TODAY’S S&P 500 SET-UP – May 27, 2014

As we look at today's setup for the S&P 500, the range is 28 points or 1.19% downside to 1878 and 0.29% upside to 1906.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

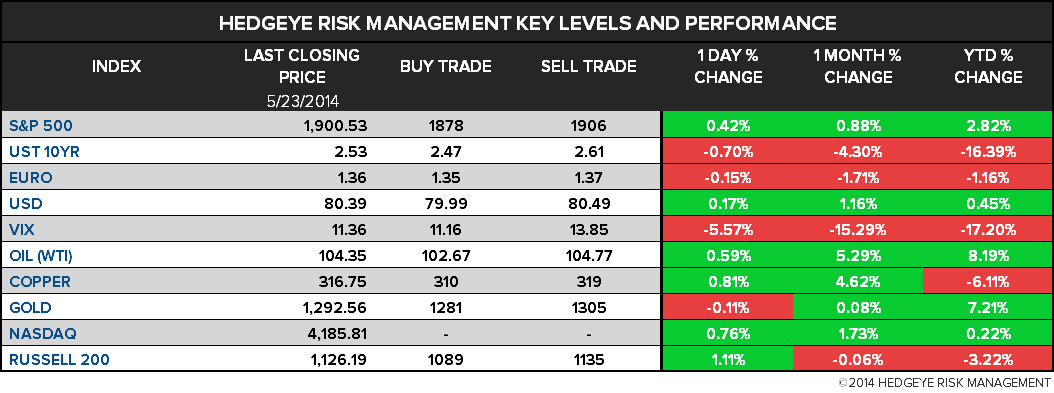

- YIELD CURVE: 2.19 from 2.19

- VIX closed at 11.36 1 day percent change of -5.57%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Durable Goods Orders, Apr., est. -0.7% (prior 2.9%, revised from 2.6%)

- 9am: FHFA House Price Index m/m, Mar., est. 0.5% (prior 0.6%)

- 9am: S&P/CS 20 City m/m SA, Mar., est. 0.7% (prior 0.76%)

- 9:45am Markit US Composite PMI, May (P) (prior 55.6)

- 9:45am: Markit US Services PMI, May (P), est. 54.5 (prior 55)

- 10am: Consumer Confidence Index, May, est. 83 (prior 82.3)

- 10am: Richmond Fed Manufact. Index, May, est. 5 (prior 7)

- 10:30am: Dallas Fed Manf. Activity, May, est. 9.2 (prior 11.7)

- 8:10pm: Fed’s Lockhart speaks in Baton Rouge, La.

GOVERNMENT:

- Obama lands in Afghanistan for unannounced visit with troops

- White House inadvertently exposes Afghan CIA Chief: WPost

- Supreme Court may issue opinions

- Senate, House not in session

- Washington Week Ahead: Obama to deliver address at West Point

WHAT TO WATCH:

- Pfizer weighs next move as $117b AstraZeneca bid ends

- China said to push banks to remove IBM servers in spy dispute

- GE seeks consent in pledge to keep Alstom nuclear ops in France

- GE’s Immelt, Siemens’s de Maistre at hearing in France

- Fox’s X-Men sequel topples Godzilla through holiday weekend

- Sony forms China Playstation venture in Microsoft challenge

- Twitter is getting bigger in Asia amid slowing U.S. user growth

- InterContinental jumps after report co. spurned bid approach

- ICE plans Euronext IPO, to list in Paris, Amsterdam, Brussels

- China Hangzhou asks Lilly, AstraZeneca for self-checks: Herald

- BofA said to find error after change in Fed wording: WSJ

- Apple seeks order blocking sale of some Samsung smartphones

- Germany plans Google entries’ mediation service: Handelsblatt

- Google said to consider acquiring Dropcam: The Information

- Russia, Ukraine draft gas debt plan as price dispute unresolved

- Lloyds plans initial public offering for TSB banking division

- EU austerity rethink demanded as leaders meet post protest vote

- Poroshenko triumphs in Ukraine vote as Russia open to talks

EARNINGS:

- Autozone (AZO) 7am, $8.45

- National Bank of Canada (NA CN) 6pm, C$1.04 - Preview

- Qihoo 360 (QIHU) 5pm, $0.35

- Scotiabank (BNS CN) 6am, C$1.31 - Preview

- Wet Seal (WTSL) 4:05pm, ($0.18)

- Workday (WDAY) 4:02pm, ($0.15)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Trades Near Four-Day Low After Ukraine Vote; WTI Steady

- Russian Palladium Flows to Switzerland Jump on Sanction Concerns

- Solar Farmers in Japan to Harvest Energy With Crops: Commodities

- Copper Touches an 11-Week High on Outlook for Stimulus in China

- Corn Slumps to 12-Week Low as U.S. Planting Progress Accelerates

- Cocoa Climbs to Highest Since 2011 as Robusta Coffee Declines

- Gold Falls to Two-Week Low in London as Ukraine Outlook Weighed

- Cocoa Climbs 0.6% to $3,040/T, Highest Since September 2011

- Rebar Rises to 2-Week High on Optimism China Economy Improving

- Ukraine Drafts $2.5 Billion Russia Gas Debt Plan to Avoid Cutoff

- Platinum Producers to Meet With Judge Mediating Strike Talks

- Shakeout Threatens Shale Patch as Frackers Go for Broke: Energy

- Russian Gas Reliance in European Union Skews Sanctions Debate

- COMMODITIES DAYBOOK: Solar Farmers in Japan to Harvest Energy

- China’s April Gold Imports Drop Amid Lower Investment Demand

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team