TODAY’S S&P 500 SET-UP – May 29, 2014

As we look at today's setup for the S&P 500, the range is 29 points or 1.14% downside to 1888 and 0.38% upside to 1917.

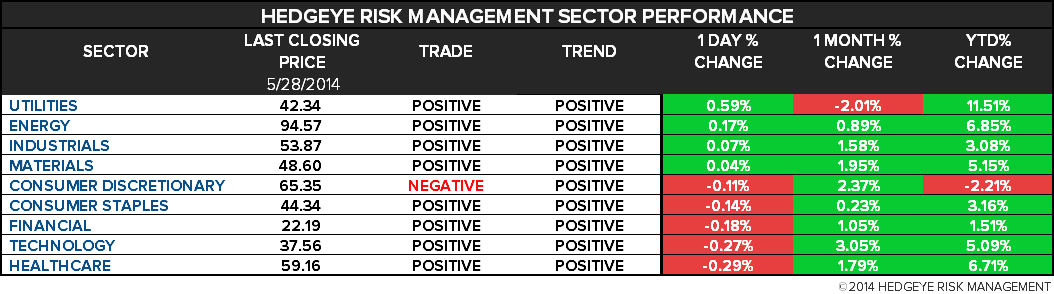

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.07 from 2.08

- VIX closed at 11.68 1 day percent change of 1.48%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: GDP Annualized q/q, 1Q (S), est. -0.5% (prior 0.1%)

- 8:30am: Initial Jobless Claims, May 24, est. 318k (prior 326k)

- 8:30am: Personal Consumption, 1Q (S), est. 3.1% (prior 3%)

- 8:30am: Fed’s Pianalto gives opening remarks at conf. entitled, “Inflation, Monetary Policy and the Public”

- 9:45am: Bloomberg Consumer Comfort, May 25 (prior 34.1)

- 10am: Pending Home Sales m/m, Apr., est. 1% (prior 3.4%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: DOE Energy Inventories

- 9:30pm: Fed’s George speaks at Stanford

GOVERNMENT:

- Push grows for Shinseki to go as report cites veteran-care flaws

- Senate out; House in session

- U.S. Chamber of Commerce Pres. Thomas Donohue speaks at University of Havana; leads delegation of business leaders, including Cargill CFO Marcel Smits, on fact-finding trip

- 11:05am: President Obama to announce public, private commitments to raise awareness about concussions at summit on youth sports injuries

- 1pm: House Small Business Cmte holds hearing on EPA’s “Waters of the United States” rule

- U.S. ELECTION WRAP: Democrats’ Local Strategy; GOP on VA Scandal

WHAT TO WATCH:

- Microsoft, Salesforce said to be discussing cloud partnership

- Apple agrees to buy Beats for $3b in biggest-ever deal

- Ackman looks to raise money from fund listed in London: NYT

- Costco quarterly profit trails estimates even as sales increase

- Google vows to improve diversity after disclosing staffing data

- AIG sees labor-cost arbitrage as jobs move to Philippines, TEX

- Phillips 66 says tribunal supports Sweeny takeover from PDVSA

- Man Group considering purchase of quant money manager Numeric

- RBS said to sell stake in private-equity arm to Adams Street

- Energy Capital hires banks to explore EquiPower sale, IPO: WSJ

- GIC to sell Florida Golf property purchased from Paulson Group

- U.S. states meld zero-emission car plans in drive to sales goal

- Russia urges “emergency steps” on Ukraine after rebel losses

AM EARNS:

- Abercrombie & Fitch (ANF) 7am, $(0.19) - Preview

- CIBC (CM CN) 5:50am, C$2.02 - Preview

- Fred’s (FRED) 7:45am, $0.20

- Pall (PLL) 7am, $0.83

- Sanderson Farms (SAFM) 6:30am, $1.70

PM EARNS:

- Avago Technologies (AVGO) 4:05pm, $0.77

- Express (EXPR) 4pm, $0.14

- Guess (GES) 4:03pm, $(0.07)

- Infoblox (BLOX) 4:05pm, $0.03

- Lions Gate Entertainment (LGF) 4:01pm, $0.43

- OmniVision Technologies (OVTI) 4:25pm, $0.26

- Pacific Sunwear (PSUN) 4pm, $(0.13)

- Splunk (SPLK) 4:02pm, $(0.06)

- Veeva Systems (VEEV) 4:05pm, $0.05

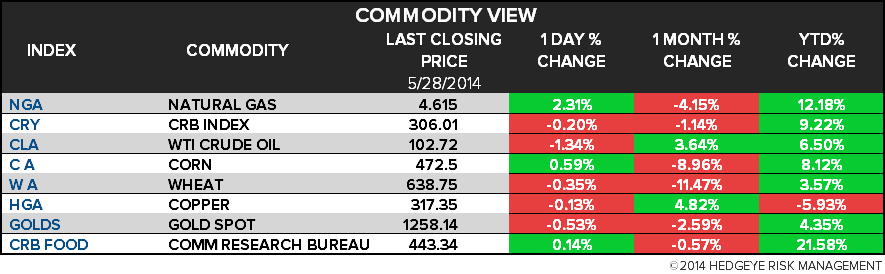

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Trades Near One-Week Low After Stockpiles Grow; Brent Steady

- Sugar Output in Thailand Seen Climbing to Record as Area Expands

- Cocoa Shortage Looms as Growers Opt to Farm Rubber: Commodities

- Gold Falls to 16-Week Low as Palladium Near Highest Since 2011

- Copper Drops From 11-Week High as Investors Capitalize on Gains

- Corn Heads for Biggest Monthly Drop Since June on Sowing in U.S.

- Sugar Bounces With Newfound Demand After Losses; Coffee Advances

- Scrap Copper Imports by China Seen Recovering With Refined Price

- Nickel Pig Iron Output Costs in China Seen Surging as Ore Jumps

- Blackstone Unit Foreshadows Google Path to Power Company: Energy

- Minister’s Platinum Strike Plan Seen Unlikely to Bring Quick End

- Birthplace of USS New Jersey Saved by Shale Production: Freight

- London Bullion Market Gold Fix May Go the Way of Silver

- Steel Rebar Falls as Iron Ore Price Drops to Lowest Since 2012

CURRENCIES

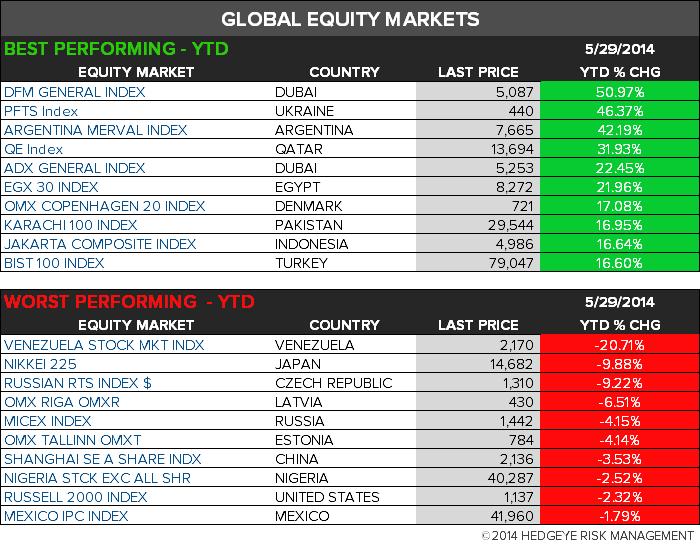

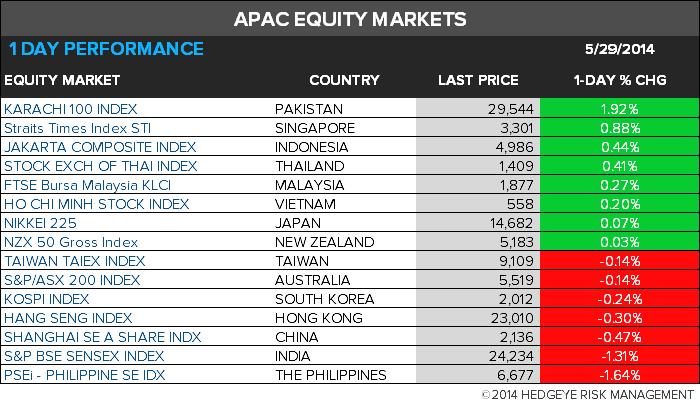

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team