SUMMARY BULLETS

- Pressure to Build Through 2014: One of the major risks facing YELP in terms of both attrition and new client growth is the sharp rise in commodity costs, which has seen its sharpest sequential increase since 2011. SMBs will be hit hardest, making adverting expenditures tougher to swallow.

- Today's Strength = Tomorrow's Weakness: YELP is losing virtually all its clients annually, meaning it must continually to sign more new clients in excess of what it starts the year with in order to drive growth. That said, it's current client base will always be its future hurdle; the larger that is, the larger the hurdle, the lower it's future growth. Given a shrinking TAM, that's a scary prospect.

Pressure to Build Through 2014

We're not seeing as much risk to 1Q14 Revenues; largely because what we've seen in terms of macro pressure didn't begin until mid February, which was after the company issued 2014 guidance (2/5/14). That said, the backdrop has materially deteriorated since then, and will only get worse through 2014.

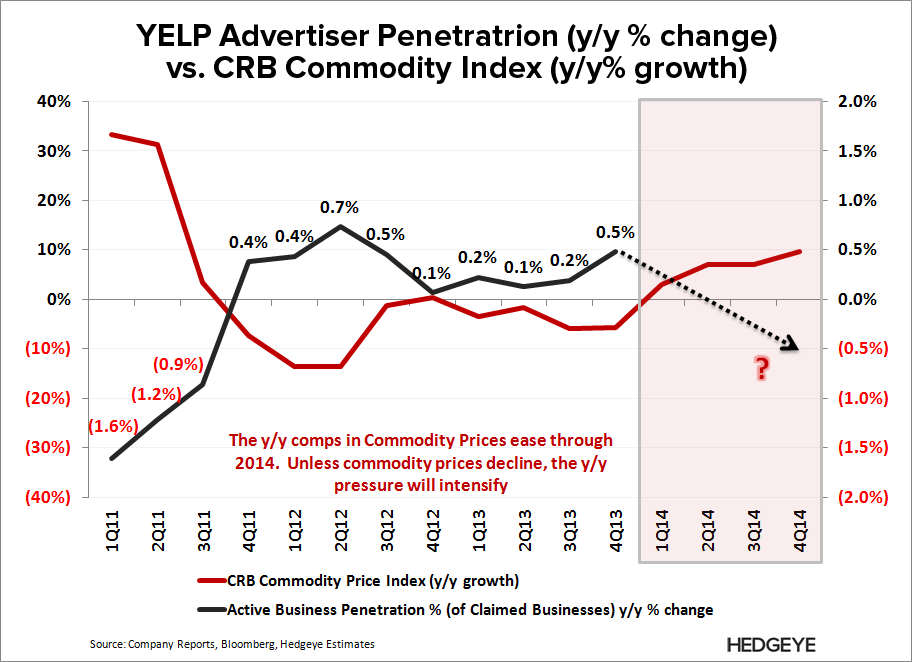

We previously pointed out the sensitivity of YELP's customer penetration levels to commodity prices in our YELP Short Best Ideas presentation. Dating back to 1Q11, the y/y change in customer penetration levels is almost perfectly inversely correlated (-.93) with the change in commodity prices on a y/y basis.

The point is that SMBs see a disproportionate impact from rising input costs given lower economies of scale. In turn, advertising expenditures become increasingly discretionary when the SMB P/L is under pressure.

The CRB index has seen its sharpest sequential increase since 2011; most of that acceleration occurring after the company issued guidance. More importantly, commodity comps ease throughout the year, so unless commodity costs decline materially, the y/y pressure will intensify.

Put another way, as we move through the year, each SMB that is debating whether to renew its contact with YELP will be in a progressively worse situation than it was when it initially decided to advertise with YELP.

Today's Strength = Tomorrow's Weakness

YELP loses virtually all its clients annually, meaning it must continually sign more new clients in excess of what it starts the year with in order to drive growth. That said, it's current client base will always be its future hurdle; the larger that is, the larger the hurdle, the lower it's future growth.

The sad truth is that YELP's current year strength will become next year's weakness since it can't hold on to its customers, and it's addressable market is much smaller than many believe (see note below more detail). In turn, the stronger YELP's 1Q14 revenues, the more bearish we become.

We provide more detail on our short thesis in the note below, and far more detail in our YELP Short Best Ideas Slide Deck. For a copy, or to discuss our thesis in more detail, let us know.

YELP: Death of a Business Model

04/04/14 10:05 AM EDT

http://app.hedgeye.com/feed_items/34518

Hesham Shaaban, CFA

@HedgeyeInternet