We recently added BNNY to the Hedgeye Best Ideas list as a SHORT.

BNNY’s core business is the marketing and distribution of natural and organic food products under the Annie’s brand name. BNNY has the number one natural and organic market position in four product lines: macaroni and cheese, snack crackers, fruit snacks and graham crackers. The natural and organic segment of the food industry is the fastest and most dynamic part of the industry – and BNNY is a key player.

BNNY operates three main business segments: meals; snacks; and dressings, condiments and other. While the company has shown admirable topline growth, the growing pains of managing this growth as a publicly traded company are beginning to take their toll on the margin composition of the company.

The company has faced numerous issues since coming public in April 2012, including executive departures, product recalls and balance sheet issues (excess inventory growth, inventory write-downs, accounts receivable). In addition, a viable competitor, WhiteWave (WWAV) has emerged and is going after both BNNY’s core macaroni & cheese and cracker businesses. On top of all this, significant commodity inflation in organic wheat has recently emerged as another notable headwind facing the business.

The company has not provided guidance for FY15, but will do so when they report earnings on June 10th. We think the current EPS estimate of $1.13, or 22% growth, is very aggressive. Although estimates were revised down significantly following 3QF14 earnings, we believe they have not come down nearly enough.

INVESTMENT POSITIVES

Great Brand in the Right Category – As advertised, the Annie’s brand authentically honors social responsibility and environmental sustainability by selling products with clean ingredients and giving mom a healthy alternative to mainstream packaged foods.

Strong Volume Growth – The company has reported significant volume growth in its grocery and mass distribution segments since coming public, driven by deeper penetration in the main aisle of the grocery store. Additional volume growth is being driven by innovation and expansion into new categories.

Broader Popularity – A big shift for Annie’s is the pivot to selling more products in the main aisle of the grocery store. Historically, natural and organic foods were primarily only available at independent organic retailers or natural and organic retail chains. Mainstream grocery stores and mass merchandisers have expanded their natural and organic food offerings to meet the increasing consumer demand for natural and organic products, which generally command a higher margin for the retailer.

New Products – FY14 marks a year of accelerated innovation for Annie’s, as the company launched two new products. On the 4QF13 earnings call, management announced a “highly incremental” platform extension to the mac & cheese business – the entry into the single serve microwaveable cup segment. This segment represents approximately 20% of the total mac & cheese category and is growing at twice the rate of the overall category in conventional distribution channels. On the 1QF14 earnings call, management said they’d secured over 15,000 points of distribution for microwaveable cups, adding that sales so far have been incremental to the base mac & cheese business.

During the same call, management also announced BNNY’s entry into the Family Size segment of the Frozen Entrée category with the launch of four items: Lasagna with Meat Sauce, Classic Mac & Cheese, Shells & White Cheddar with Chicken and Butternut Squash Mac & Cheese. This segment is nearly a $3.5 billion category that’s dominated by large, conventional brands and lacks an established, authentic natural organic offering.

INVESTMENT NEGATIVES

The Pivot to an Asset-Based Model – Since becoming a publicly traded company, BNNY has had a difficult time meeting earnings guidance. Clearly, managing a rapidly growing business is a challenge for management. In FY15, the company is taking on incremental operational risk by acquiring hard assets. Historically, the company utilized contract manufacturers or co-packers to manufacture the company’s entire product line. In FY13, BNNY’s four largest contract manufacturers accounted for 75% of the company’s sales.

Last week, the company announced the closing of its acquisition of the Safeway snack factory in Joplin, Missouri. We believe both the company and the street have inadequately accounted for this acquisition. In our opinion, it is prudent to assume the pivot to an asset-based model will present operational issues in FY15.

Our first concern is regarding the geographical location of the plant – Joplin, MO is a considerable distance from Berkley, CA. Second, and more importantly, BNNY is currently an asset-light business model. Given that the company uses all contract manufacturers to source its product, owning a manufacturing plant could present new, unexpected operational issues. Third, any inefficiencies stemming from the plant will be significantly dilutive to EPS in FY15. On the positive side, the plant already produces close to 100% of Annie’s product and the company has signed a three-year supply deal with Safeway to help ensure consistent demand.

Commodity Inflation – According to management, FY15 is going to be “a tale of two halves.” The inflation headwinds that pressured margins in FY14 will persist, particularly with regards to organic wheat and cheese prices. For the time being, commodity inflation is expected to moderate over the course of FY15, with overall pressure being more modest on a year-over-year basis.

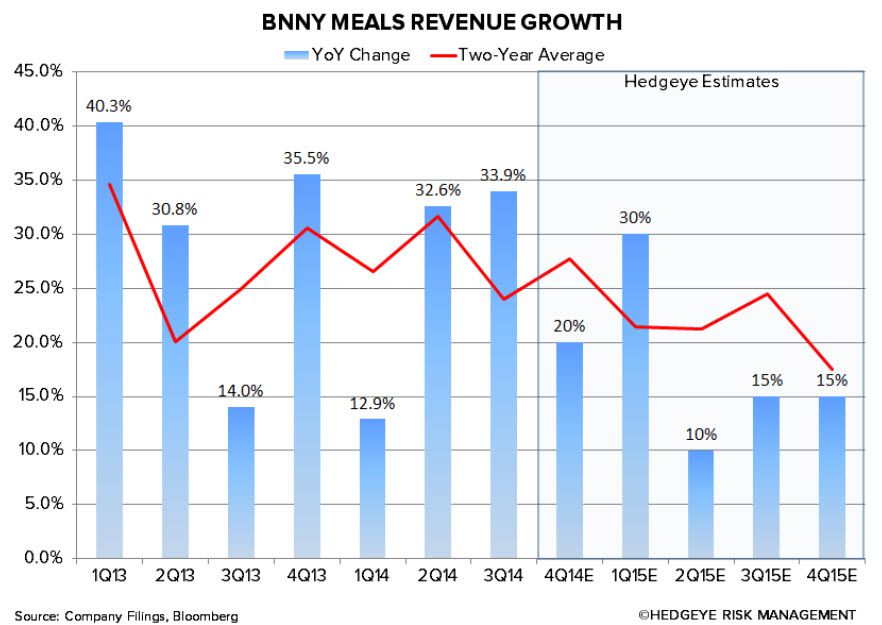

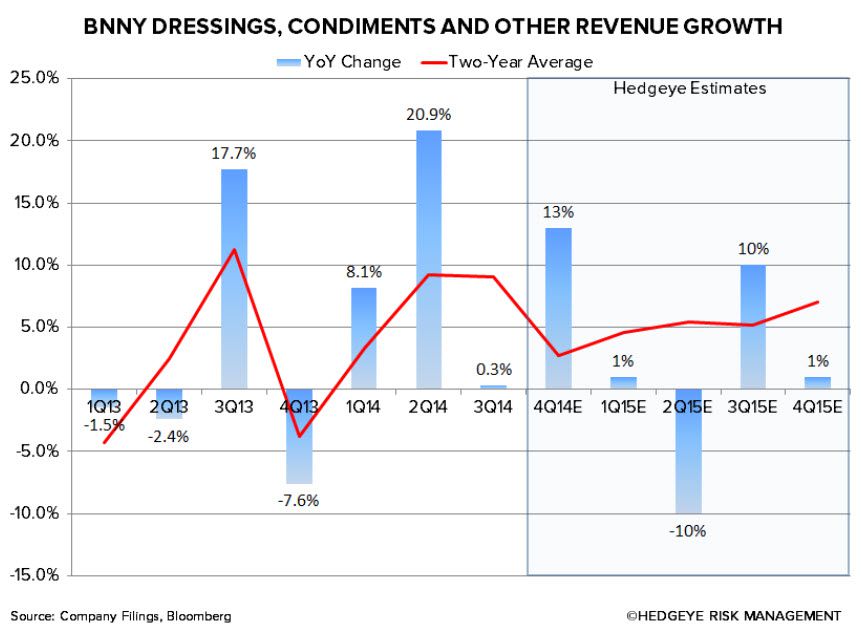

Decelerating Sales Trends – Two-year sales trends are set to slow in FY15, as the company rolls over the introduction of two new product launches in FY14.

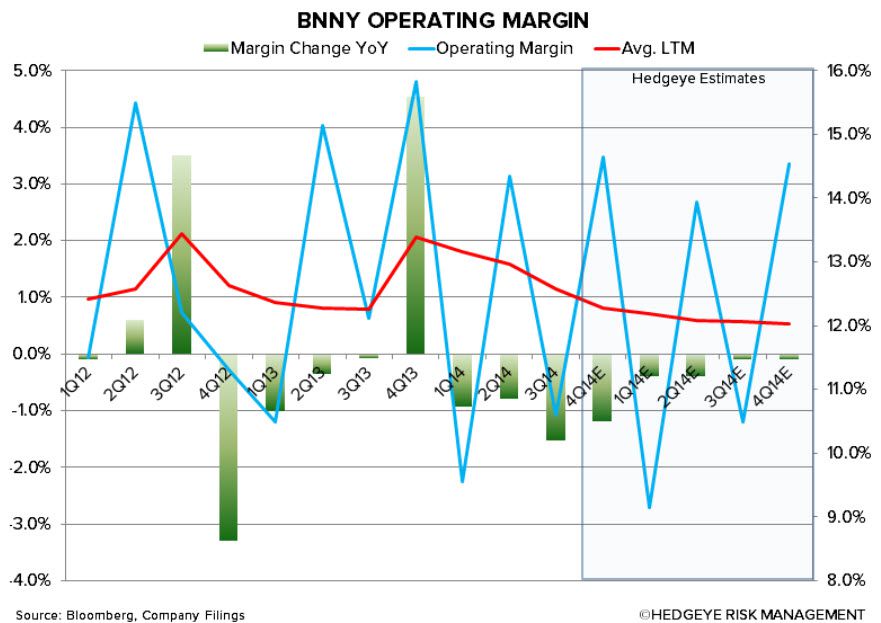

Margin Pressure – We expect increased complexity, new products and food inflation to all lead to a significant decline in gross margins. With 4QF14 yet to be reported, we estimate gross margins will be down 200 bps for the full fiscal year. While some of this can be labeled as “one time” in nature, it is likely that the company will be operating at a lower gross margin for a significant period of time. In FY14, the majority of gross margin pressure came from inflation, sales mix and inventory management. More recently, there has been material commodity inflation due in large part to a surge in organic wheat and cheese prices. We don’t expect this to ease until sometime in 2HF15.

While inflation pressures may lessen in the back half of FY15, channel issues and a sales mix shift due to new products will likely persist for the balance of the year and potentially longer. We also see “aged inventory” as a troubling sign and believe this signals weak internal controls.

Operating margins only declined 150 bps in 3QF14 due to aggressive expense management. For a growth company, this decline in SG&A is not a net positive and can be labeled as “one time” in nature as well. The company remains on a very aggressive growth curve and is transitioning its business to an asset-based model. We question how much wiggle room they have left on the SG&A line.

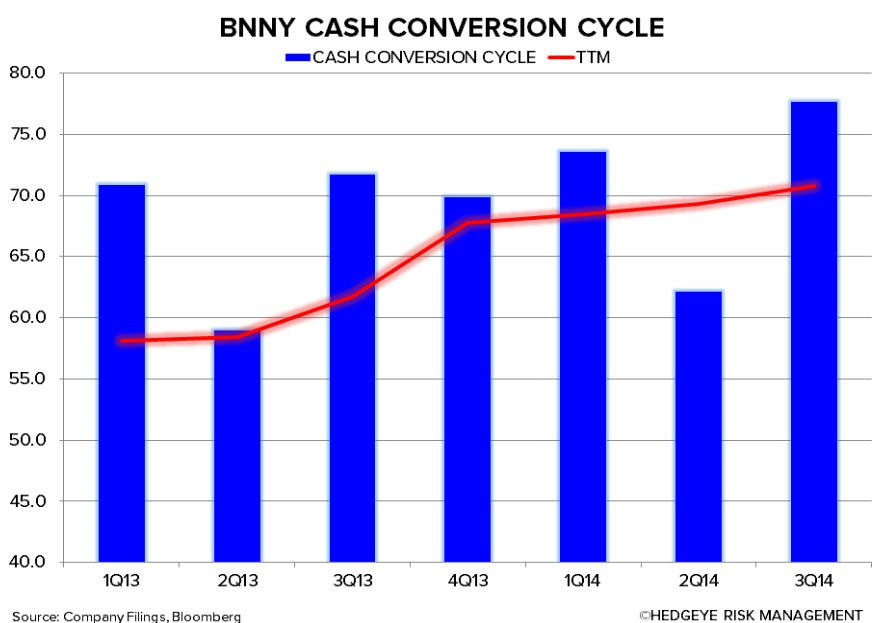

Balance Sheet Issues – For a company such as BNNY, which is seeing tremendous volume growth, we find it very odd that it needs to write down old inventory and has trouble converting sales into cash.

Employee Turnover – Former CFO Kelly Kennedy announced her resignation back in November 2013. Former EVP and Chief Supply Chain and People Officer Amanda Martinez tendered her resignation at the end of March 2014. We suspect Ms. Martinez may be taking the fall for the companies issues to-date in 2014. It’s an odd move, considering she was only promoted to the position a few months ago.

Increased Competition – WhiteWave, through its Horizon brand, has recently introduced a new mac & cheese business as well as a snacks & crackers business to compete directly with Annie's products. While this is not new news to the market, it continues to be an overhang on BNNY. Annie’s FY14 results thus far have not shown a significant slowdown in Mac & Cheese sales trends, but the pressure will not be going away any time soon.

SENTIMENT

Generally, the street is rather cautious on the name, with 80% of analysts rating the stock a hold and short interest comprising 23% of the float. However, with the street looking for 22% EPS growth in FY15, we believe this is a prudent call.

VALUATION

At 34x NTM EPS, the stock trades at a substantial premium to the group, which is trading closer to 22x. To its credit, BNNY is showing significantly stronger top line growth than its peers; however, we have legitimate concerns with the company’s ability to manage EPS.

We believe BNNY represents an attractive risk/reward setup for short sellers, offering material downside in the intermediate-term.

Howard Penney

Managing Director

Matt Hedrick

Associate

Fred Masotta

Analyst