THE STANDOFF: Initial Jobless Claims say the Labor Market continues to improve, 1Q14 GDP & April Pending Home Sales say “escape velocity” remains a panglossian phantasm, and consensus growth expectations continue to sing a sirenic but delusional tune around 2014 growth.

In this morning’s Early Look, ahead of the 1Q14 GDP revision, we made the following remark:

“ Q114 GDP probably wasn’t as bad as the headline and Q214 won’t be as good...taking the average of the two quarters offers the easiest smoothing adjustment and it will show we’re a high 1% economy – which is about right.”

In the wake of the worse than expected revision to reported 1Q growth that still pretty well characterizes our view.

THE CONCLUSION: Labor market trends remain solid, but with housing slowing, inflation rising, earnings growth static (w/ savings rates troughed) and the current level of consumption growth (which sat as the singular source of strength in 1Q14 GDP) overstated and/or unsustainable, we continue to think the currency and debt markets ($USD broken and rates in full retreat) are scoring the immediate/intermediate term growth outlook correctly.

THE DELUSION: Consensus GDP estimates for full year 2014 remain at +2.5-3%, implying 4% growth for the balance of the year. We’d argue the side on which the balance of risk in that expectation sits is fairly conspicuous.

(Note: This morning’s strategy note- Sell #OldWall Polish - reviews how the markets are scoring the data YTD and highlights our view and preferred positioning for the immediate/intermediate term. This morning’s housing note reviews the April Pending Home Sales data - Pending Home Sales Remain Sluggish)

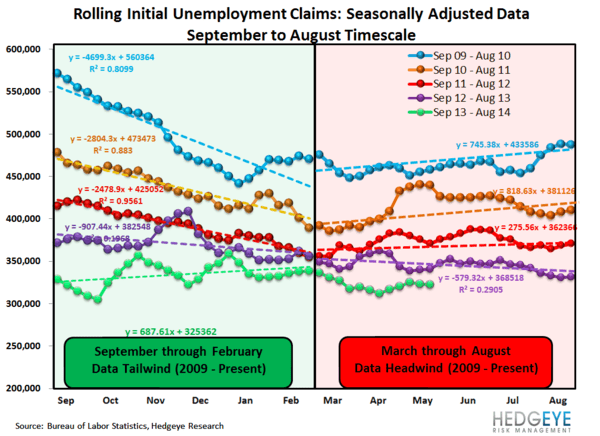

INITIAL CLAIMS: ANOTHER STRONG PRINT

- The Data: Headline claims fell -26k WoW to 300K with the 4-wk rolling average declining -11K WoW to 311.5K. Non-seasonally adjusted claims, which we consider a more accurate representation of the underlying labor market trend, came in at -15% YoY (vs. -5.3% prior) with the 4-wk rolling average improving to -10.4% YoY vs. -5.3% last week.

- The Takeaway: The positive momentum in the labor market along with the broader, sequential improvement in the domestic macro data off the 1Q14 weather distortion suggest no change in the pace of Tapering. The improvement in claims also bodes well for the May employment report. While SA claims reported during the BLS survey period (conducted during the pay period including the 12th of the month) were less good than the most recent weeks figures, on balance, the May claims data is supportive of a good NFP print.

source: Hedgeye Financials

1Q14 GDP (1st Revision): #GrowthSlowing

- Bad But Not A Surprise: The first revision to 1Q14 GDP came in at -1.0%, missing estimates of -0.5%. The magnitude of the revision was larger than expected but the negative print and downward revisions to inventories, exports, & Gov’t spending was not a surprise as the actual march data came in worse than the BEA estimates embedded in the advance GDP report.

- Inventory Drag: The negative revision to inventories was the biggest contributor to the total revision. The inventory ramp, which comprised a big portion of reported nominal GDP growth in 2H13, is now reversing as end demand/income growth proved insufficient at expeditiously drawing down that burgeoning stock.

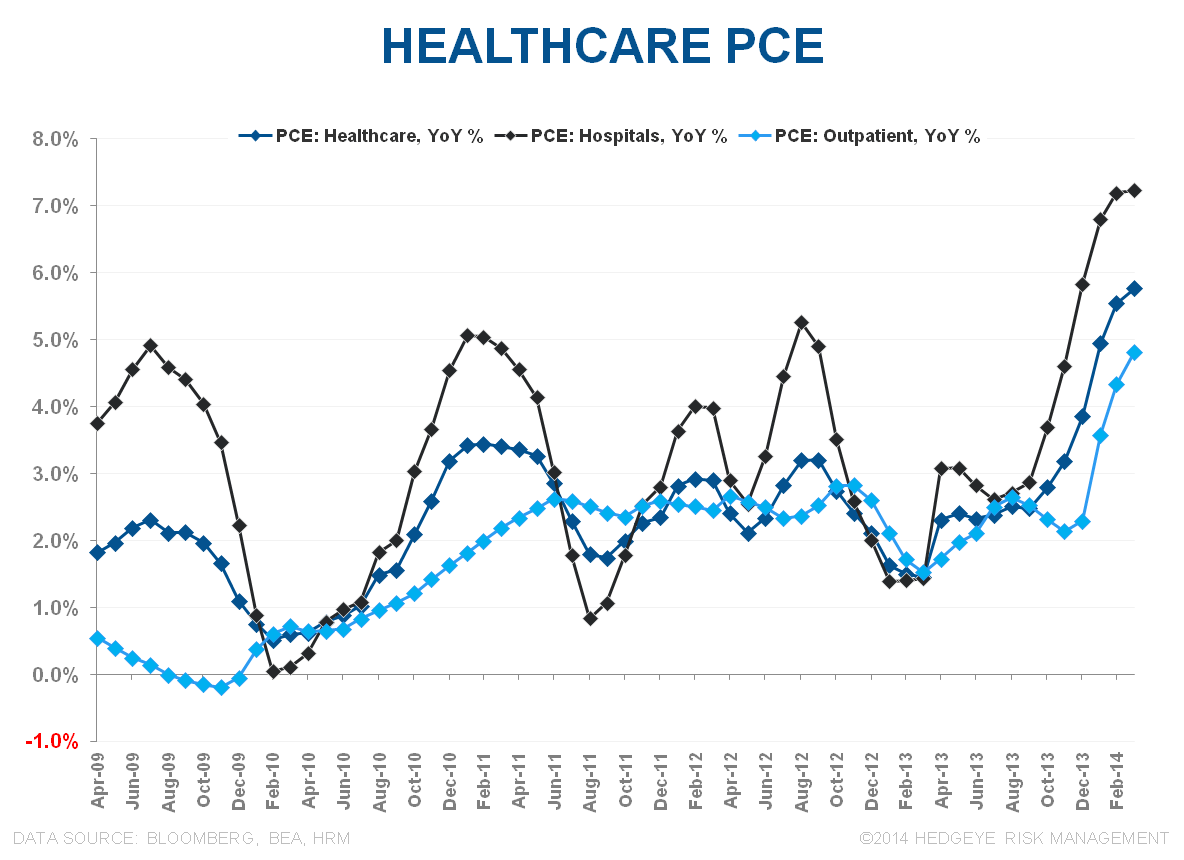

- Consumption: Strength in consumption growth, particularly Services, was the conspicuous positive on the quarter. Notably, Services consumption was supported by the significant acceleration in healthcare spending.

*Healthcare Spending: The strength in Healthcare Services spending stems largely from the implementation of Obamacare. The reported figures, by BEA’s own admission (see their note Here), are very much an estimate and the preliminary data are likely to be revised (significantly) over time as the Census bureau’s quarterly QSS and annual SAS survey’s provide harder data.

With reported Hospital and Outpatient spending both accelerating materially in 1Q14, it could also be that individuals are accelerating medical consumption ahead of ACA implementation and uncertainty around coverage changes.

Either way, in the context of the broader spending data, the takeaway is pretty straightforward – Healthcare Services represent ~17% of total household consumption expenditures and certainly impacts the direction of reported, headline consumption growth. To the extent that deceleration is the larger trend across the balance of services, a mis-estimation of ACA related spending and/or a significant, transient pull-forward in medical consumption could be materially distorting the prevailing, underlying trend.

- Real Final Sales growth (GDP less Inventory Change): decelerating 2.1% QoQ to 0.6%…revised lower by 10bps

- Gross Domestic Purchases (GDP less exports, including imports): Very Weak sequentially. Decelerating 160bps QoQ to +0%..revised lower by -90bps

- Real Final Sales to Domestic Purchasers (GDP less exports less inventory change): Probably the cleanest read on aggregate private sector demand was decent at 1.6% QoQ (flat sequentially)…revised up +7bps.

- So…: Ugly Macro or (now) easy comps – pick your spin!

Christian B. Drake

@HedgeyeUSA