Below are Hedgeye analysts' latest updates on our EIGHT current high-conviction investing ideas. We also feature three research notes from earlier this week which offer valuable insight into the markets and two particular stocks.

*Please note we removed CCL from Investing Ideas this week..

*We will send CEO Keith McCullough's updated levels for each stock in a separate email this weekend.

HEDGEYE CARTOON OF THE WEEK

IDEAS UPDATES

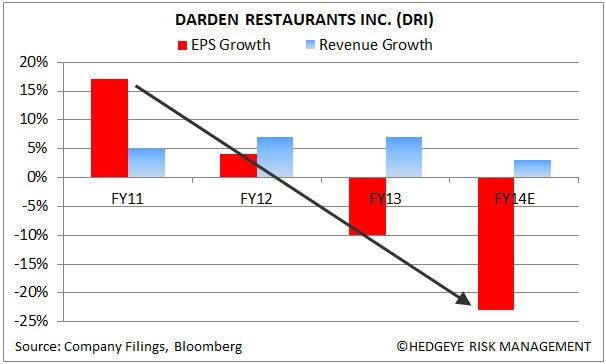

DRI – Managing Director Howard Penney got the news he was looking for on Tuesday, when Starboard Value LP announced it had secured enough votes to call a special shareholder meeting. The goal of this meeting is to stop the proposed Red Lobster spinoff which would potentially destroy significant shareholder value. Darden will have 60 days to call the meeting.

Starboard reportedly received 55.5% of the vote. Although this may look like a slim margin of victory, it is actually quite overwhelming considering the turnover since the record date, the amount of shares short and the retail component. Starboard Managing Member, Chief Executive Officer and Chief Investing Officer, Jeffrey C. Smith, was very clear about what he believes needs to happen at Darden. According to him, Mr. Otis is in a hot seat and deservedly so – just look at the chart below. Many have remarked that Mr. Otis is losing control of the company; ironically, that just took on a whole new meaning.

Although we may see some near-term volatility as this situation plays out, we remain bullish on Darden as a long-term investment.

HCA – We had flagged rising surgical case volume as a near term reason to remain positive on HCA Holdings coming out of their Q413 earnings. We had specifically noted the acceleration in US Orthopedic sales and what appeared to be a durable relationship with some of our macro data series.

Fast forward to UHS results on Friday and that looks like the right bet. This week both SYK and ZMH put up some decent numbers in their US franchises, although trends slowed modestly. Meanwhile, UHS in talking about a 6.3% increase in revenue per adjusted admission cited ”strengthening surgical volumes,” and fewer “uninsured patients and more Medicaid and commercial insurance patients.” UHS tells us a lot about HCA ahead of their release next week where we are now more convinced we’ll see some upside to numbers. In the chart below you’ll see the same-store revenue per adjusted admission growth rate for the two companies. Coming into hospital earnings the concerns have been the foul weather of Q114 and the Affordable Care Act not delivering much upside. Our data suggested weather was less of an issue than feared and the Affordable Care Act is not the most important driver. Turns out we were right to focus on surgical volume.

HOLX – We believe Hologic will have a good quarter in their Breast Health segment driven by Digital Breast Tomosynthesis products, when they report earnings. We’ve developed a proprietary way to track placements month to month and the March quarter looks like their best yet. There is plenty of noise in their other businesses these days to keep in perspective, however.

The first was this week’s approval of Roche’s HPV test as a first line screen for cervical cancer. Traditionally the Pap test, which HOLX dominates with their ThinPrep test, has been the first line screen which is then followed by an HPV test for confirmation. In some ways it makes more sense to screen for cervical cancer by looking directly for the virus that causes the disease first and then do the Pap test if the patient tests positive. The problem however is that HPV infection is really common, particularly among sexually active women, and is usually harmlessly cleared by the body. The point is that sorting this out will take a very long time. OB/GYNs are already coping with guideline changes for the recommended interval between negative test result. ThinPrep volume is already down in the mid teens and becoming less important by the quarter. We’re following this closely with a monthly survey, so we should see it coming if things get even worse from here, but we doubt that will happen.

Which brings us back to Breast Health and the DBT trend. After speaking to a number of experts in the field recently we are getting more confident that the reimbursement Medicare will give DBT this Fall will be high enough to drive a rapid adoption of DBT. In the short run, we are keeping our eye on negative news items such as the Roche HPV approval, but we’re also keeping it in perspective. We think the story is DBT and we think they’re having a good quarter.

LM – We have no material update on our recommendation of Legg Mason as a core long for retail investors. We think that the theme of getting exposure to a defensive bond manager is slowly making its way into the asset management stocks as Legg is the only positive performer in the group year to date. LM stock is up 5.5% thus far in 2014 versus the group average of a decline of 4.4%. We estimate that Legg shares are worth over 20% higher than current prices on an intermediate to long term basis as we see earnings results over 10% higher than our Street competitors and also some multiple expansion on this out of favor stock.

LO – Lorillard reported Q1 2014 results on Thursday that were lukewarm, missing Street estimates on the top and bottom lines, however the stock closed up on the day.

Our long-term bullish outlook remains unchanged and built on 1) the strength and profitability of its advantaged menthol portfolio, 2) our belief in the limited menthol regulatory risk over the longer term, and 3) upside growth in its blu e-cigarette business that commands leading share in the U.S.

CEO Murray Kessler recognized that the convergence of numerous headwinds impacted the quarter’s results: for cigarettes lower wholesale inventory levels, severe weather affecting core markets, a tax increase in Puerto Rico and holiday timing (Easter), as well as in e-cigs lower prices of its rechargables kits and pipeline inventory build versus the year ago-quarter.

All that said, LO had impressive price/mix of +5.8% to offset total cigarette volume decline of -2.9% (outperforming the total industry at -4.0%). Total LO retail market share in the quarter rose 30bps to 15.2%, its highest level ever and its first quarter above 15%, and Newport’s share grew 40bps to 13% while LO’s share of the menthol market was flat Y/Y at 40.7%, but improved 80bps sequentially.

While its e-cig blu contributed a $0.02 loss in the quarter and sales fell for a second straight quarter, the company announced a $10-20MM spend over next 6 to 9 months to rebrand its ownership in SKYCIG in the U.K. as blu and continue to support incremental brand building for blu in the U.S. The playing field in the U.K. is decidedly fragmented, yet the second largest e-cig market behind the U.S. We like LO’s strategy to invest early in its e-cig business to become category leaders.

OC – Owens Corning missed consensus estimates on both top and bottom line mostly stemming from poor weather. So is weather a valid excuse? We think so. It is quite hard to install insulation or roofing products in snow and ice. As a result, the segment data can be quite noisy shown in the graph below. More importantly, we saw margin improvement in its two core segments: Insulation and Composites. Margins held steady and/or improved in a challenging environment bodes well for OC. 2Q should see higher volume across OC’s segments as construction activity picks up heading into the summer. FY 2014 guidance remains unchanged, but is now expected on the lower end. It is hard to put too much weight on 1Q results, but OC will need to deliver in 2Q.

RH – Restoration Hardware had a notable personnel event this week, with the appointment of Dr. Leonard Schlesinger to its Board of Directors. Ordinarily we don’t comment on developments on a company’s Board. But this one is notable – especially given the concern that so many people have about the company’s executive ranks since the departure of its former Co-CEO last year. The new Board member is about as well-decorated as a company the size of RH could hope for. He was Vice Chairman/COO of Limited Brands from 1999 through 2007 and is currently a Professor at Harvard Business School. He has served in numerous other roles in both C-Suites and Academia. We like how well-rounded Schlessinger is – especially given some of the questionable Board appointments we see these days. This is very complimentary to the addition of Doug Diemoz last month as Chief Development Officer.

We don’t expect this to wipe away the concerns of all the people that think that Gary Friedman is a risk being the sole person at the top. But we think that will be addressed by one thing alone – the focus of the management team, and the company’s performance over the next year. Both of those should absolutely be there. In the end, by this time next year, we think that ‘management risk’ will be off the table for people considering RH as an investment (and a part of the short case will be taken out to pasture).

ZQK – On Friday VF Corp announced solid 1Q earnings, which we think has several implications for Quiksilver. First off, VFC is the biggest apparel company that most people never heard of. It owns 30 lifestyle brands including Wrangler, Lee, Timberland, Vans and The North Face. While it operates primarily through wholesale channels, it has 1,100 of its own retail stores across concepts throughout the globe.

So what applies to ZQK? 1) Every division at VFC missed expectations except its Outdoor/Action Sports coalition. Furthermore, the strongest brand in the quarter – and now officially the biggest brand in the portfolio – is Vans. That’s a good sign for the action sports space, and most specifically, ZQK’s DC Shoes division. 2) VFC particularly noted that it’s Southern European business is picking up – where ZQK is particularly strong. 3) Most importantly, this beat shows how important Action Sports is to VFC. There is no question in our minds that VFC will continue to be acquisitive in this space, and as it’s $11bn revenue base continues to grow there are not too many brands it can buy that will make a dent in the financial model. One of the few is ZQK. 4) Add that to the comment from Kering (owner of Gucci, Puma, Volcom, Tretorn, Cobra Golf, YSL, Alexander McQueen, etc…) that it is looking to acquire more sports brands, and that puts ZQK right in the sweet spot. It does not hurt that ZQK CEO Andy Mooney gets a $25mm payday if the stock breaks through $9.28.

We continue to believe that the brand will gain traction organically, until it is ultimately taken out in 1-2 years – likely at a low double-digit price. We think it’s a 2-year double.

* * * * * * *

Click on each title below to unlock the institutional content.

Macro analyst Christian Drake says at the midpoint in Q1 2014 earnings, the trends are looking very much the same as those that prevailed in Q4 2013.

We Remain Bullish on Chipotle (CMG)

Managing Director Howard Penney remains bullish on CMG, as it continues to take share in an ultra-competitive environment. Recent comp & traffic numbers are unheard of.

Debunking Dillard’s (DDS) at $155—We Like the Short Side

Retail Sector Head Brian McGough says DDS at $155 seems ridiculous. The asset play is maybe $50 on a great day. If people value DDS like a retailer again, the stock’s in trouble.