Continuing the theme from Q1, restaurant companies are beating Q2 EPS expectations by cutting costs. Unlike Q1, a significant earnings beat is no longer driving stocks appreciably higher. The cost cutting theme is becoming the consensus and not an investable theme that moves stocks.

Here is the drill from a typical company.

The good news:

“We’ve also identified other cost savings opportunities”

“The lower capital spending will go towards boosting our cash balance, further strengthening our balance sheet and increasing our future flexibility. And we will have even more time and resources to focus on operations and execution at our existing base of restaurants.”

Unfortunately:

“Despite a continued low level of visibility for the rest of the year due to both last year’s volatility and the ongoing economic uncertainty it’s very difficult to know where same-store sales will come in”

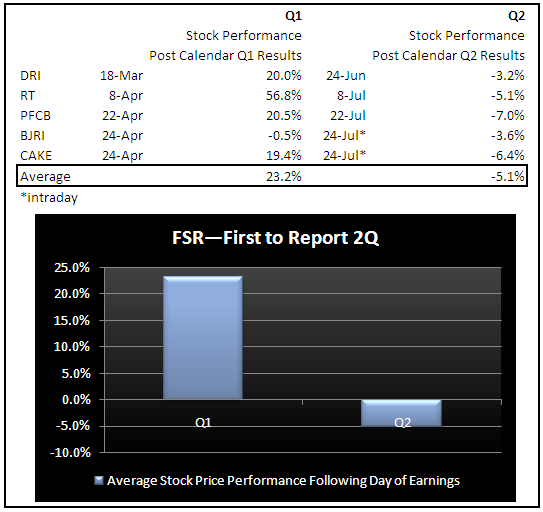

So far this earnings season, the stocks are not reacting to the better than expected earnings news. Stocks performed well post calendar Q1 numbers because for most FSR companies it was the first quarter of operating margin growth in at least two years. In Q1, restaurant operators proved they could cut costs to offset sales weakness and boost margins. In Q2, investors seem to be expecting these cost savings and even when a company increases its cost saving projections, like CAKE did yesterday, it is not enough to get the stock moving higher.

The bulk of the fat has been cut from these companies’ operating models so the obvious question is where do we go from here. It will be impossible for these companies to continue to grow margins once they start to lap these savings initiatives if sales don’t pick up. They can’t cut costs forever without hurting the customer experience and eroding their brands. And, as I already pointed out, most companies are saying they have limited visibility about when sales might turn positive.

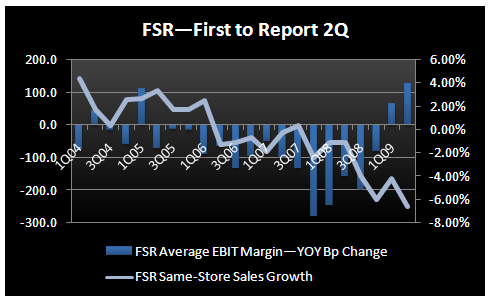

This thought can best be shown by the chart below, which looks at FSR same-store sales growth trends, as reported by Malcolm Knapp, relative to the average YOY bp change in EBIT margin for DRI, RT, CAKE, PFCB and BJRI (FSR companies that have reported calendar 2Q earnings so far).

Clearly this trend is not sustainable – these companies cannot continue to grow margins with negative same-store sales growth. CAKE’s CFO Doug Benn highlighted this point in response to a question about if and when the company would recapture the margin level of yesteryear:

“Internally, the way that we are looking at it, we’re taking it one step at a time. If you go back to 2007 margins, operating margins they were around 8.5%, which is somewhere in the neighborhood of 250 to 300 basis points better than where we expect to end this year. And the scenario to get back there, some of it is going to be this cost-cutting and the cost initiatives and we’ve made some great progress there but the real avenue to get back is we have to have a plus sign in front of comparable store sales. And until we do that, we’re not going to be able to get all the way back.”

We all know that comparisons get very easy in 2H, particularly in Q4. What if easy comparisons are not that easy? Minimum wage is now higher for the balance of 2009 and the benefits of lower commodity costs will diminish over the next six months.

I don’t want to paint a bearish picture because nearly all the companies I follow are financially strong cash generators. And, with little to no development plans in the near-term, their cash positions are only building. What I’m struggling with is deciphering the catalyst (positive or negative) that will get these stocks moving in either direction.