This note was originally published at 8am on May 28, 2014 for Hedgeye subscribers.

“Only when we admit what we don’t know can we ever hope to learn it.”

-Ed Catmull

That’s another fantastic leadership quote from a new book I introduced in yesterday’s Early Look – Creativity Inc. – Overcoming The Unseen Forces That Stand In The Way of True Inspiration.

“The best managers acknowledge and make room for what they do not know – not just because humility is a virtue but because until one adopts that mindset, the more striking breakthroughs cannot occur… They must accept risk… and engage with anything that creates fear.” –Ed Catmull

I can tell you that I wake up every morning living in fear of one simple thing – losing. I hate losing. And I refuse to allow my team to lose for extended periods of time. If and when we are wrong, we either double down or change our mind. We get paid to take a line and be held accountable to it.

Back to the Global Macro Grind…

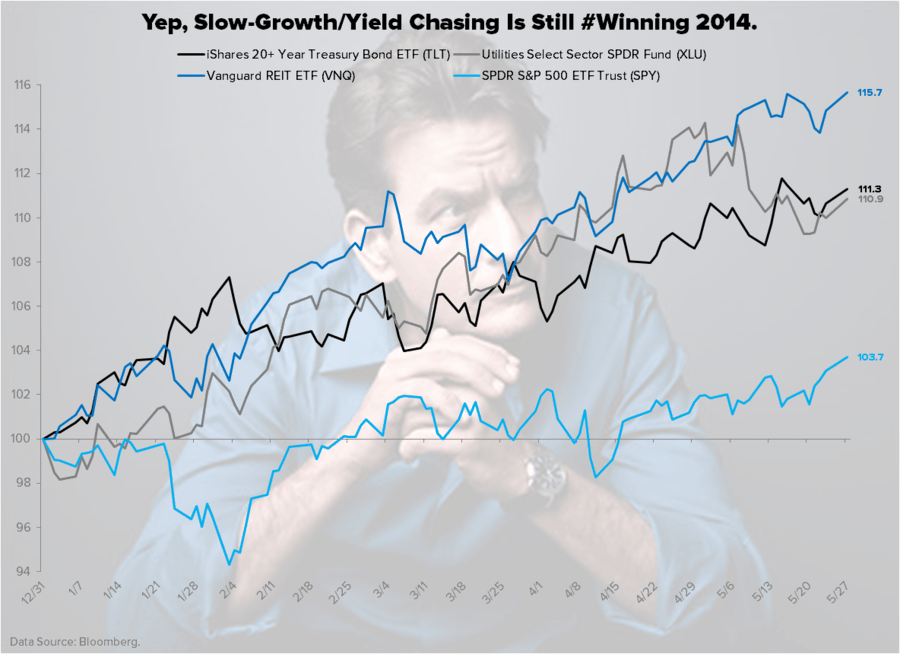

Being long slow-growth and #YieldChasing in 2014 (i.e. being long bonds and/or anything equities that looks like a bond) has not only been the winning position YTD, but it was yesterday too.

With SP500 busting out (on no volume – US Equity Volume -29% vs the 3mth avg) to all-time-bubble highs intraday, bonds reversed from opening down to closing at their highs of the day. The 10yr UST Yield has ticked down yet again this morning to re-test a fresh 2014 low of 2.49%. Bond bears are losing.

But, but, Biotech (IBB) +2.5% yesterday was winning. Yep, nice trade. I just hope you didn’t own it the whole way down, because that “growth” sub-sector of the SP500 has been a certified train wreck this year. Most things high-multiple, high-beta have been.

“So” do we buyem because they were up?

Let’s get real here folks. I left Career Risk Management Inc. in 2007 so that on days like this I could double-down on my team’s hard work and process. If you want to beat a monthly bogey, great – chase the wabbit. If you want to win a championship in 2014, stay with the fundamental trends.

In the US, here are the big intermediate-term TRENDs that have been winning for the last 5-6 months:

1. US #InflationAcclerating

2. US #ConsumerSlowing

3. US #HousingSlowdown

Winning being defined as the score:

1. CRB Commodities Index, Food, and Oil +8-22% YTD #InflationAcclerating

2. US Consumer Discretionary Stocks (XLY) = DOWN -2.1% YTD #ConsumerSlowing

3. US Housing Stocks (ITB)= DOWN -3.0% YTD #HousingSlowdown

That’s not to say that I didn’t feel like the NY Rangers last night. However magical a playoff run they’ve had, getting lit up for 7 goals in Montreal feels like I did at yesterday’s market close. Kreider went to de penalty box in the first minute of the game. Canadiens scored. He felt shame.

“So” why shouldn’t I change our entire Macro Theme Deck (6-12 month view) and positioning this morning?

1. Why isn’t it “different this time” (i.e. bond yields going down aren’t an explicit sign of US growth slowing)?

2. Why isn’t it time to giddy up and buy stocks like Facebook, Twitter, and Yelp that blew up into the thralls of April?

3. Why isn’t it time to pretend that no-volume and an 11 VIX doesn’t matter as a risk management signal anymore?

Why Mucker? Why can’t you just change everything you and your team have done YTD and join a crowded consensus long-growth US Equity Multiple Expansion (and bearish on inflation and bonds) view that almost everyone else on the sell-side has?

What would change my mind? That’s easy. Going back to what we loved about our US #GrowthAccelerating call in 2013:

1. #StrongDollar

2. #RatesRising

3. #DeflatingTheInflation

In fact the Swiss have some of that this morning. As the Swiss Franc ripped to new highs, Swiss Exports ramped +2% year-over-year and so did Switzerland’s GDP growth rate. Sound familiar, Mr. Krugman? Same thing happened this year in the UK. #StrongCurrency tax cuts for The People.

“So”, other than a lot, what else don’t we know that could be driving spooos higher with the Russell 2000 -1.9% YTD?

1. How many hedge funds came into 2014 levered long growth, got smoked, then shorted the April lows?

2. How many people have Yellen and Bernanke whispered to that if growth continues to slow, that they go Qe6?

3. How many one-legged ducks can avoid swimming in a circle?

What we do know is that with the VIX at 11.51 (testing YTD lows) and the II Bull/Bear sentiment spread at its YTD highs (58.3% Bullish, 17.3% Bearish = +4100bps wide to the Bull side) that the buy in May, chase performance, and pray thing is alive and well.

Our immediate-term risk ranges are now (12 Global Macro Ranges are in our Daily Trading Range product):

UST 10yr Yield 2.48-2.60%

SPX 1888-1924

RUT 1089-1144

VIX 11.09-13.79

WTIC Oil 102.99-105.27

Gold 1261-1315

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer