This note was originally published at 8am on June 03, 2014 for Hedgeye subscribers.

“Dude, look at your dirty shoes – you need a shine!”

-Joe (NYC)

Yesterday I was getting my shoes shined in NYC at one of my favorite spots – on the corner of Avenue of the Americas and 46th Street, right across from the building where I got fired.

Not that I keep track of the when and the why, but I wrote a book about it so it’s out there. Carlyle fired me for being “too bearish” on the US #ConsumerSlowing on November 2, 2007. My 1st son was born on November 7th. And the SP500 dropped 6% by the end of the month.

Yep, risk happens slowly, then all at once. You know when your shoes are dirty too. If you go to my spot, tell Joe I sent you. He’ll chirp anyone who is looking NYC serious with dirty shoes. Within a block, they all look down. They may not like it, but the truth is staring at them from their feet.

Back to the Global Macro Grind…

Our preferred US Equity Growth index to be short of in 2014 remains the Russell 2000. In addition to being down -0.5% on Friday, it dropped another -0.7% yesterday to -3.1% YTD.

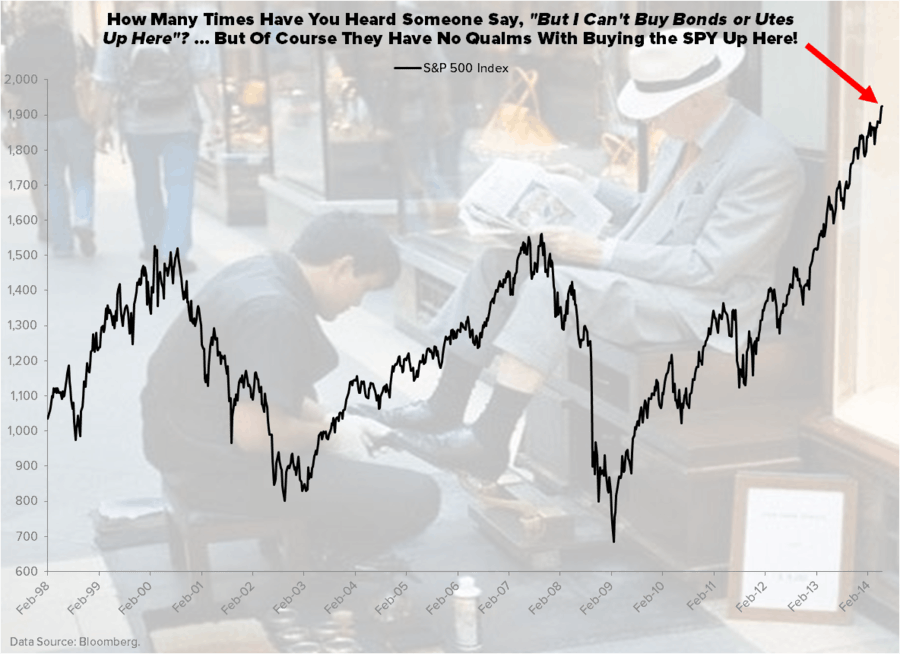

BREAKING: SP500 hits all-time highs –CNBC

Yep, as bond yields crash YTD (peak-to-trough decline in the 10yr Treasury Yield = 20%) and the Russell delivers negative returns, the world’s most consensus short position (SPX Index + E-mini) hit another new high on no volume yesterday. #hooray

Whatever you do, don’t look at your shoes yet.

Total US Equity Market Volume was -28% versus its 3-month average (and the average continues to crash!) and the US Equity market’s breadth (advancing vs. decline stocks) was negative yesterday too (46% gained in price, 50% declined). #dirty

But, but, you have to buy the SP500 … because it’s up, right?

As long as you buy SPX vs short Russell (IWM), I’m into that. From a risk Style Factoring perspective, the SP500 is not the Russell:

- SP500 has plenty of #InflationAccelerating components (like Energy and late-cycle Industrial companies taking price)

- SP500 has many more slow-growth #YieldChasing components (Utilities, REITS, Telecom, etc.)

- SP500 has way more consensus short sellers who tend to short low and cover high

Like the FTSE in the UK, the SP500 is much more multinational too. If you want the pure play on short US domestic growth, it’s the Russell.

While there’s no doubt that it’s a lot easier to call the macro game from the seat I have today than the one I used to be in, that doesn’t mean that market truths cease to exist. #OldWall hasn’t been there to help coach Portfolio Managers through US growth slowdowns. We have been.

Being right in an environment with Rising Variance at both the country and sector level gets easier if you know the macro economy we are in. With US #InflationAccelerating perpetuating US #ConsumerSlowing, here are the Top 3 US Equity Sectors you still want to be long:

- Energy (XLE)

- Utilities (XLU)

- REITS (VNQ)

To reiterate the Sector Style Factors you do not want to be long:

- Consumer Discretionary (XLY)

- Housing (ITB)

- Financials (XLF)

If you leave being US Equity market centric (life is easier that way), buying currencies and stocks in countries who had what the USA had last year (#StrongCurrency + #RatesRising and inflation deflating), current equity markets we still like on the long side are:

- United Kingdom (EWU)

- India (INP)

- Brazil (EWZ)

In addition to being long Bonds (TLT), Inflation Protection (TIP), and Commodities in 2014, it’s what you aren’t long when growth slows (bubble multiple stocks) that has made all the difference too.

My call wasn’t consensus in November 2007, and it wasn’t in January of 2014 either. While we need to be loud about seeing something that we don’t think the Street is paying attention to, we don’t want that to feel dirty to you. We want to help augment your process and keep your shoes shiny.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.42-2.57%

RUT 1089-1155

VIX 10.94-13.59

USD 80.05-80.75

British Pound 1.67-1.69

Brent Oil 108.42-110.76

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer