Below are Hedgeye analysts' latest updates on our eight current high-conviction investing ideas.

We also feature two institutional research notes from earlier this week and one special video which offer valuable insight into the markets and economy.

*Please note that CEO Keith McCullough's updated levels for each stock and ETF will be sent separately.

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

GLD – Coming off a jump after last week’s ECB meeting to close at +75 bps on Thursday, Gold closed down a meager -4 bps on Friday on U.S. equity volume that was -32% below the 3-month average. This week it’s grinded higher to close in the green every session. Gold is up 6% YTD and increased +2.4% since last Wednesday’s close (+1.7% on the week).

Sentiment, as measured by CFTC net futures and options contracts, which shifted from net long 48K contrcats at the beginning of the year, to net long 172K on March 18th when the Euro peaked, decreased for four consecutive weeks to 77K (32% below its 6-month average). As of Thursday’s close, front month implied volatilities were trading -7.0% below 1-month averages, -20% below three month averages, and 25% below 6-month averages. This shift provides some uncertainty into the FOMC next week, but we remain bullish on Gold in the face of consensus growth estimates that are still positioned for disappointments.

Regardless of recent geopolitical developments driving prices, prices ARE nevertheless higher, making these already difficult comps more difficult as the commodity squeeze continued this week:

- CRB: +1.50%

- Brent: +4.28%

- RBOB Gasoline: +4.2%

Consensus GDP estimates for 2014 full year are still in the +2-3% range. After the negative Q1 GDP revision to -1.0%, this implies a +4% increase from here the rest of the year. Considering that services consumption was a point of strength made up mostly by a significant uptick in healthcare service consumption, a further downward revision on June 25th is probable. The census bureau negatively revised the calculation that feeds the healthcare portion of services spending (17% of total services consumption) this week. This affirming data point perpetuates our view that growth comps look more difficult on the margins. Why does this matter for Gold? Because the prospect of an easier than expected fed in 2H, if not next Thursday, is likely to continue.

Our view on Gold’s strong interaction with interest rates and policy is well-understood. Correlations get stronger and weaker over time, and in low volatility periods of market complacency (VIX near all-time lows, bull/bear spread at YTD highs) Gold tends to run tighter negative correlations with the USD and Treasuries. In this complacent environment, growth, interest rates, and policy drive the interaction. The trailing 1, 3, and 6 month correlations held steady near YTD highs at -0.69, -0.63, and -0.64 respectively.

HCA – Editor's note: Healthcare sector head Tom Tobin added HCA Holdings to Investing Ideas exactly one year ago today on 6/14/13. Shares of HCA have more than doubled the S&P 500 since, gaining over 38%.

Back in 2011, when we first become interested in HCA Holdings on the long side, the company and the industry had just come through one of the more difficult times for the industry. Admissions were soft, there was an unexplained shift away from higher acuity cases, and implantable cardio defibrillator (ICD) implants were declining dramatically after research showed surgeons were overusing them. Presently however, we are starting to get marginally cautious as we are noticing several of our Key Drivers show some mixed results.

Maternity (something we have written about extensively) may still be a bright spot when we update data from the US Census Bureau later this month. But we are looking at a mixed bag in the shorter term among other important key drivers.

PPI for Medical and Surgical Catheters: If the relationship continues to hold between the PPI for Medical Surgical Catheters and US ICD sales, we would expect revenue trends within Cardiology (15% of Hospital revenue) to be under some pressure. We might even go so far as to look for a short among BSX, MDT, or STJ, the major ICD manufacturers.

Local Government Employment: As we witnessed the recovery in Orthopedic growth in the US, the best leading indicator has been Local Government Employment. There may indeed be a direct relationship between a Total Knee Replacement surgical case and Local Gov’t Employment growth given these employees are much older, carry generous medical benefits, and are a significant percentage of the workforce. But it may also reflect a broader demand dynamic that includes positive trends in housing, property taxes, and sales taxes. We think there may be as many as 300,000 knee replacement cases that were deferred over the last 5 years. So, a persistent turn would help the Orthopedic revenues, the largest contributor at 17% of total inpatient revenue.

Hospital Employment: The long pause in hiring by hospitals may have hit a low in 1Q14, although so far in 2Q, the recovery is modest at best. It’s possible hospitals were preparing for the uncertainties of the Affordable Care Act and simply stopped hiring. Maybe it was the weather in 1Q14. Either way, we’d like to see a consistently improving trend.

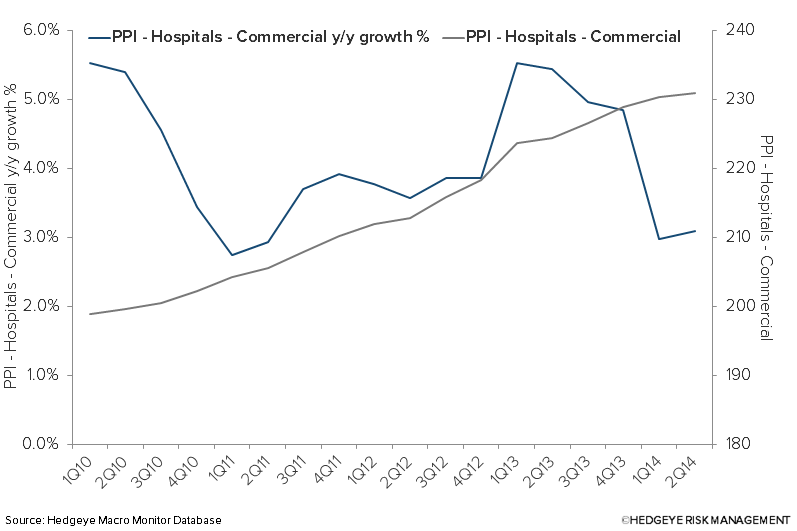

PPI Hospitals Commercial Insurance: The trend is weak for this critical revenue and profit driver. Medicare pricing has already been under pressure under ACA related reductions. We really need to see this series recover over the coming months as comparisons get easier.

HOLX – Healthcare sector head Tom Tobin has no update on Hologic this week. Tobin reiterates his high-conviction call on the stock.

LM – It was another week of fixed income inflow from the mutual fund channel which continues to support owning and adding to shares of Legg Mason. While the $1.1 billion that came into all bond funds during the most recent 5 day period was below the weekly year-to-date average of $2.0 billion per week thus far in 2014, the quarter-to-date trends are undeniable that defensive fixed income managers are the place to be in the asset management sector.

Thus far in the second quarter, fixed income funds have netted over $20.0 billion, versus all equity funds which have taken in just $6.8 billion. This trend will flow through to the group as bond assets increase faster than equity fund assets, and thus leading fixed income managers like Legg have faster profit growth.

In addition, we continue to point to Legg’s excess capital of $1.0 billion that can be used for share repurchases and acquisitions as creating alpha, or outside of market returns, as a strong reason to be involved in the story.

LO – Lorillard was up just slightly on the week. The investment community still wonders if LO will be taken out, likely by Reynolds American (RAI).

We continue to suggest that investors hold this stock into potential news of the buyout, or until our long-term fair value price of the stock at $80/share is realized. We also continue to highlight that the company’s powerful earnings generation is anchored on its advantaged tobacco and e-cigarette portfolio.

Bottom line: We do not think LO will be imminently purchased and are staying long the stock that we added to Investing Ideas on 3/7/14.

OC – There were two positive and noteworthy developments supporting our bullish case on Owens Corning this week:

First, nonresidential construction activity continues to pick up heading into the summer. The Dodge Momentum Index (a measure of nonresidential building projects in planning by McGraw-Hill Construction) ticked up 2% month-over-month and is up over 8% year-over-year. It was the highest number since mid to late 2004. The Dodge momentum indicator tends to lead nonresidential spending by a full year.

Second, the Census Bureau’s nonresidential public construction spending is stabilizing showing a 2% gain year-over-year for April. The April reading was the highest in five years.

RH – This quarter served as another milestone for Restoration Hardware in its march towards $11.00 in earnings, and additional proof for us that this is perhaps the best idea in all of US retail. The stock’s move above $80 this week is obviously nice…we’ll definitely take that. But it’d be a mistake to lose sight of the very real potential for this to be a $200+ stock over a 3-4 year time period. The EPS CAGR RH we’ll need to get there is over 40%, and our research says it’ll get there. What multiple is fair for a 40% EPS grower that earns $11? Let’s say 20x, conservatively. If we’re right on earnings, we can build to a stock well above $200. In other words, the call is not done. It’s really just beginning.

Think about it like this: RH went over six years shrinking its real estate footprint. But starting next quarter, it will go on a 5-7 year tear as it executes on its store growth strategy. Next year alone, we should see square footage grow in excess of 40%. And it’s doing this while it simultaneously executes its category expansion plan – such as kitchens, which alone should be a $2bn business.

Our point is that it’s easy to get hung up on a given quarter with this (or any) company, and this quarter the stock is definitely getting its due. But if you look at a the story bigger picture, you’ll see that it consolidated for six years, and now should gain share of the market at an accelerated rate for another six years. The bottom line is that it seems a little short-sighted from where we sit to think that just because the stock is hitting new highs that the opportunity is over.

TIP – Last Friday, we added the iShares TIPS Bond ETF TIP to Investing Ideas list and continue to favor inflation-protection in the context of what we see as developing cyclical and structural inflationary pressures domestically.

Below is a list of relevant high-frequency economic data that was released this week:

- MAY Import Price Index: +0.4% YoY from -0.4% prior. In line with our expectations, import price inflation should continue accelerating, on the margin.

- MAY Headline PPI: +2% YoY from +2.1% prior; ex-Food & Energy, PPI accelerated to +2% YoY from +1.9% prior. A rebound in food and energy inflation should continue to pressure domestic producers from a COGS perspective (e.g. Brent Crude Oil is up over +4% in the week-to-date).

- Per the MAY NFIB Small Business Optimism Index: “Seasonally adjusted, the net percent of owners raising selling prices was a net 12 percent, unchanged from April after an 8 point rise in March. Overall, there is more upward pressure on prices… Seasonally adjusted, a net 21 percent plan price hikes (down 1 point [from April]). If successful, the economy will see a bit more “inflation” as the price indices seem to be suggesting.”

Inflation forecast summary: Trend-line sequential momentum accelerating? Check. Annual comparisons getting easier on the margin? Check.

All told, the rate of consumer price inflation remains poised to accelerate throughout the year. Take advantage of this macroeconomic catalyst by allocating capital to TIPS (etf: TIP).

* * * * * * *

Click on each title below to unlock the content.

McDonald's: It's Time for a Change

Every month, we read the MCD press release on monthly sales trends expecting to see something more writes restaurants sector head Howard Penney.

Cognitive Dissonance: Death By a Thousand Data Points

Macro analyst Christian Drake takes a deep look into the data and notes that domestic growth estimates continue to decline as the economic data comes in.

Real Conversations: James Grant Says Buy Gold

Among other investing ideas and kernels of wisdom, James Grant, editor of Grant's Interest Rate Observer explains to Hedgeye CEO Keith McCullough why he believes investors should be buying gold.