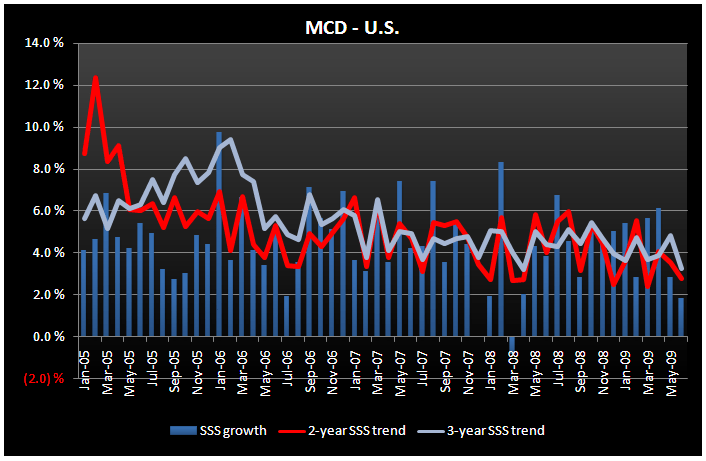

MCD’s June same-store sales slowed rather significantly on a sequential basis across the board. MCD stated that a calendar shift/trading day adjustment varied by area of the world, ranging from -2.0% to 0.2% in June 2009. Even adding back 2% to the reported numbers, 2-year average trends slowed in each geographic segment. The comparisons get substantially more difficult in July as the company is lapping a 6.7% same-store sales number in the U.S. and 8% on a consolidated basis. That being said, CEO Jim Skinner stated, “As we begin the third quarter, we expect to report July consolidated comparable sales similar to or better than June.”

U.S. comparable sales increased 1.8% in June following a 2.8% number in May. And, it looks like these weaker than expected trends are likely to continue in July.

As I said earlier this week, I continue to believe that McDonald’s current product strategy, including the roll out of its premium Angus burger and McCafe specialty coffee platform, is not focused on its core market – family and value-minded customers. As we are seeing with other QSR operators that are focused on more premium menu offerings, particularly CKR, now is not the right time to try to drive traffic with more expensive menu items. Rolling out a $4 sandwich and $3.50 cup of coffee into the teeth of a 10% unemployment rate could be a case of unfortunate timing.