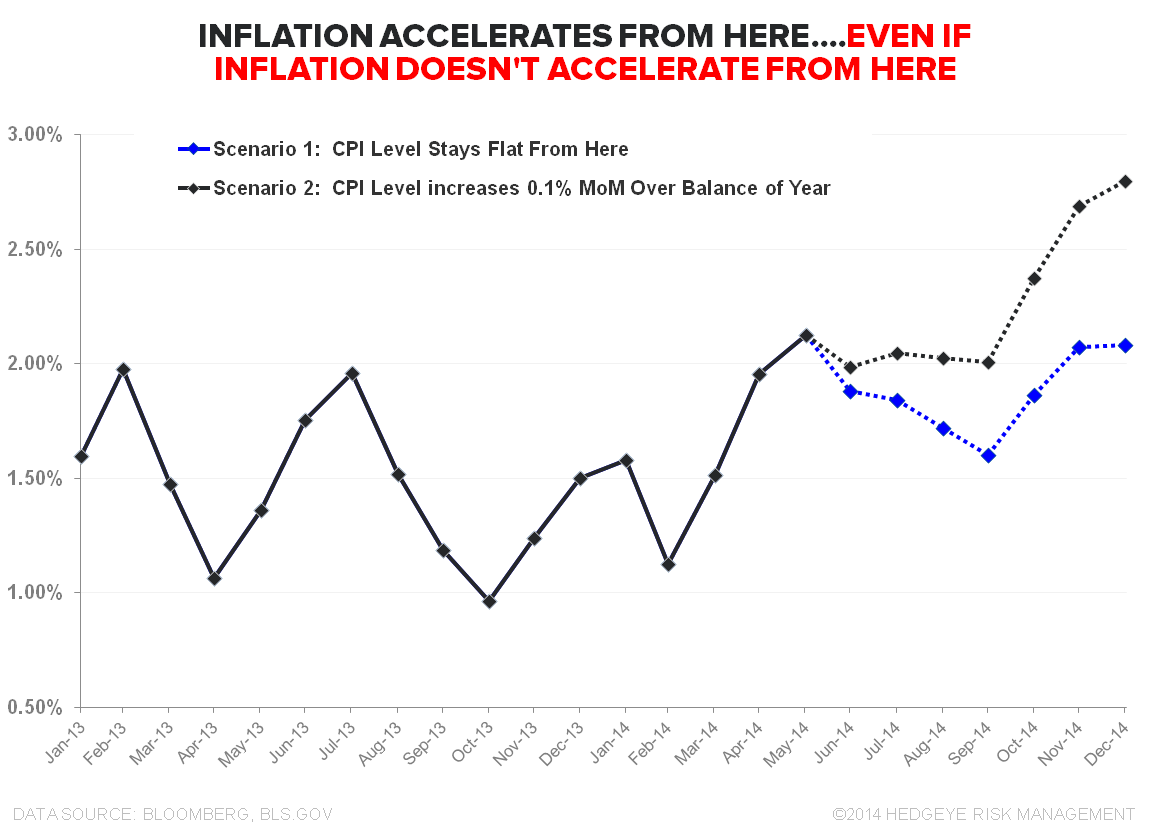

Interestingly, the slope of price growth need not continue increasing for inflation to hold the 2% line or accelerate further over the balance of 2014.

To illustrate, we show two simple scenario’s in the chart below:

- Scenario 1: if the current CPI Index level doesn’t change at all for the balance of the year, CPI growth will finish 2014 >2% as base effects predominate.

- Scenario 2: If the CPI Index compounds at +0.1% MoM (for reference: 6M ave = +0.3%/mo, TTM ave=+0.2%/mo) for the balance of the year, CPI inflation will be north of 2.80% at year end.

Simply, inflation comps continue to ease through October and we don’t need much in the way of incremental price growth to drive a further acceleration in reported CPI growth.

With oil prices jumping alongside heightened geopolitical risk, the $USD still broken, and the potential for the Fed to get rhetorically easier alongside a slowdown in both housing and the consumer, we continue to think the risk to inflation estimates is to the upside – at least through the third quarter.

REAL WAGE GROWTH: Back to Negative Growth in May

Flat Nominal Wage growth + Accelerating Inflation = Lower Real Wage growth

It’s been our contention that the conflation of dollar depreciation and rising inflation serves to slow real growth as food/energy/rent costs take down a rising share of the consumer’s wallet.

The identity above is trivial, but the gravity associated with that reality in terms of household capacity for accelerating real, discretionary consumption is not insignificant – particularly with consensus 2014 growth estimates still aggressive despite the iterative haircutting of expectations over the last few months.

To the point, this morning BLS reported real weekly earnings grew -0.1% YoY in May while real average hourly earnings declined -0.2% YoY.

Sure there are some signs of wage inflation pressures building under the hood, but overtly strong labor and income dynamics propelling resurgent consumerism isn’t the reality of the moment. Negative real earnings growth in May appears in harmony with the middling consumer spending data in April/May and the conspicuous rise in revolving credit.

Christian B. Drake

@HedgeyeUSA