We added BOBE to the Hedgeye Best Ideas list as a long on 05/02/2014 at 47.21/share. We continue to believe there is a significant opportunity for value creation at the company that activist investor Sandell Asset Management is working hard to unlock. This is our highest conviction long idea.

All told, we aren’t expecting much good news when BOBE reports next Tuesday and highly recommend buying into any weakness. If you missed our Best Idea call, we encourage you to review our thesis in the deck below.

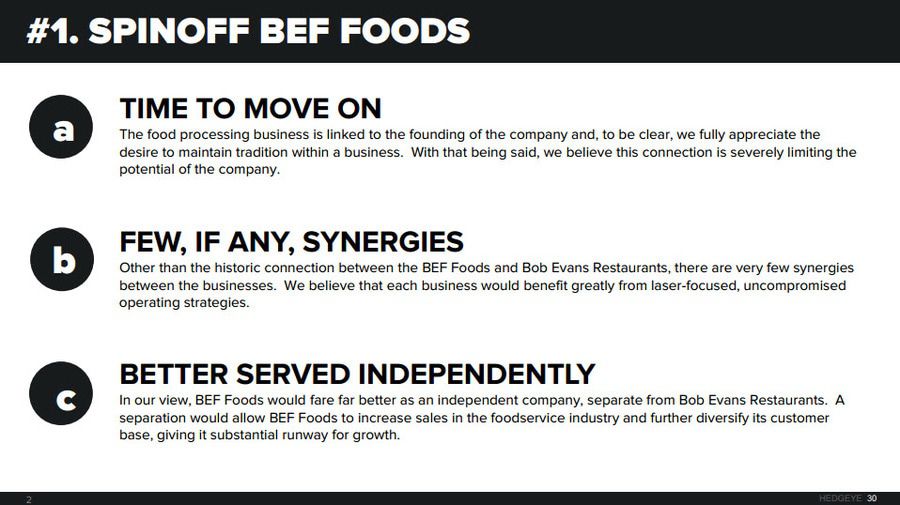

Presentation – Best Idea: Long BOBE

The Bob Evans story has flown under the radar for quite a while, but is beginning to generate some well-deserved attention. Earlier this week, Tyson Foods (TSN) won a bidding war to acquire Hillshire Brands (HSH), the maker of Jimmy Dean sausage and Ball Park hot dogs, at a substantial premium valuation. But that’s not all. Last night, BOBE was featured on Jim Cramer’s “Mad Money” during which he recommended the stock as a long for reasons similar to ours. We believe this heightened attention will help Sandell build considerable momentum in its pursuit to unlock significant shareholder value.

Considering the robust demand for protein companies, we believe now is the appropriate time to spinoff BEF Foods in what would be a value enhancing breakup. We also see opportunities for significant SG&A reductions and believe the restaurants business would be best served by transitioning to an asset light model.

If Sandell is successful in their efforts to effect change, we see at least +45% upside to BOBE shares. Please view our presentation for specific scenario analyses. Interestingly enough, the market is currently betting against Sandell (which we believe is a mistake), making it an opportune time to get into the name.

Call with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst