“He is striking at everything. I am afraid of this man.”

-Thomas Gibbons, 1822

That’s the opening line to Part One (titled “Captain” – 1) in the latest brick I’ve cracked open, The First Tycoon – The Epic Life of Cornelius Vanderbilt, by T.J. Stiles. If you’re into hard core capitalism, this is where it’s at.

That’s not to say I’m not into Grubhub.com (GRUB) going public this morning (I couldn’t make that up if I tried)… or any company that doesn’t make any money for that matter. If the public is dumb enough to pay 15-20x revenues for companies with no earnings, there is a precedent for that. #1999

There’s also a longstanding history in America of hard core capitalists making hard core profits. Admittedly, I have a confirmation bias towards them. As William Gibbs McNeil said about Vanderbilt in 1840, “I’d sooner have him with us, than against us.” Amen to that.

Back to the Global Macro Grind…

As the European Central Bank (ECB) reduces the size of its balance sheet, Yellen’s Federal Reserve continues to ramp up the size of hers. At $4.2 TRILLION, I was perusing the Fed’s balance sheet last night. It was up another +$9.5B wk-over-wk, and +$1 TRILLION year-over-year. Socialism, baby!

Is that a bad word?

Or should we use statism? What else would you call an un-elected agency (the Federal Reserve), whose mandate is to get tighter as inflation accelerates and the economy expands, getting looser for the sake of the 1%-10% of the population that benefits from asset price inflation?

Economic expansion?

Yes. Newsflash:

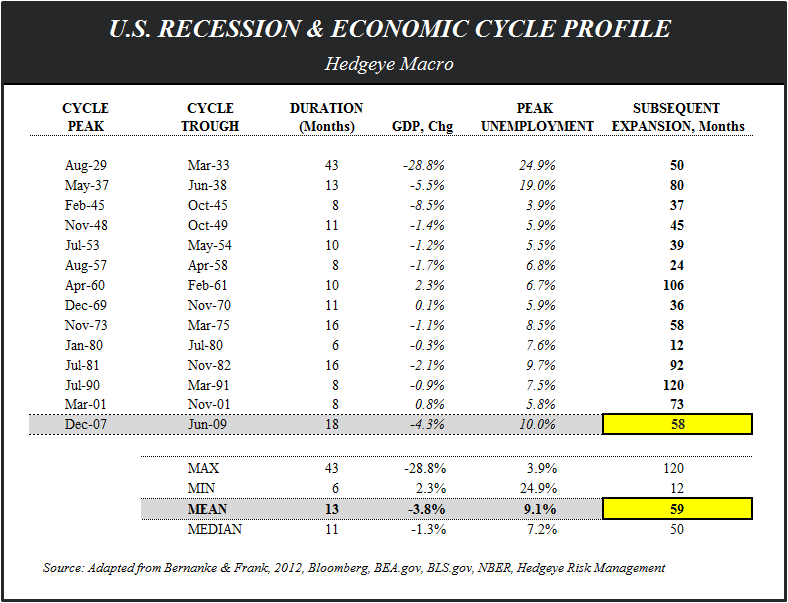

- The US economic expansion is now going into its 59th month!

- Pardon? Yes. Take out all the spew politicians have been whining about since missing the buying opp of a lifetime in 2009.

- And focus on what actually happened. In gravity speak, this is called a cycle (see #history table in today’s Chart of The Day)

Oh, and what you’ll note in the historical data is that the average US economic expansion following a recession is also … drum-roll… 59 months!

In other words, during this epic expansion, the Fed:

- Didn’t see any inflation, at the all-time-highs in US energy, food, education, rent, etc. inflation – so it didn’t see a need to tighten

- Won’t ever see inflation, until we have another inflation crisis

- And is now tapering (late) into what will likely be a US consumption growth slowdown

Yep, that last part is the least consensus of everything else I wrote, primarily because my conclusion is embedded in a forecast that isn’t consensus – i.e. that US #InflationAccelerating is finally slowing US consumption growth.

Hard core Keynesianism, this view is not. And what do you do if you share it? Do more of what you’ve been doing for 3 months:

- Buy Inflation (Short US Dollars, and Buy Commodities and/or anything with pricing power)

- Buy Bonds (because the Fed has 0% credibility and/or intention to fight inflation)

- Buy Foreign Currencies who has monetary policies that are building credibility

That’s why I feel pretty good about selling US Buy-The-Damn-Bubble #BTDB Growth Equities (everything we liked last year), booking those gains and plowing them back into the former Bernanke Bubbles (Food, Gold, Utilities, REITS, Bonds, Emerging Markets, etc.) that blew up in 2013.

The inflation topic drives people who take the Fed’s word for it (that there is no inflation) squirrel. But those are mostly people who are educated with a serious level of Western Academic Groupthink and don’t think for themselves. If you ask objective people, they know the government is lying to them.

We did a poll yesterday (powered by Polstir, here) that asked a very basic question: Do you trust the government’s inflation numbers?

87.5% responded no.

Yes Mr. and Mrs. Big-Government-Made-Up-Data, Hedgeye is 6 years older (with much wider distribution) than when we called you out on the last inflation-slows-growth cycle reality (our US consumer recession call in early 2008). We’ll be striking at everything you say going forward. Be afraid of the common man.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.66-2.82%

SPX 1

USD 79.83-80.72

EUR/USD 1.36-1.38

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer