Claims Strong = Rates Down

Yesterday the 10-Year Treasury yield dropped 8 basis points to close at 2.44%, down from 2.52% on Tuesday. In early May, we argued that the Fed's ongoing taper, facilitated by strong labor market data, was indirectly causing downward pressure on long-term rates. This was based on the idea that following the expiration of both QE1 and QE2 we saw 100+ basis points declines in long-term rates.

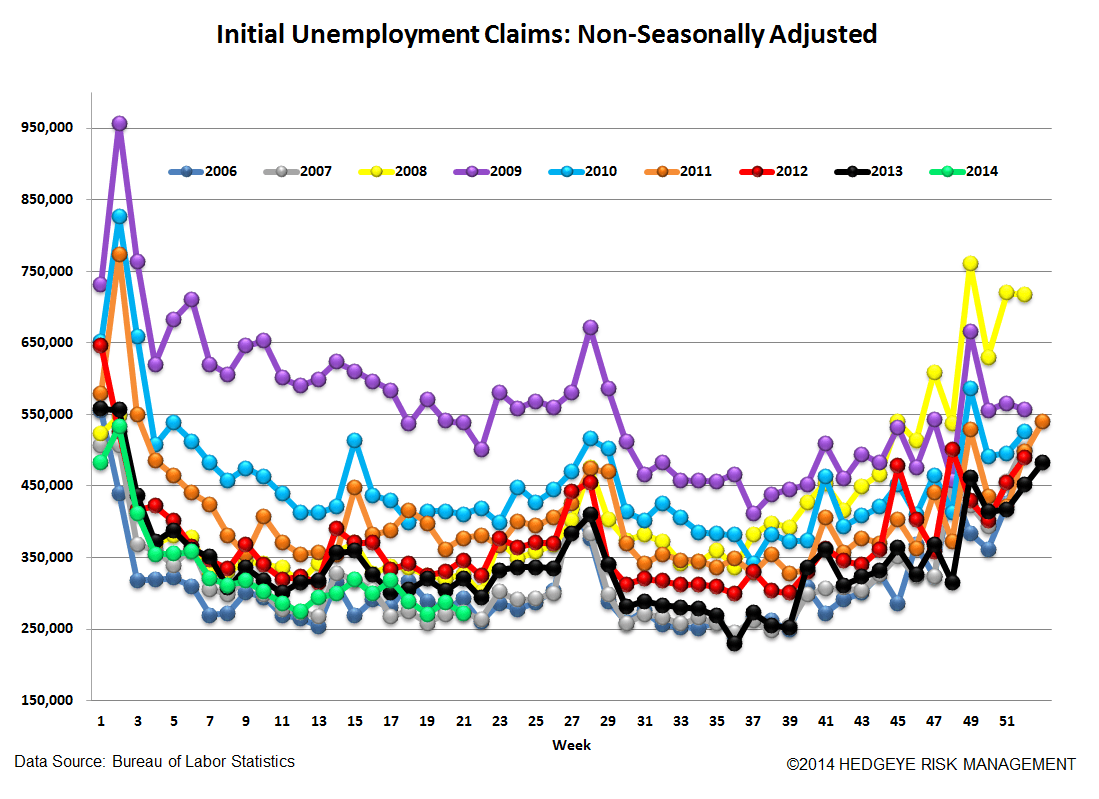

With that in mind, today's initial jobless claims data is very strong, and the ongoing taper of QE3 should continue and, by extension, the ongoing decline in long-term rates should persist over the short/intermediate term. The year-over-year change in NSA initial claims came in at -15% and the four-week rolling average is now lower by 10.4% year-over-year versus the prior week being lower by 5.3%. It's fair to say that this is some of the strongest labor market data we've seen in a while, and it bodes well for next Friday's May labor market report. It's also interesting in the context of the negatively revised 1Q GDP print.

The Data

Prior to revision, initial jobless claims fell 26k to 300k from 326k week-over-week, as the prior week's number was revised up by 1k to 327k.

The headline (unrevised) number shows claims were lower by 27k week-over-week. Meanwhile, the four-week rolling average of seasonally-adjusted claims fell -11k week-over-week to 311.5k.

The four-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -10.4% lower year-over-year, which is a sequential improvement versus the previous week's year-over-year change of -5.3%

* * * * * * *

Editor's Note: This is an excerpt of a research note that was originally provided to subscribers on May 29, 2014 at 9:35 a.m. EST by Hedgeye’s Financials team. Follow Jonathan Casteleyn and Josh Steiner on Twitter @HedgeyeJC and @HedgeyeFIG.