SUMMARY: I’ve been dealing with and strategically parenting around my 18-month olds discovery of and increasing proclivity for the word “No” over the last month, so we’ll go with that as the theme for May Employment as it sufficiently characterizes this mornings release:

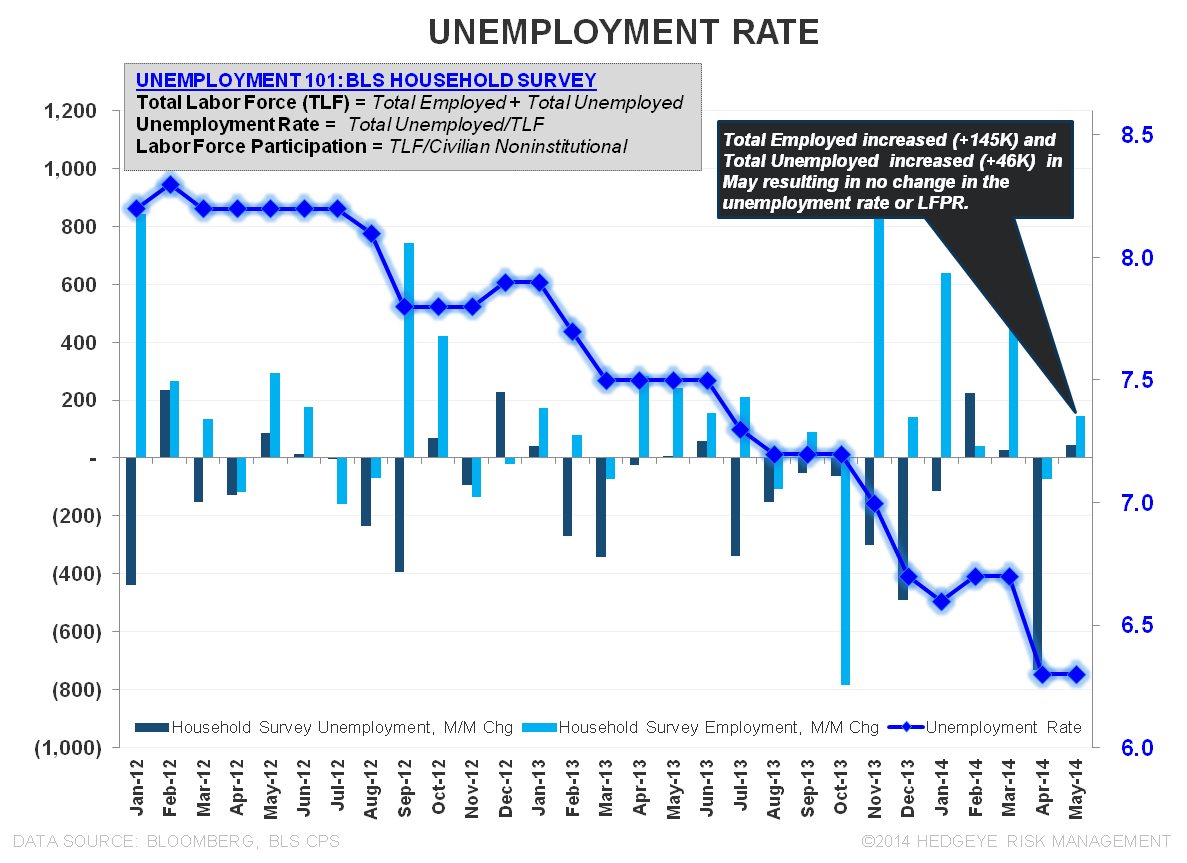

No change in Unemployment rate, No change in the U6-U3 spread, No change in the Labor Force Participation Rate, No acceleration in the pace of job growth, No acceleration in earnings growth, No good news for housing, No #EscapeVelocity in the labor market…and probably no change in the present policy course out of the fed.

No change in our intermediate-term outlook for growth either as we continue to think slow-growth exposure outperforms alongside rising inflation, a constrained consumer, and consensus expectations that require 4%+ GDP growth over the balance of 2014 to hit full year growth estimates. Reported Growth will obviously accelerate sequentially in 2Q14 but the TREND, at least through 3Q14, is one of deceleration.

A summary highlight of the numbers/data below:

A NEW HIGH: We eclipsed the January 2008 peak in Private employment last month and finally eclipsed the prior, Jan 2008, peak in total NFP employment by +98K with the net gain of +217K in May. The private sector’s share of total employment has increased 40bps to 84.2% compared to 83.8% prior to the recession.

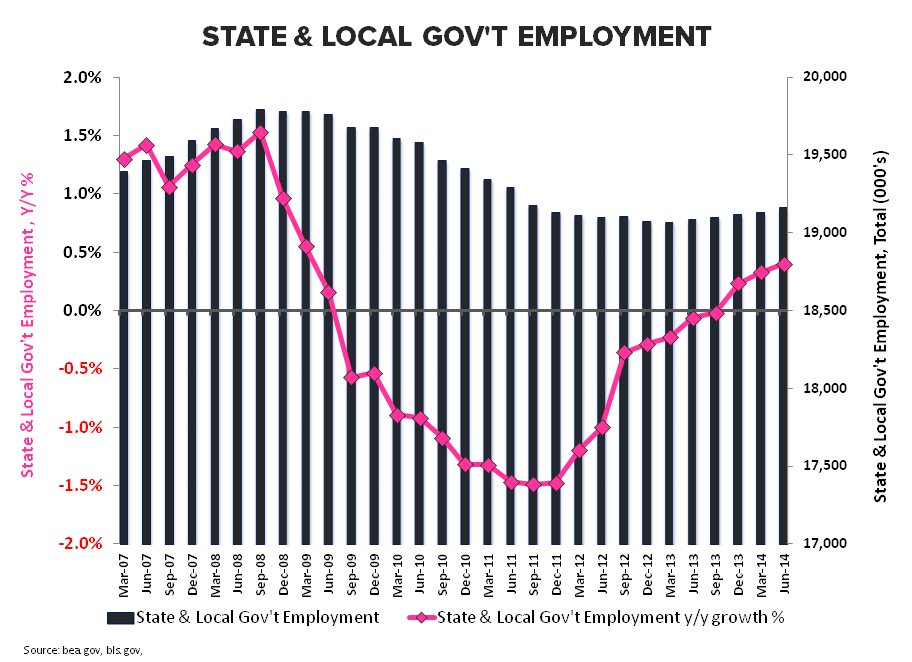

State & Local Government Employment increased for a 9th consecutive month in May while the rate of job loss at the Federal level improved 60bps sequentially to -2.3% YoY. Aggregate government salary and wage growth has finally begun to contribute positively to aggregate disposable income growth.

Labor Force Participation: The participation rate was static at 62.8% MoM in May. The shift in participation by age since the start of the recession is not new, nor particularly surprising, but notably, the divergence from pre-recession levels has continued to increase moderately, not mean revert.

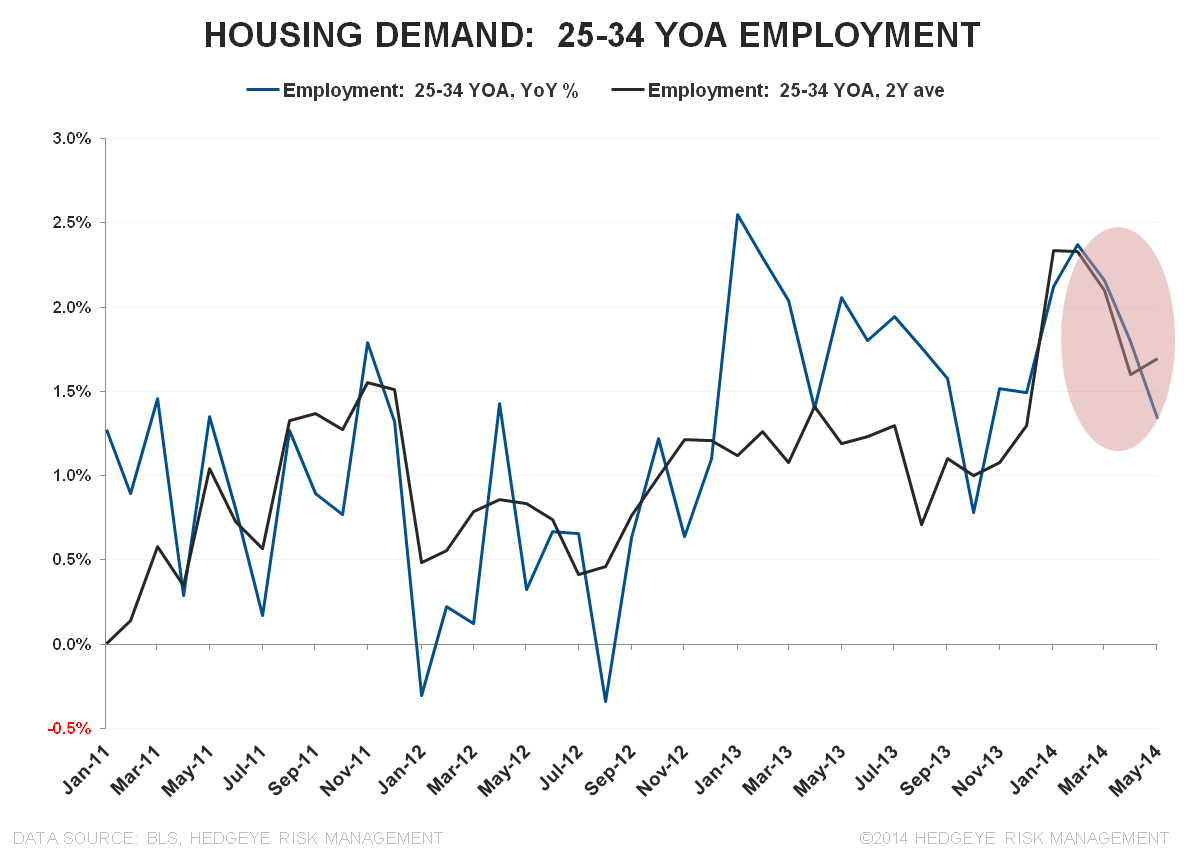

#HousingSlowing: Employment growth in the 25-34 year old buck decelerated for a third straight month in May. With 1st-time home buyers representing ~30% of the market and a key first rung in housing’s ladder, weak wage growth and decelerating employment trends in this key age demographic do not augur strength for forward housing demand/HPI

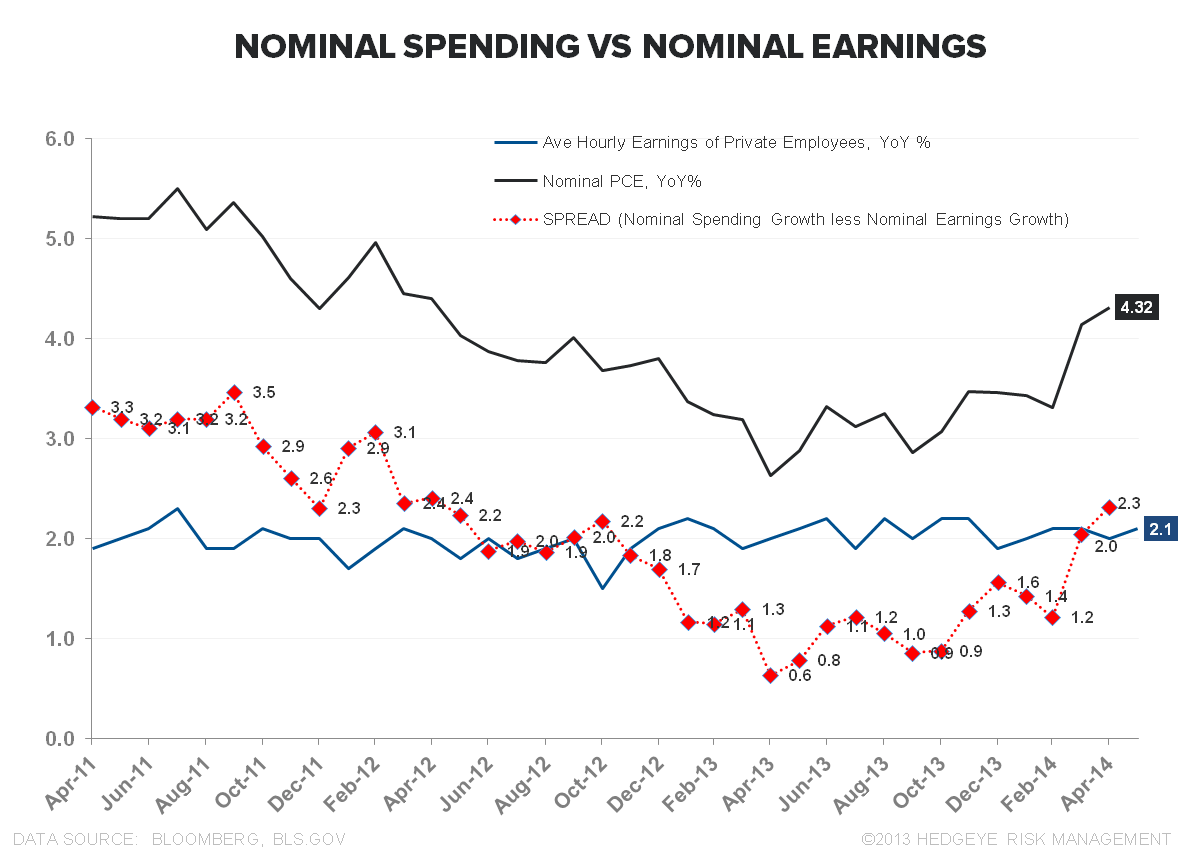

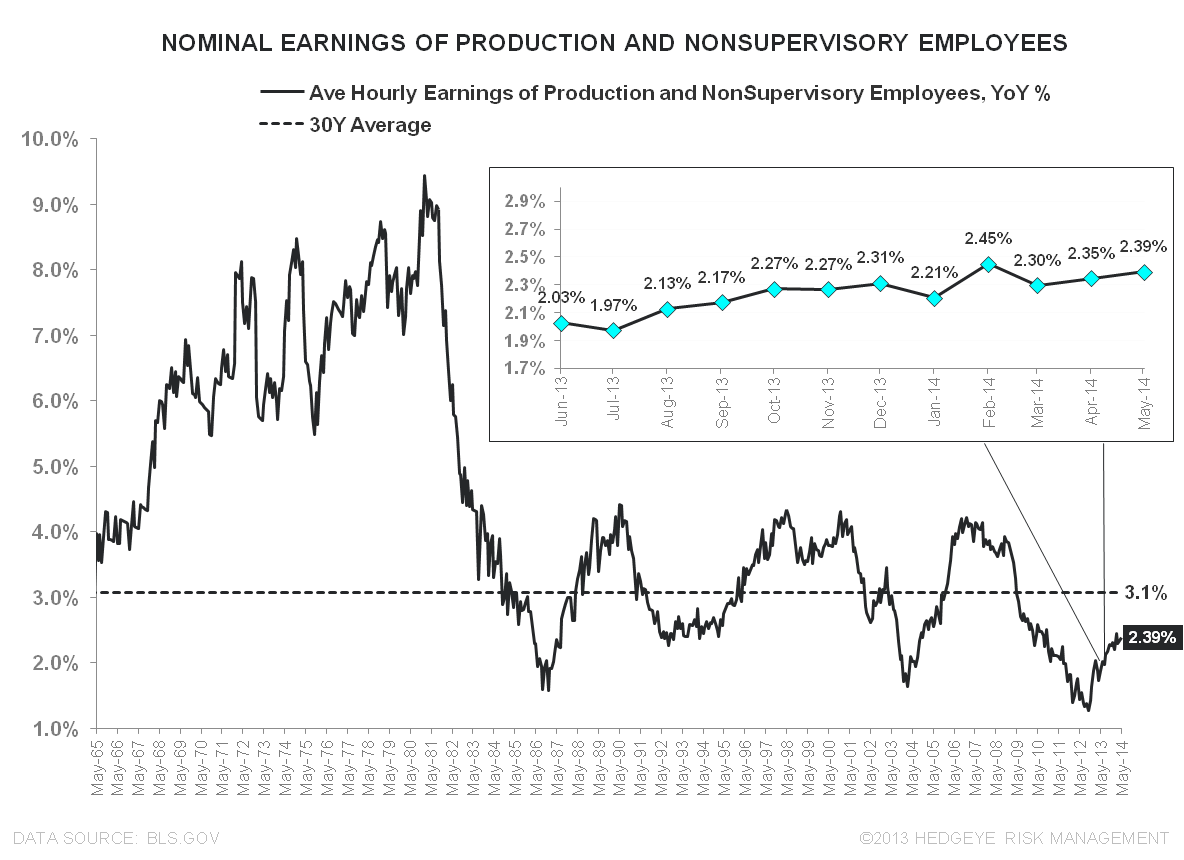

Earnings Growth: Average hourly earnings in the Private sector grew 2.1% YoY, up from +2.0% in April but a continuation of the stagnant 2.0% +/- 20bps that has prevailed over the last two years. Average hourly earnings for Production and Nonsupervisory employees was better, growing +2.4% YoY with the slope on the trend line still positive. (See our prior note for Labor's Bad Bank for a more detailed discussion of labor dynamics).

With earnings growth static and the spread between spending and earnings growth having re-expanded the last couple quarters, we continue to think the upside to consumption growth remains very much constrained in the immediate/intermediate term (see #Gravity: April Consumer Spending for further detail).

THE TICKING CLOCK: At 60 months as of May, the current expansion has now surpassed the mean duration of expansions (59 months) over the last century. We continue to think this reality weighs into the feds policy calculus – they need to get out of QE if only to give themselves the opportunity to (credibly) get back in if need be.

Unemployment Rate: The unemployment rate held at 6.3% in May while the U-6 rate (Unemployed + Marginally Attached + Part-time for Economic Reasons) dropped -10bps to 12.2%. Policy makers look at the spread between the two as a broad measure of labor market slack.

While the percent of LT unemployed and U-6 rate continue their steady, albeit painfully slow, march lower, the U6-U3 spread remained at 5.9% in May - well above longer-term averages which sit closer to ~3.5%

80o and Sunny on tap for the Northeast. Enjoy the weekend.

Christian B. Drake

@HedgeyeUSA