SUMMARY BULLETS

-

1Q14 Review: Solid quarter, 2Q14 guidance above consensus, 2014 guidance raised in excess of 1Q14 beat

- Beat, Raise, Sell-Off (Again): We covered our short on expected 1Q14 upside. That was a mistake; street was expecting 1Q14 upside comparable to what TWTR produced in 4Q13.

-

It Only Gets Tougher From Here: Consensus estimates are rising, and the street expects upside on top of that. That becomes less likely in 2H14/2015 when the monetization tailwind slows.

-

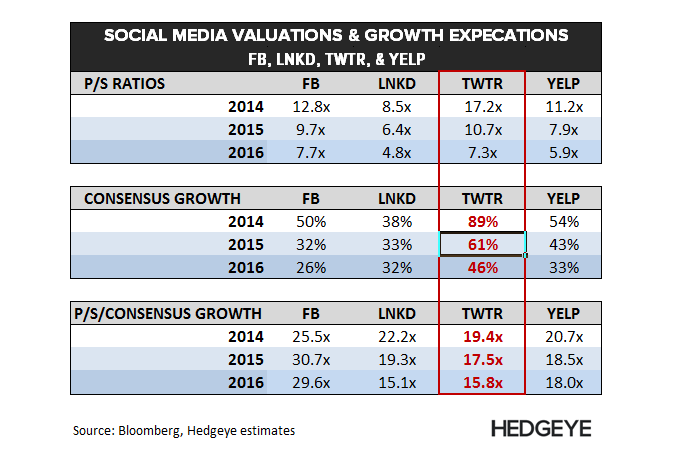

$25 Stock?: We're expecting revenues to slow materially in 2H14, and particularly 2015 (43% vs. consensus of 61%). Based on our growth-adjusted P/S analysis, TWTR shouldn't be trading above $25

-

Supporting Research: See notes below for supporting detail on our short thesis. We are in the process of refreshing or slide deck.

1Q14 Review

- Revenues: $250.5M vs. consensus of $241.5. 1Q14 Ad revenue growth (y/y%) accelerated vs. 4Q13 both globally (up 125% vs. 121%, respectively) and in the US (106% vs. 97%)

- User Growth: US was up 19% y/y vs. 20% in 4Q13. Global up 25% vs. 30% in 4Q13. Int’l slowed to 27% in 1Q14 vs. 34% last quarter.

- Engagement (timeline views/user): Decelerated globally, decline moderated in the US (-2% vs. -5% in 4Q13), deteriorated internationally (-10% vs. -2%).

- Monetization (ad revenue/timeline view): Accelerated sharply globally (96% vs. 76%), mostly driven by int’l, but US improved as well (78% vs. 73%).

- Guidance: 2Q14 revenue of $270-$280 vs. consensus of $272. Raised 2014 range by $50M to $1.20B-$1.25B, ahead of the beat on 1Q guidance

BEAT, RAISE...SELL-OFF (AGAIN)

We covered our Short prior to the 1Q14 release. We believed street expectations had rebased following the sell-off on its 4Q13 release. Given the upside we saw to 1Q14 consensus estimates, and that our bearish fundamental view centers around 2H14/2015, we decided to get out of the way looking to reshort at a higher price. That was a mistake.

Despite a very solid quarter and 2014 guidance raise, the stock is down 10% today. We suspect this is tied to the smaller magnitude of the 1Q14 beat and guidance raise in relation to what TWTR produced in 4Q13.

IT ONLY GETS TOUGHER FROM HERE

TWTR is in a precarious setup. Every time TWTR beats estimates, consensus estimates move higher. However, street expectations differ from consensus: TWTR is expected to continue to beat those increasing estimates, and guide higher.

We continue to expect a dramatic slowdown in revenue growth into 2H14, and particularly 2015 (see notes below for supporting detail). Our bearish fundamental view vs. rising consensus & street expectations suggest the setup will only get worse from here.

In short, the hurdle keeps moving higher while its growth prospects get progressively worse.

$25 Stock?

TWTR is trading at a premium to its Social Media peers given heightened growth expectations. Consensus is assuming 61% revenue growth in 2015. We're expecting 43% growth as its monetization tailwind slows precipitously into 2H14 and 2015.

In turn, TWTR's 2015 growth profile is similar to what the street is assuming for YELP, which trades at 7.9x 2015 revenues vs. the 10.7x that TWTR is trading at today. That said, TWTR shouldn't be trading at any more than 8x 2015 revenues, which translates to a $25 stock; and that assumes the Social Media space can maintain its lofty P/S multiples.

SUPPORTING RESEARCH

See the notes below for detail on our short thesis. If you would like to see our TWTR short deck (update in progress), or have any questions, please let us know.

TWTR: Covering Short...For Now

03/10/14 11:41 AM EDT

http://app.hedgeye.com/feed_items/34021

TWTR: Staying Short, But...

02/07/14 04:55 PM EST

http://app.hedgeye.com/feed_items/33438

Hesham Shaaban, CFA

@HedgeyeInternet