The quantitative set-up for Brent Crude is in what we call a Bullish Formation (i.e. bullish on all 3 of our core risk management durations, TRADE, TREND, and TAIL).

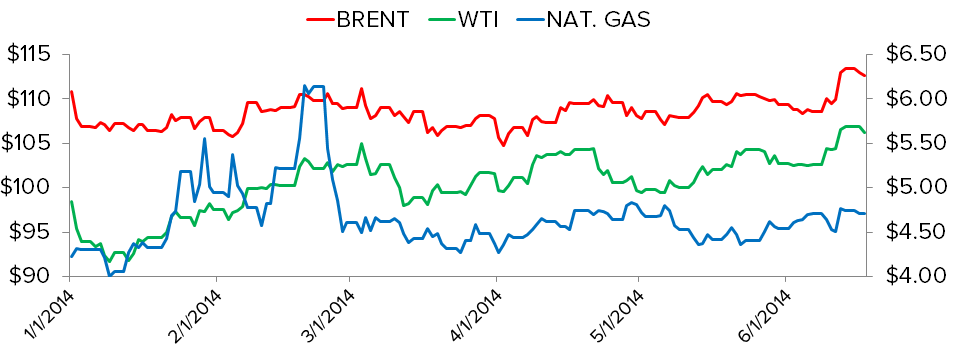

Brent Crude increased +4.4% on ICE last week to its highest level since September and now sits at +1.8% YTD after hovering unchanged for most of the year. WTI also touched 9-month highs on NYMEX on Friday, closing at +4.1% on the week (+8.6% YTD). Market sentiment, as measured by net positions in all actively traded futures and options contracts, suggests the market is leaning 4.7% longer than its 6-month average. Volume in Brent has spiked and front-month implied volatility has more than doubled to 18% from the lowest levels since 1988 on June 3rd (7.2%).

The CRB sits at +10.5% YTD with 16 out of 19 commodities in green territory. We reiterated our consumer slowing call yesterday in the chart-of-the-day by showing a snapshot of just how sensitive the average American is to food and housing prices:

Hedgeye’s inflation call has not been to ignore the potential price impact of unexpected weather and geopolitical tension in commodity markets year-to-date. Periods of relative calmness followed by bouts of heightened volatility have historically been commonplace. The commodity inflation that perpetuates our #consumerslowing theme remains a self-reinforcing headwind on the consumer. With a final Q1 GDP revision that could be as low as -2% on the 25th coupled with a CPI reading this morning that doubled-up expectations (+0.2% vs. +0.4% estimated), an easier than expected policy response tomorrow from Janet Yellen is probable.

Market participants choose to hold commodities for different reasons. For example, our view on Gold’s interaction with policy has been well documented. We added Gold (ETF: GLD) to Hedgeye’s investing ideas on May 23rd and remain comfortable on the long-side:

To clarify our process, we do not view the choice to hold GOLD or something like a COFFEE futures contract to hedge the heightened expectation of future dollar devaluation as interchangeable. With regard to the push-back we have received on highlighting weather-driven, overextended softs and agricultural commodities as a driver in our inflation call...

We have not made the argument that the entire complex’s negative correlation with the dollar is purely a growth and policy relationship. However, a spike in the cost of the goods and services that people consume alongside a flat dollar perpetuated by wealth-destroying monetarism burdens the consumer on the margins. This squeeze results in slower-than-expected consumption growth. We highlight the risk in this environment by alluding to sector variances and the increasingly negative correlations between the U.S. dollar and the commodity complex as a whole as this shift takes place.

Therefore, ignoring all arguments for why commodity prices are at artificially-high levels (i.e. weather, geopolitics, etc.), the reality is that they ARE in fact much higher from three months ago:

It will always be difficult to predict the next volatility-producing event in the space, but consequential responses to sharp changes in supply and demand are almost certain to follow. Unfortunately monetary policy has made the average consumer increasingly sensitive to commodity and asset price inflation as margins become thinner on a micro level. Almost 50% of the average American’s after-tax income is spent on food, housing, and utilities.

---

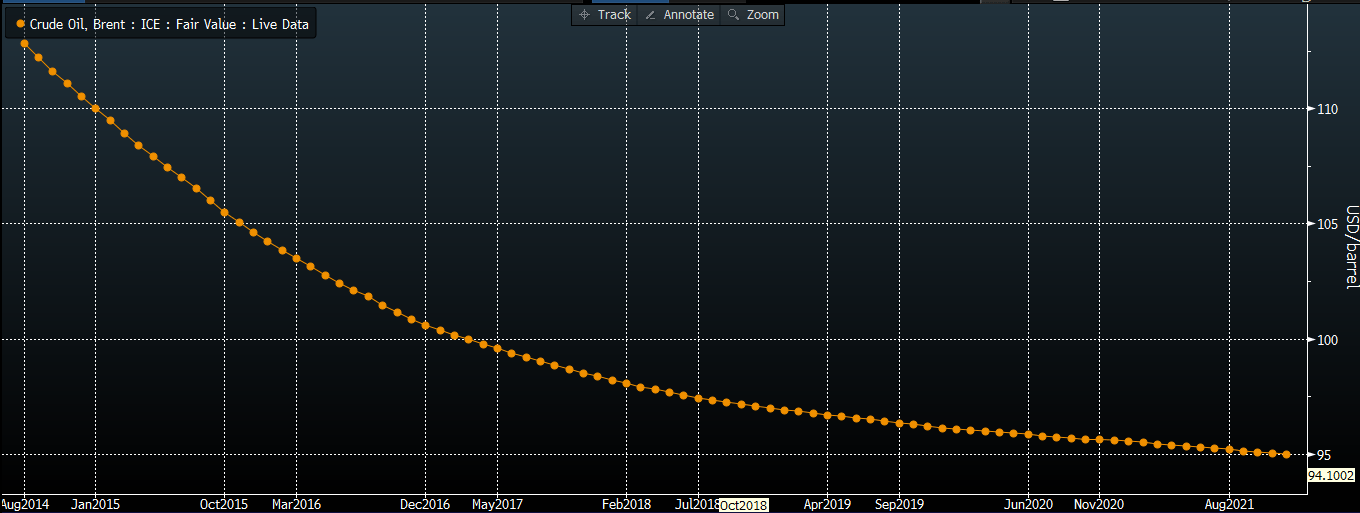

Proven crude oil reserves seem plentiful with North America’s newly utilized capacity. Brent has hovered in negative territory for most of the year with the crack spread near all-time highs despite geopolitical tension and a surge in the commodity complex. The forward curve suggests this downward trend will continue:

However, a number of factors suggest that today’s geopolitical dynamic is capable of instilling fear of short-term supply disruptions:

1) Chinese reserve-build policy and forceful effort to obtain production capacity abroad (East and South China Seas)

2) Political Unrest in OPEC’s second largest producing country

3) Supply restraints imposed on Ukraine

On Friday June 6th we hosted guest speaker, Professor Charles Hill to highlight some of the axioms of these three points of concern:

The EIA estimates that southern Iraq holds about 75% of the country’s proven reserves. Iraq shipped 3.3MM barrels/day last month on average and it ranks second in oil exports among OPEC countries behind Saudi Arabia. All of May’s exports were shipped out of southern ports. ISIL militants were successful in seizing the Kirkuk-Ceyhan pipeline, halting repairs, and taking Iraq’s second-biggest city, Mosul, but oil has ceased had flowing through this Mediterranean port since March 2nd. Nevertheless ISIL has successfully halted stopped the repairing of this pipeline which is capable of exporting 310K barrels/day. Abdalla El-Badri, Secretary General of OPEC, said yesterday in front of the World Petroleum Congress that Iraq will maintain its production limit of 300MM barrels/day for now. Iraq successfully shipped 5.43M barrels of oil from Basra in Southern Iraq on Friday and supply disruptions have not yet materialized.

Ben Ryan

Analyst