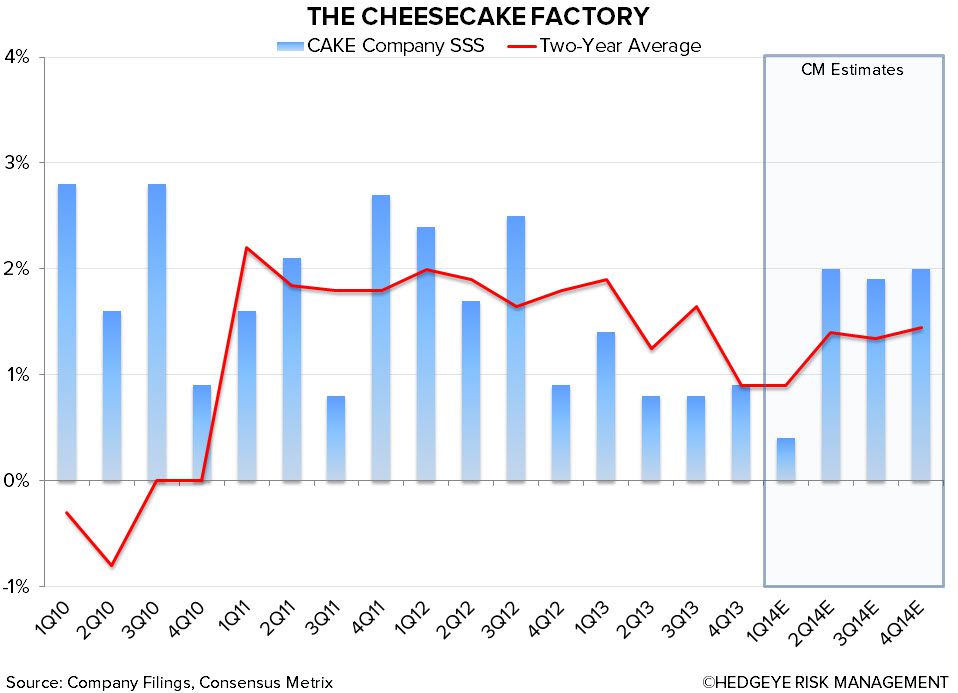

The Cheesecake Factory Incorporated (CAKE)

Details: We’ve been bullish on CAKE for the better part of the past two years, but we believe margin pressure is building and the bar is set too high for FY14. To be clear, this is not a structural short. CAKE is a strong company with a good management team, so we will be disciplined with our call.

Traffic: Traffic has declined for the past five quarters at CAKE and the macro backdrop hasn’t been encouraging. We believe the casual dining industry is in secular decline as it continues to lose market share to select fast casual and quick service players. Mall traffic has also been weak as consumers are increasingly shopping online. CAKE has significant exposure to malls, but management has denied a link between mall and restaurant traffic. We contend that this dynamic presents a headwind for CAKE, not matter how minimal it presently is.

Margin Pressure: CAKE needs to drive positive traffic soon. As a result, we expect them to reinvest in labor and other expenses in order to attract more visits and increase frequency. Minimum wage increases and the looming ACA are also expected to pressure margins. Our biggest concern, however, is on the cost of sales line as food inflation has accelerated meaningfully in 2014. Management guided to 3-4% food inflation in FY14, due in large part to rising shrimp and salmon prices which are up +60.8% and +10.4% YoY, respectively. We believe dairy prices are causing incremental pressure on the COGS line, as the surge in milk and cheese prices has been more resilient than most anticipated. These two commodities are up +36.6% and +17.5% YoY, respectively. Management previously noted that they only have 40% of dairy needs locked in for FY14. The street only estimates cost of sales as a % of revenue to increase 8 bps for the full year. We believe this is very unlikely.

Guidance: Management guided down 1Q14 numbers on the 4Q13 earnings call, but maintained full-year guidance. As such, the stock has been quite resilient. We believe the bar is too high and expect management to guide down FY14 numbers on the 1Q14 earnings call. FY14 EPS estimates have come down slightly, from $2.38 to $2.36, only to reflect a disappointing first quarter. Full-year estimates look achievable if commodities ease in the back half of 2014, but we’ve seen no signs of this happening. FY15 estimates for 16% EPS growth on 8% sales growth continue to look aggressive.

Valuation: CAKE trades at 20.07x P/E and 9.08x EV/EBITDA on a NTM basis.

Bloomin’ Brands

Details: It’s difficult to find a compelling company in the casual dining industry that has a large, complex portfolio of brands. We believe the casual dining industry is in secular decline. According to Malcolm Knapp, 2013 marked the eighth consecutive year of same-restaurant traffic declines. In the new age of casual dining, the brands that focus on doing one thing right are the most successful. Companies with large, diverse portfolios are at greater risk of missing the numbers than smaller, more nimble players.

Sales Trends: Two-year same-store sales trends across all four of BLMN’s main concepts are deteriorating. As a result, management has been rolling out weekday lunch at Outback and Carrabba’s. We contend this is to mask a decline in the core dinner business. As a result of the lunch rollout, we expect same-store sales trends to outperform the Knapp Track Index. We believe BLMN will run into trouble at some point in 2H14 and beyond as they begin to lap the lunch rollout. Bonefish Grill, the portfolio's “growth vehicle,” has had same-store sales decline on a two-year basis since 1Q12.

Margins: BLMN has some of the worst operating margins in the restaurant industry. Despite the efficiencies management has claimed to achieve, operating margins as a % of sales have mostly remained flat since 1Q11. We believe this is a primary reason why BLMN opted to acquire its Brazilian JV late last year. We expect food costs in FY14 to pressure margins more than the street expects and believe the street is too aggressive in its labor cost leverage assumption. We believe margins will be pressured for the majority of 2014. FY14 consensus estimates have been cut in half to 10% EPS growth on 8% sales growth. The real disconnect comes in FY15, with the street expecting 20% EPS growth on 7% sales growth. These estimates are far too aggressive – in fact, we don’t think BLMN will ever grow EPS by 20% in a given year.

Valuation: BLMN trades at 18.59x P/E and 8.61x EV/EBITDA on a NTM basis.

Panera Bread Company (PNRA)

Details: PNRA has secular and well-publicized operational issues working against it. This has led to the vision for Panera 2.0, in which management aims to thrive in a digital future. We are on board with management’s plans, we just happen to think they will take longer to materialize than consensus.

Increased Competition: PNRA has secular forces working against it that didn’t exist a few years ago. There are more fast casual players than ever before, QSR chains have upgraded looks and menus, and casual dining companies have resorted to discounting. These chains market their products heavily and offer them at cheaper price points than Panera’s core offerings. As a result, PNRA has little pricing power and a value equation that is out of sync.

Operational Issues: Capacity and throughout issues plagued PNRA in 2013. As a result, 2014 and 2015 will be heavy investment years. PNRA must invest to improve its café operating experience by reconfiguring product lines, streamlining menu offerings, offering lower priced items, delivering product consistency and improving speed of service. We believe Panera 2.0 will address these issues, but it will take significant investment and time to materialize. PNRA also plans to ramp up its advertising spend in 2H14 with a national cable TV launch. Will the system be ready to handle incremental traffic as a result?

Concerns: We are concerned by a lack of visibility around earnings and the reality is PNRA 2.0 won’t be fully rolled out until the end of FY15. Management would not commit to higher margins post-rollout, because they don’t know if this is possible. They also spoke of conscious cannibalization during the Investor Day in late March. To us, this signals market maturity and indicates that the majority of future growth will be at lower returns as cannibalization and the significant investment (labor and training, IT fees, etc.) that comes with Panera 2.0 take hold. We expect FY14 and FY15 to be margin compressing years. FY14 could get a bump from the national advertising rollout, but FY15 estimates of 15% EPS growth on 10% sales growth look aggressive.

Valuation: PNRA is trading at 24.6x P/E and 10.76x EV/EBITDA on a NTM basis.

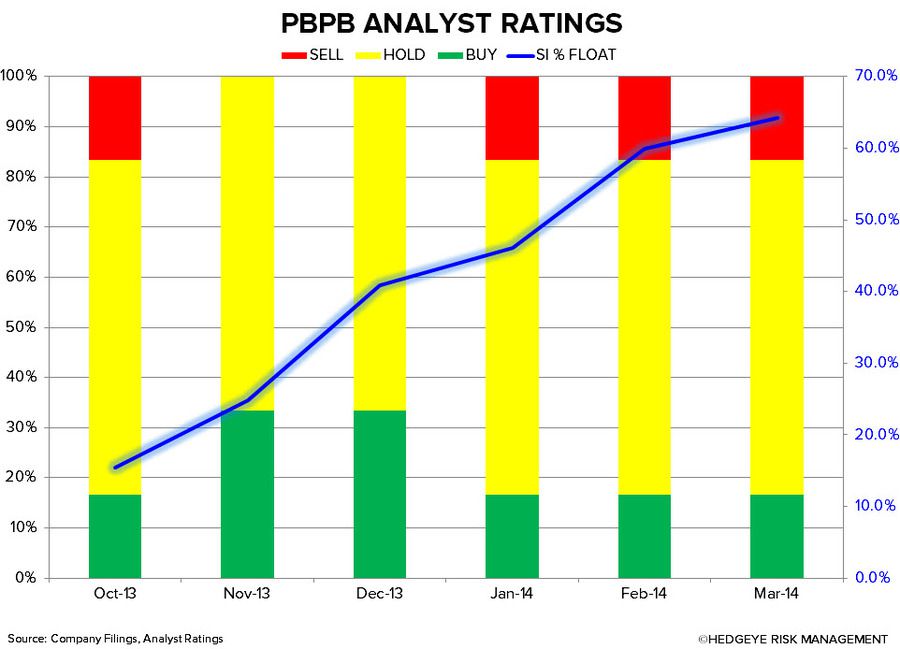

Potbelly Corporation (PBPB)

Details: We’ve been bearish on PBPB since it closed its first day as a public company at $30.77 a share. We believe Potbelly is a solid company, with a respected management team, but it’s been difficult to justify its valuation considering it competes in the most competitive segment in the restaurant industry. At its core, PBPB is a single daypart, low margin, low return, local sandwich chain with declining traffic and little competitive advantage over its most basic peers.

Fundamentals: Same-store sales and traffic trends continue to be discouraging for a company flagged as a growth chain. Weather is partly to blame for recent weakness, but the truth it will continue to be a headwind until management diversifies its unit base. PBPB’s operating model requires sales leverage in order to drive further upside. We believe 1Q14 will mark the fifth consecutive quarter of traffic declines and another quarter of lower YoY average unit volumes.

Takeaway: We believe PBPB can be a feasible, financially robust company over the long haul, but we continue to see downside in the stock. Current fundamentals continue to suggest it is overvalued and the FY14 outlook is under pressure. We’d be tempted to like PBPB at a much lower price, but we need to see the company begin to generate some sustainable same-store sales momentum.

Valuation: PBPB is trading at 50.18x P/E and 20.92x EV/EBITDA on a NTM basis.

Howard Penney

Managing Director

Fred Masotta

Analyst