CAKE remains on the Hedgeye Best Ideas list as a SHORT.

CAKE reported mixed results AMC, beating top line estimates by 61 bps and missing bottom line estimates by 1192 bps. Labor and, to a lesser extent, food costs pressured the P&L in the quarter as restaurant level margins decreased approximately 70 bps YoY.

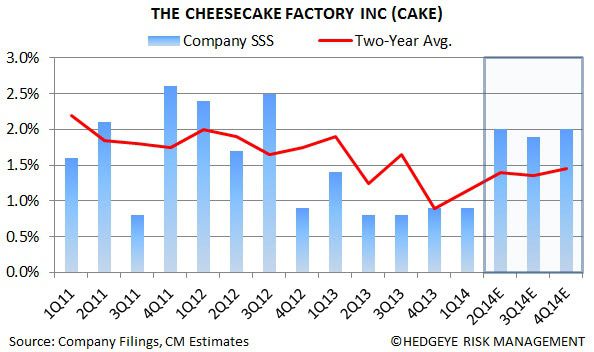

System same-store sales increased 0.9% despite management citing a negative 2% impact from severe winter storms and a holiday shift. This includes a 1.2% increase at The Cheesecake Factory and 2.9% decline at Grand Lux Café. Chairman and CEO David Overton highlighted notable strength in three of CAKE’s largest markets: California, Florida and Texas. CAKE’s same-store sales continue to outperform the broader casual dining industry. However, we estimate that traffic was down 1.0% in the quarter, making it the sixth consecutive quarter of negative traffic.

Management guided down FY14 EPS to $2.24-2.33 from prior $2.29-2.41. They also reiterated their full-year commodity inflation outlook of 3-4% led by salmon and shrimp. Although meat and dairy prices are higher than anticipated, they are expected to be offset by the easing of other commodities. Management did not disclose what these other commodities are.

To be clear, this is by no means a structural short. CAKE has been and continues to be a very strong operating company. However, we continue to believe that the company will be negatively impacted by looming margin pressure in 2014.

With that being said, our 4Q and 1Q catalysts have passed and although earnings estimates have been revised down noticeably, the stock has not followed suit. We expect price to more properly reflect fundamentals in the near-term. On the positive side impressive same-store sales momentum, strong brand relevance and shareholder friendly practices continue to support the stock.

What we liked:

- 1.2% same-store sales at The Cheesecake Factory, despite operating in a difficult environment.

- Same-store sales booming in its three largest domestic markets (up approximately 3% in 1Q).

- 70 bps benefit to SSS in 2Q due to timing shift.

- Food cost inflation outlook for the full-year remains unchanged at 3-4%.

- Shareholder friendly capital allocation. Plan to use all FCF in FY14 to fund dividends and share buybacks.

- International stores are strong performers and the growth potential is promising.

What we didn’t like:

- FY14 EPS guided down to $2.24-2.33 from prior $2.29-2.41.

- Labor line was disruptive in 1Q due to higher than anticipated group medical costs and productivity inefficiencies as a result of volatile weather/traffic.

- Traffic was down 1.0%, making it the sixth consecutive quarter of negative traffic.

- Commodity inflation remains a risk, although management appears to have this under control.

Howard Penney

Managing Director

Fred Masotta

Analyst