RBA governor Glenn Stevens announced yesterday that the cycle of rate cuts has ended and that the next move by his team will be an increase. With the base rate at a 55 year low of 3%, Stevens has room to maneuver in either direction –unlike Bernanke & Co. (unless they decide to acquiesce to Maxine Water’s call to implement negative rates).

(text continues after chart 1)

Stevens is signaling an unwillingness to wait for inflation to rear its head, choosing to act decisively now before unemployment peaks. This decision is made easier by the relative strength of the economy down under, but the decision still reflects a degree of integrity in the face of political pressure that is wholly alien to the leadership of the United States.

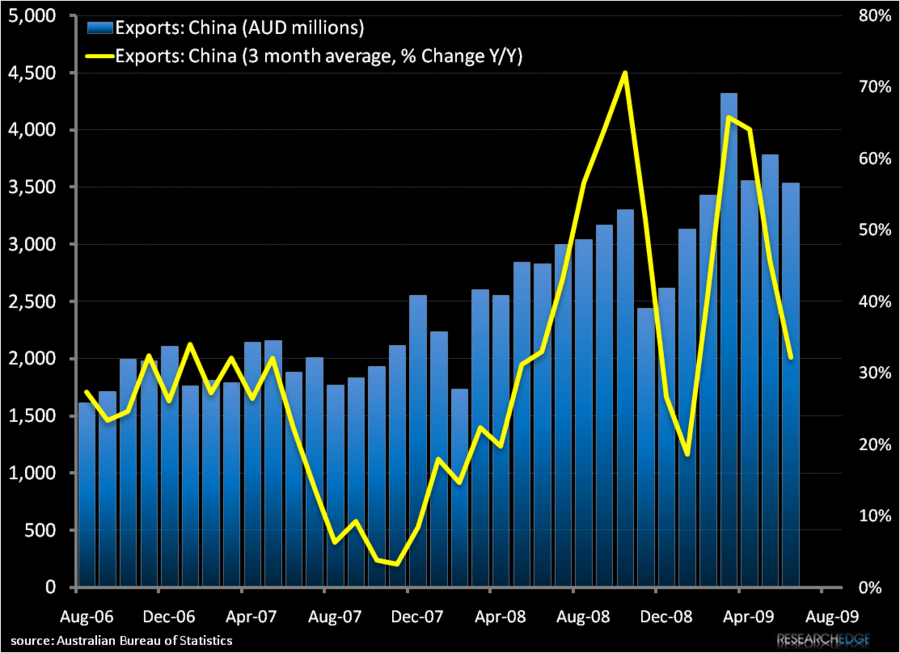

Evidence that Steven’s inflationary concerns are well founded arrived in today’s ABS June trade data release. At -$441 million AUD the deficit was almost half the consensus estimate, a decline driven by an increase in export value rather than volume as spot prices for ore, coal and precious metals continued to reflect increasing Chinese demand. Australia is able to provide “The Client” with both what they need AND what they want and, despite a slowing trajectory, total exports to China grew by double digits on a Y/Y basis for each of the first 6 months of the year.

Although we are not currently long Australian equities or the Aussie dollar, we continue to be bullish on prospects for this well managed economy rich in natural resources feeding off Chinese demand with inflationary tailwinds beginning to blow for core exports.

Andrew Barber

Director