Japanese trade and production data released today showed sequential improvement in June with Production up 2.4% M/M while shipments improved by 3.5% for the month. Total exports showed a sequential improvement on a year-over-year basis but, at -37.78% (SA), external demand for Japanese goods remains weak.

As domestic Japanese investors are focused on the upcoming election and calculating the prospects for the economy under a post-LDP regime there may well be opportunities for optimism. Anticipated new stimulus measures for 2010, implemented either by the presumptive Democratic victors or LDP underdogs, combined with signs of bottoming in production and exports will likely be welcomed as a potential tonic for the current stagnation (regardless of increased debt levels resulting from increased government spending).

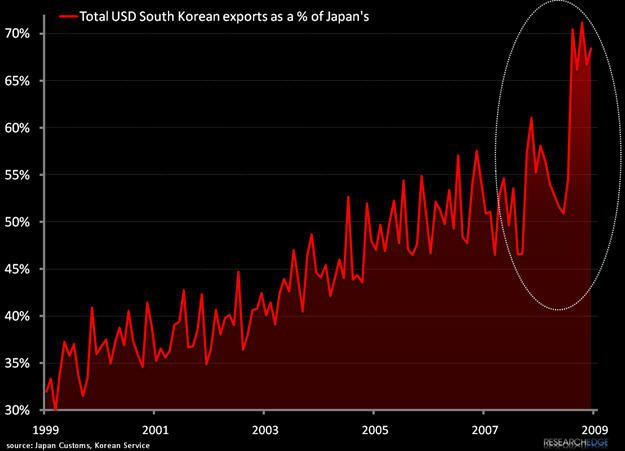

Our view is that any recovery for exporters will be more difficult than some anticipate. In the chart below we have illustrated total USD exports from South Korea as a percentage of Japanese exports. If we were to create similar charts for the other regional rival economies the trend would be similar. With proficient quality Korean automotive and industrials, Taiwanese consumer electronics producers and other competitors stealing market share it is presumptuous to expect that Japan can simply reclaim those lost markets simply by waiting for a global recovery.

We continue to believe that recovery in Japan will lag the other major Asian economies, and that an ultimate day of reckoning will be forced by massive public debt and deteriorating demographics. In the near term, the hollow promises of political candidates and a weak yen are the most likely positive catalysts for Japanese equities in the near term.

Andrew Barber

Director