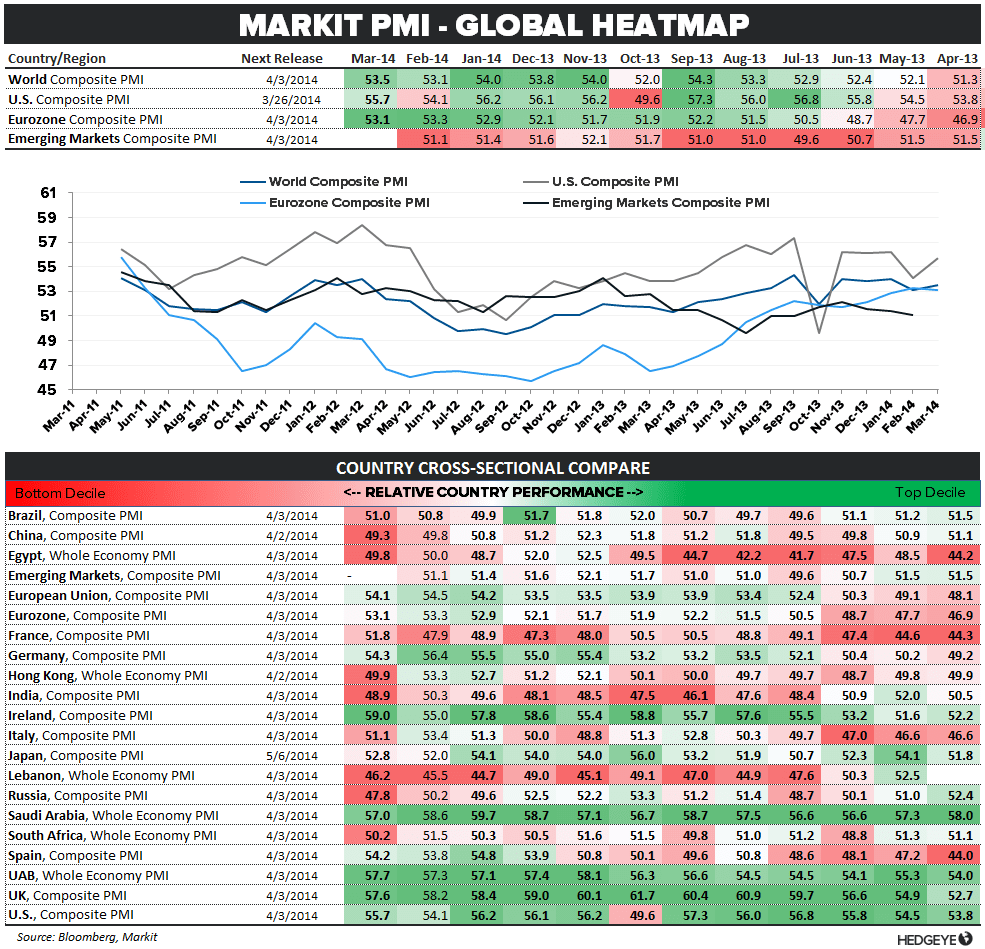

This morning’s initial claims data showed a second week of strong improvement while both the ISM Services reading and the final Markit Composite PMI rose +1.5 pts MoM in March.

As we’ve highlighted, sequential improvement in the reported March/April domestic macro data should be the base expectation – indeed, the surprise would be if we didn’t see a quasi-meaningful bounce off the weather distorted jan/feb figures.

So, unsurprisingly, the March ISM data showed sequential improvement but the magnitude of the bounce in Headline ISM services (or Monday's Mfg data) wasn’t overly compelling. The Business Employment sub-index gained +6.1pts in March, but failed to re-trace the -8.9 drop the month prior.

Similarly, New Orders advanced +2.1pts MoM but the Trend in New Orders across both the Services and Manufacturing survey’s remains one of discrete deceleration.

Further, the Business Activity and Backlog indices actually declined MoM while prices paid jumped +4.6 to 58.3.

Of course, from a policy perspective – where the path of least resistance is to continue to step down the pace of QE - even an optical recovery in the reported economic data should support the prevailing policy stance.

From a positioning perspective, while we’ve remained constrained in our intermediate-term growth outlook, tactically, we have been positioned net long in real-time alerts since the 1842 oversold signal in the SPX (see Oversold, Again: SP500 from march 19th).

To really pivot on our intermediate term view, we’d like to see the fundamental data recapture the slope of growth we saw in June-Sept/Oct of last year alongside a breakout in the dollar (Trend resistance = 81.19) and 10Y yields (2.81%) and move towards lower highs/lower lows in the VIX.

Until the collective fundamental and price signals confirm, the game plan of the last two months remains the same - we’ll simply continue to manage exposure within the risk of the immediate-term range.

Below is the detailed breakdown of this morning's claims data from the Hedgeye Financials team led by Joshua Steiner. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

- Hedgeye Macro

-------------------------------------------------------------------------------------------------------

INITIAL CLAIMS: Labor Market Tailwinds

Today's initial jobless claims data is positive and marks a continuation of the positive inflection in labor market data seen last week, bringing the new trend to two weeks. As a reminder, we focus on the year-over-year rate of change in the rolling, non-seasonally adjusted data. This week, claims were lower by 8.0% y/y, which is better vs the prior week's 7.1% improvement y/y. More importantly, the trend had been deteriorating in the YTD period until the inflection two weeks ago. We've now seen positive data for two weeks in a row, which matters because we it may shed some light on the ongoing debate about what role weather may or may not be playing in the economic data.

As we said last week:

One of the arguments put forward in support of the generally weak 1QTD data has been weather. If weather is playing a role in suppressing the strength of the data then one would expect that as we move from the winter to the spring months we could reasonably expect to see improvement in the data. The next few weeks of data should be important in this regard, as they may serve to answer this fundamental question.

The Data

Prior to revision, initial jobless claims rose 15k to 326k from 311k WoW, as the prior week's number was revised down by -1k to 310k.

The headline (unrevised) number shows claims were higher by 16k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 0.5k WoW to 318k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -8.0% lower YoY, which is a sequential improvement versus the previous week's YoY change of -7.1%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT