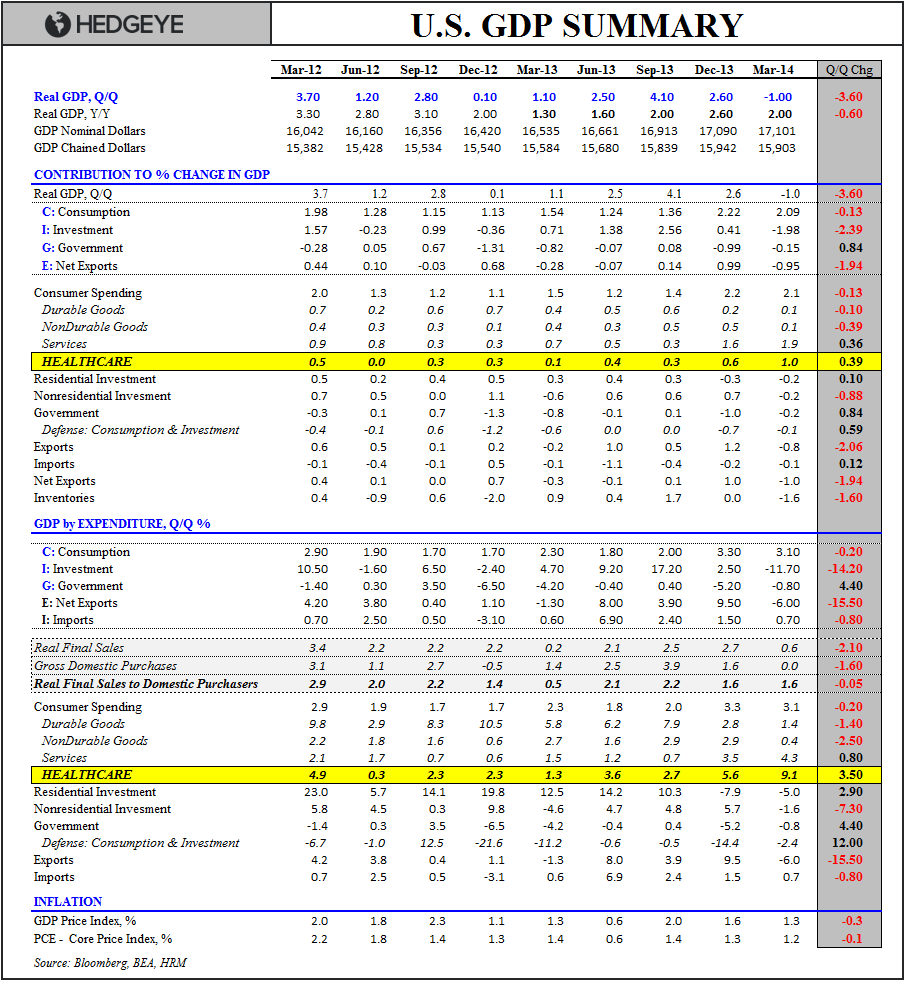

We’ve highlighted repeatedly over the last few months that reported healthcare spending in 1Q14 was largely a guess by the BEA due to the implementation of Obamacare and a dearth of hard data. More specifically, we noted the following in March & April:

*Healthcare Spending: The strength in Healthcare Services spending stems largely from the implementation of Obamacare. The reported figures, by BEA’s own admission (see their note Here), are very much an estimate and the preliminary data are likely to be revised (significantly) over time as the Census bureau’s quarterly QSS and annual SAS survey’s provide harder data.

With reported Hospital and Outpatient spending both accelerating materially in 1Q14, it could also be that individuals are accelerating medical consumption ahead of ACA implementation and uncertainty around coverage changes.

Either way, in the context of the broader spending data, the takeaway is pretty straightforward – Healthcare Services represent ~17% of total household consumption expenditures and certainly impacts the direction of reported, headline consumption growth. To the extent that deceleration is the larger trend across the balance of services, a mis-estimation of ACA related spending and/or a significant, transient pull-forward in medical consumption could be materially distorting the prevailing, underlying trend.

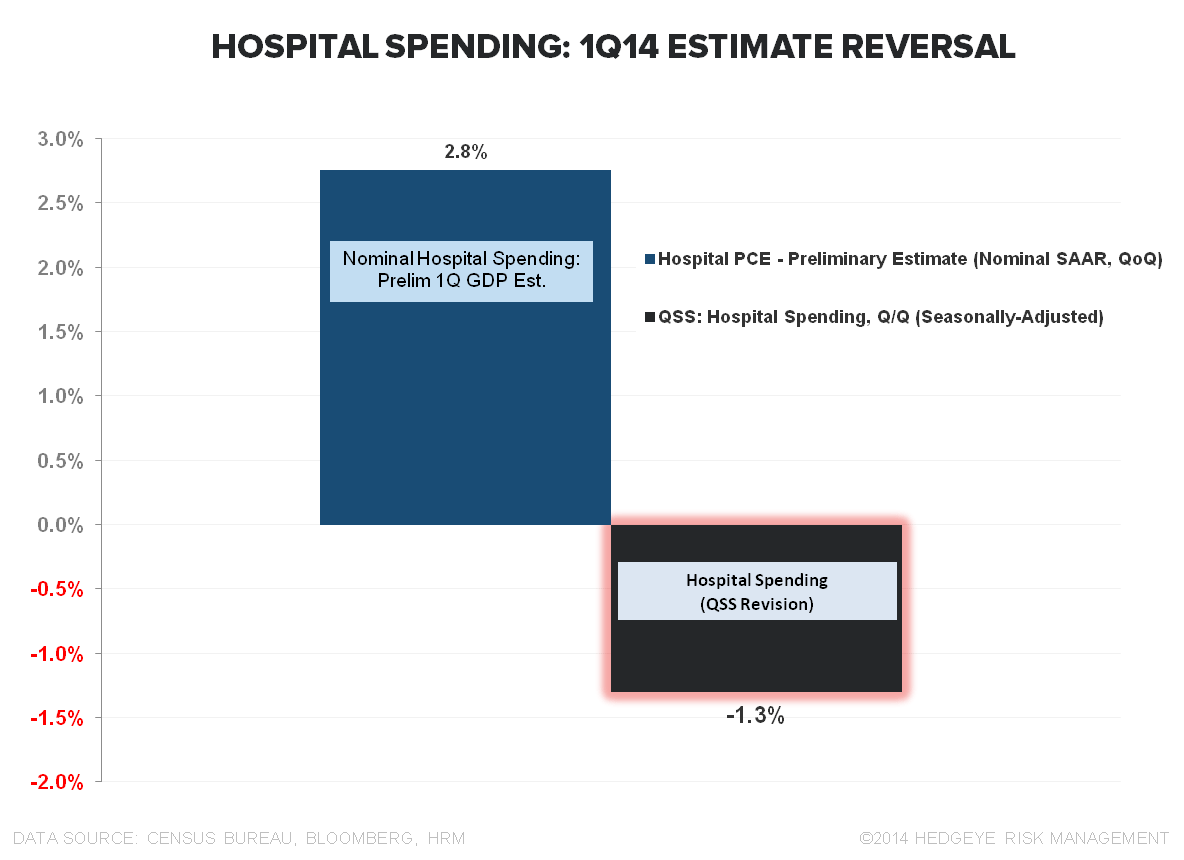

The Census Bureau released the 1Q14 QSS data this morning (note: the QSS survey data feeds the calculation of household spending in GDP) and the estimate for Healthcare spending saw a sharp negative revision.

Specifically, the data showed total revenue for Healthcare and social-assistance declined -2% QoQ in 1Q14 while Hospital revenue (the largest component of healthcare spending) declined -1.3% QoQ.

Translating that into an exact impact on the final GDP estimate for 1Q14 (June 25th) is complicated by the fact that the reported QSS Healthcare spending data is both nominal and non-seasonally adjusted while the Hospital revenue is not adjusted for price changes (but is reported on a seasonally adjusted basis)

The translation complication is really besides the point, however. The larger takeaway is simply this:

Services consumption was the singular source of strength in the 1Q14 GDP report and most of that was from Healthcare Services which contributed +1.01% to GDP – that estimate of accelerating healthcare consumption just got revised to negative growth which will take the final GDP estimate for 1Q down to -2.0% plus or minus.

It also notable that Healthcare consumption growth, while decelerating modestly sequentially, was still very strong in April (again one of the lone sources of strength in household spending). If the April (& 2Q) numbers get revised lower also then 2Q growth estimates will take a hit as well.

Full year consensus growth estimates for 2014 remain in the +2.5%-3% range - implying 4%+ growth over the balance of the year (exclusive of the forthcoming negative revision to 1Q). Those estimates still need to come down.

Christian B. Drake

@HedgeyeUSA