This note was originally published at 8am on May 12, 2014 for Hedgeye subscribers.

“There is hardly a part of the United States where men are not aware that secret private purposes and interests have been running the government.” –Woodrow Wilson

I had a fantastic Real Conversation (HedgeyeTV video here: https://www.youtube.com/watch?v=hN7-u7Sd7Gk) with best-selling author Jim Rickards last week. Since he suggested we “quarantine the Princeton Economics Department”, I figured I’d quote the 28th US President (who was also President of Princeton).

Princeton is a cool place; especially if you go there wearing Blue and White and crush their Tigers at the Hobey Baker rink. While that may be easier for more recent Yale Hockey teams to do, back in my day Princeton was as tough as any team in the league.

There was tough love for the Keynesians in my conversation with Rickards. We talked about the broken Fed model and how the US government doesn’t think about financial market risk the right way. The feedback on this video has been tremendous. Evidently this taps into a new reality – The People Are Aware.

Back to the Global Macro Grind…

People in our profession are also very much aware of the real-time score on US Growth expectations falling, fast:

- Russell 2000 down another -1.9% last week to -4.8% YTD

- Nasdaq down another -1.3% last week to -2.5% YTD

- US Consumer Discretionary Stocks (XLY) down another -0.6% to -4.5% YTD

But, but, the Dow “hit an all-time high” on Friday (which puts it dead flat on the YTD #joy). So make sure you own everything in the Dow that is:

- Slow-growth

- Low-beta

- High-Yield

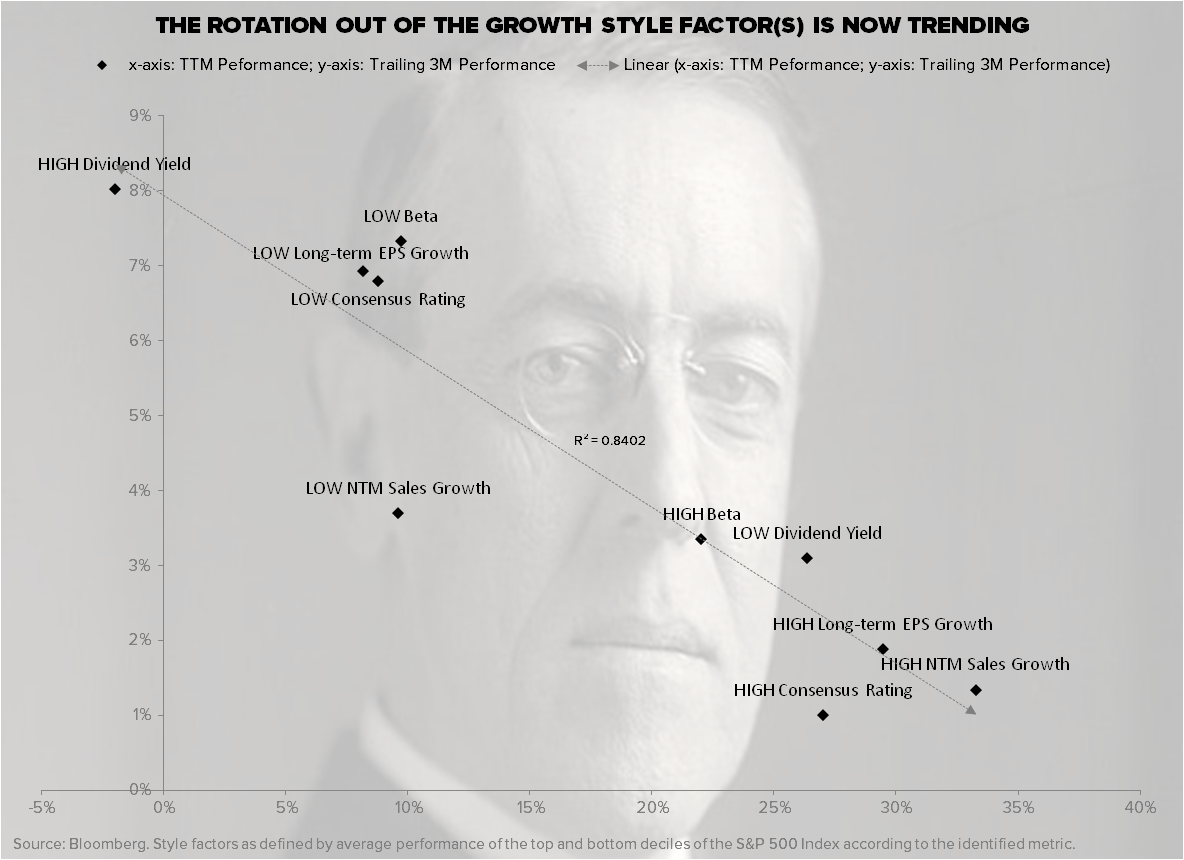

But you already have that on because that has been the strategy and asset allocation decision to make for the last 4.5 months. While that may not be trivial to someone who hasn’t evolved their process, in modern day markets real-time risk managers look at what we call Style Factors:

- Slow-growth stocks (Bottom 25% of the SP500’s EPS Growth is +5.2% YTD)

- Low-beta stocks are +6.1% vs High-beta up a paltry +0.4% YTD

- High-dividend-yielding stocks are +3.9% for 2014 YTD

“So”, what is driving slower-growth-hamster-on-the-wheel #YieldChasing? That’s too easy. It’s the Fed’s Policy to Inflate:

- So you buy inflation protections via TIPs

- Or you buy inflation by buying inflation itself (Oil, Food, Gold, etc.)

- Or you buy bonds and/or anything that looks like a bond as slower-growth-expectations drive down interest rates

Of course you’d have to let go of most academic ideologies that bonds don’t do well during #InflationAccelerating, and embrace that the Bernanke/Yellen Fed has 0% credibility on fighting inflation. I don’t know how many more times I can rant about this in print – that’s why I went to the video!

How about that stuff the Fed calls “non-core” (like ripping US rents and food) last week?

- CRB Foodstuffs Index up another +0.6% last week to +23.7% YTD

- Soybeans up another +1.1% to +11.6% YTD

- Corn up another +1.6% to +16.1% YTD

Yep. If you don’t like that definition of #InflationAccelerating, eat a REIT – and like it. Last week the MSCI REIT Index was up another +1.2% to +14.1% YTD, which means that you can bet your Madoff that rents are going higher in this country, not lower.

Oh, did I mention being long of US Housing in housing and/or related construction stocks terms (ITB) sucked wind again last week? For some reason this and most of the aforementioned market realities didn’t make it into Hyman’s weekly update. ITB (Housing) is down -6.4% YTD.

But never mind what Old Wall economists who missed calling the Q1 08’ and Q1 11’ slowdowns in US consumption growth think. As the early response to my un-plugged video with Rickards reminds us, The People Are Aware now. And that’s progress.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.56-2.67%

SPX 1869-1889

RUT 1189-1117

USD 79.18-80.08

EUR/USD 1.37-1.39

Gold 1278-1314

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer