“The distribution of wealth is one of today’s most widely discussed controversial issues.”

-Thomas Piketty

Roger that Tommy. And thanks for giving the world’s big central planning bureaucrats some Marxist 2.0. They needed a French Keynesian economist to inspire them.

Who is Karl Marx? According to Picketty, “In 1848… he published the Communist Manifesto, a short, hard hitting text…” (Capital In The Twenty First Century, pg 8). “Hard hitting?” #cool

Instead of calling this NY Times fan fav book “Capital”, it should have been titled “Class Warfare.” This is going to be a painful read for me, but I will endure. The last 1% of economists who think socialism is the best path to prosperity still need to be studied.

Back to the Global Macro Grind…

What is the last 1%?

- The last 1% rally in the Russell 2000 (IWM) on no-volume to lower-highs?

- The last 1% rally in US Consumer Discretionary (XLY) stocks to lower-highs?

- The last 1% of McDonald’s (MCD) customers slowing in May due to the February “weather”?

That last one was a beauty of a headline that the US government dudes perpetuating American Inequality via their Policy To Inflate had a tough time explaining yesterday. McDonald’s same-store US Sales for May were down -1% year-over-year with some of the best weather we’ve had in years.

After spending on primitive things like food and shelter (Food prices +21% YTD; US Rents at all-time highs), evidently America’s Median Consumer can’t afford to fill her car up with gas to go buy the new “family pack” (for $14.99) at Mickey D’s!

I was in Chicago seeing Institutional Investors all day yesterday and today I’ll be in Kansas City. The core of the bear case for US consumption growth is what is hitting the heart of America right now – it’s called #InflationAccellerating USA’s cost of living to all-time highs.

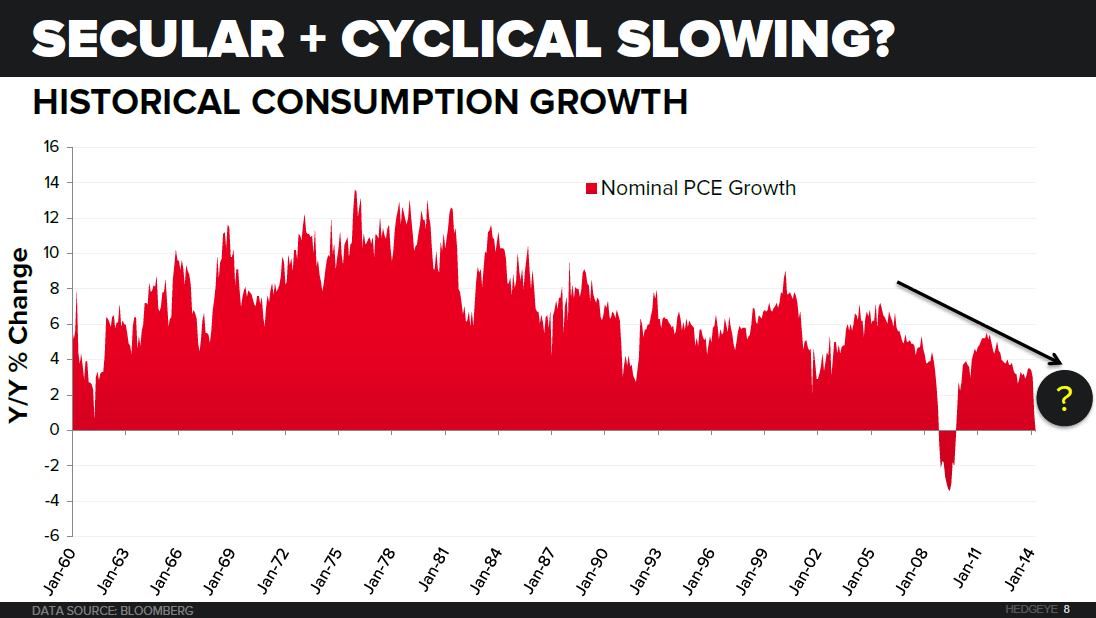

As you can see in today’s Chart of the Day, US Consumption Growth (1) is in what we call a long-term secular decline. That’s mainly because the 50yr chart overlaying that called cost of living (inflation) is in a secular bull market.

But whatever you do when debating people like Piketty on inequality, don’t talk about central planning policies that A) devalue the purchasing power of the people and B) inflate the cost of living.

In case you want to run against Hillary for President of the United States, just ask her the questions we answer in slides 12-15 in our current Hedgeye Macro Slide deck:

- Who Is The Median Consumer in this country?

- How Does the Consumer Make Money?

- Where Do They Spend it?

The answer for the Median Consumer in America on the spending side is this:

- Housing (34% of the country rents) = 29.2% of spending

- Transportation = 17.8% of spending

- Food = 12.5% of spending

“So”, if you tax that spending basket with an un-elected and un-legislated Policy To Inflate (read: print money), you get the answer to the inequality equation Krugmanites have been longing for:

FED POLICY + INFLATION = INEQUALITY

Yep. The top quintile of Americans (read: us) gets paid 66.4% of the benefits of money printing (interest, dividends, property related income, etc.). The median quintile gets 1.4%.

Inequality is only a “controversial issue” because, like in the 1970s, both the Democrat and Republican parties (Nixon/Carter then Bush/Obama) have supported Policies to Inflate, without calling them that.

Our immediate-term risk ranges (with bullish or bearish intermediate-term TREND signals in brackets) are as follows:

UST 10yr Yield 2.41-2.64% (bearish)

SPX 1 (bullish)

RUT 1133-1177 (bearish)

Nikkei 141 (bearish)

VIX 10.77-13.35 (bearish)

USD 80.23-80.89 (bearish)

EUR/USD 1.35-1.37 (bullish)

Pound 1.67-1.69 (bullish)

WTIC Oil 102.62-105.27 (bullish)

NatGas 4.53-4.76 (bullish)

Gold 1 (bullish)

Copper 3.01-3.11 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer