Welcome to The Hedgeye Housing Research Vertical

Yesterday we introduced our Hedgeye Housing Vertical research product. The effort is being led by Josh Steiner and Christian Drake from the Financials and Macro teams. Subscribers to Financials and/or Macro verticals are currently set up to receive this product. If you'd prefer not to receive our housing-focused research going forward please let us know.

Our goal is to help investors understand the trends and spot inflection points in the US housing market by tracking 15-20 different housing data series and presenting them in a hyper-simple format. Whenever data hits we will publish a brief note summarizing its importance, or lack thereof. Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

We've broken the market into four main categories: Home Prices, the existing home market, the new home market, and other miscellaneous data. The focus is on simple supply and demand measurements and whether they're weakening or strengthening, on the margin. We're using red and green to make it easy for investors to gauge, at a glance, whether there's widespread improvement, deterioration or a mixed bag.

As the housing research effort evolves we hope you'll engage us with questions and feedback.

Today's Focus: April Housing Starts & Permits

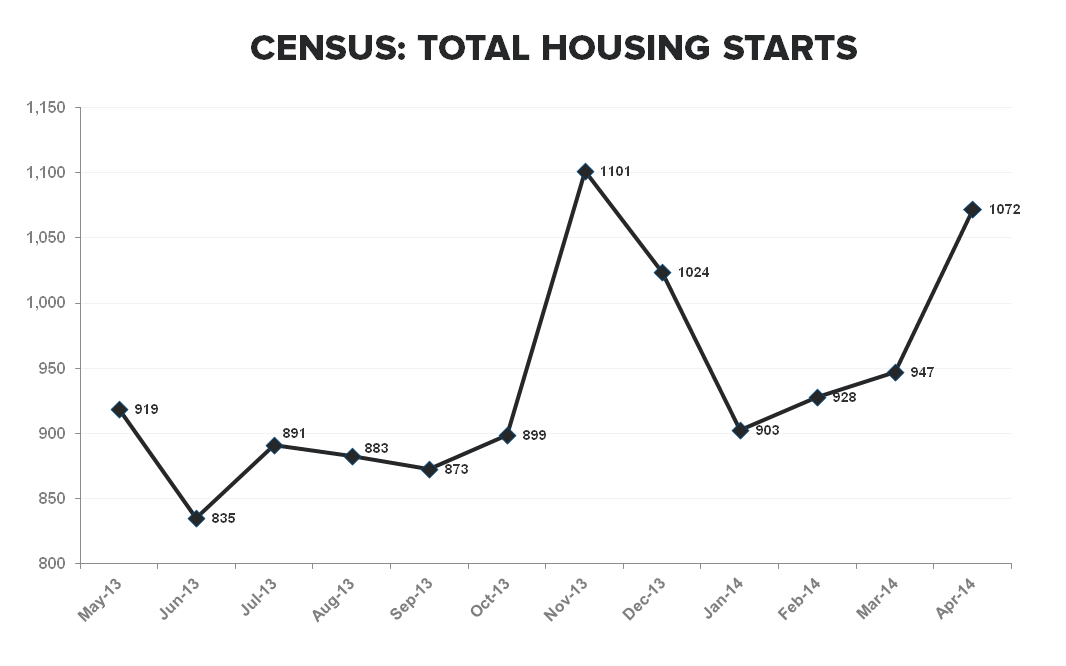

The Census Bureau released its monthly Housing Starts & Permits data for April this morning. The big takeaway is this: don’t be fooled by the headline.

While total starts and permits bounced sharply in April vs March, the bounce was entirely attributable to multifamily. Single family starts and permits did not show any bounce from normalizing weather and continue to show slug-like progress in renormalizing back to pre-crisis levels. Multifamily starts and permits remain strong and are showing a nice, weather-related bounce, suggesting that rental demand continues to benefit from the conjunction of a strengthening labor market, ongoing household formation and QM’s negative effects on would-be first-time buyers.

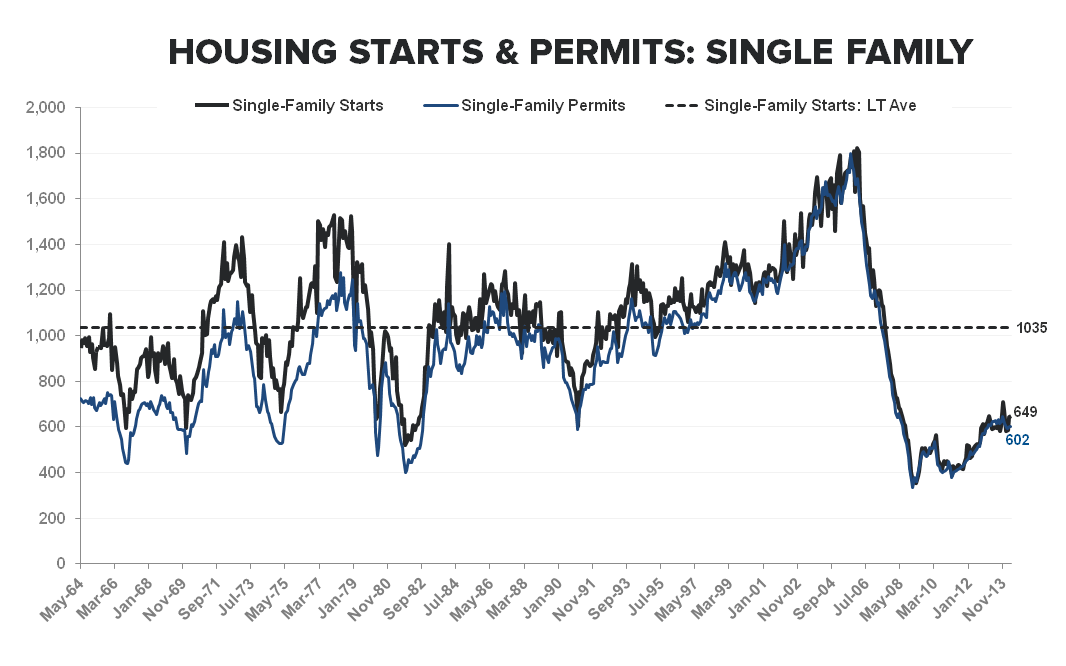

Taking a look at the data, single family starts grew 5k month-over-month or 0.8% to 649k, while single family permits grew 2k, or 0.3% m/m to 602k. Multifamily starts, however, grew by an impressive 120k m/m (+39.6%) to 423k and permits were up 78k m/m, or +19.5% to 478k. Said differently, multifamily accounted for 96% of the growth in Starts and 98% of the growth in Permits month-over-month.

One interesting observation is the apparent trendline divergence between LTM SF starts and permits. Take a look at the first chart below. SF starts are exhibiting a positive upward slope, but permits are showing the opposite. Permits, by definition, lead starts, so the lack of any upward trajectory in permits should tamp down expectations for a coming bounce in starts.

Yesterday’s soft NAHB HMI print of 45 taken with today’s soft single family data paints an ongoing picture of a housing market that continues to stumble through the first half of 2014. Interestingly, these most recent two data points reflect the new home market, which is actually faring better than the existing home market due to the slightly higher affluence of the average buyer.

We think three factors are principally responsible for this weak 1H14 performance. First, QM rules that took effect on January 10 of this year are having a suppressing effect on credit availability. Second, institutional investor demand for properties is waning sharply. Third, affordability dynamics have swung sharply; whereas 12-18 months ago there was a strong asymmetry favoring homeownership, today renting vs owning are close to a toss-up.

About Housing Starts & Permits:

The US Census Bureau records the number of new housing units that have obtained permits for construction and those that have begun construction. This data includes new buildings intended primarily as residential units. The US Census Bureau defines a start as, “Start of construction occurs when excavation begins for the footings or foundation of a building.”

Joshua Steiner, CFA

Christian B. Drake