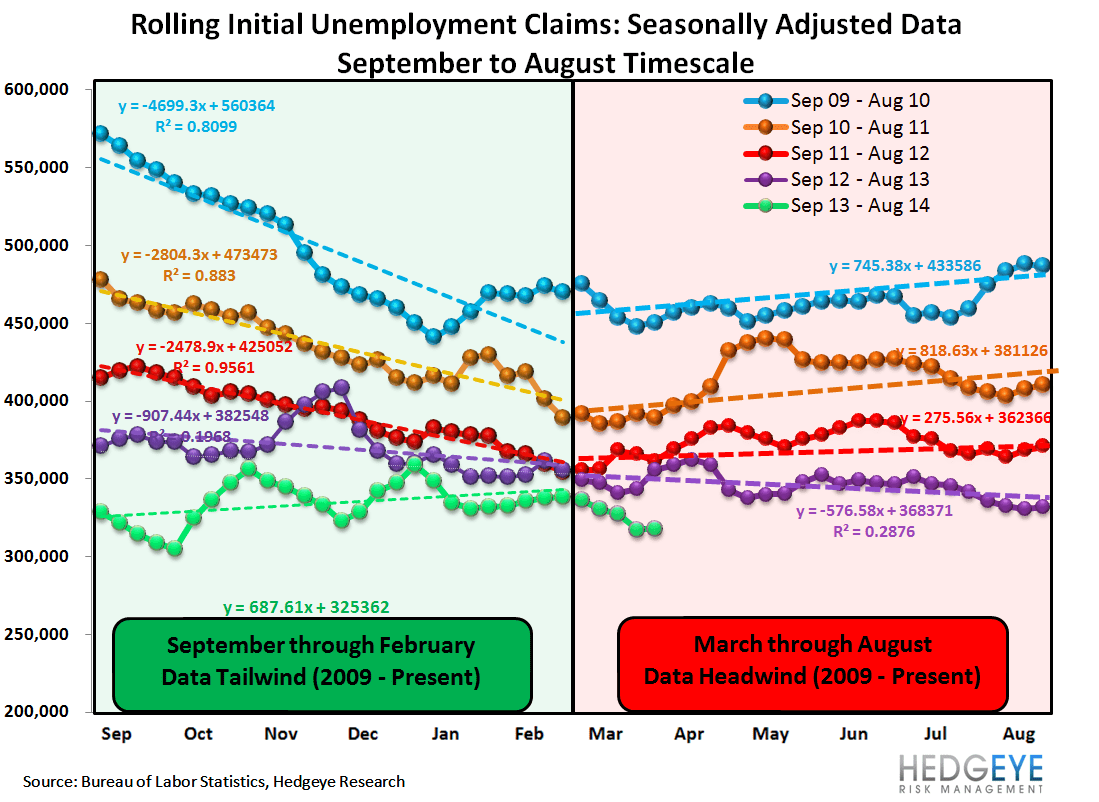

Labor Market Tailwinds

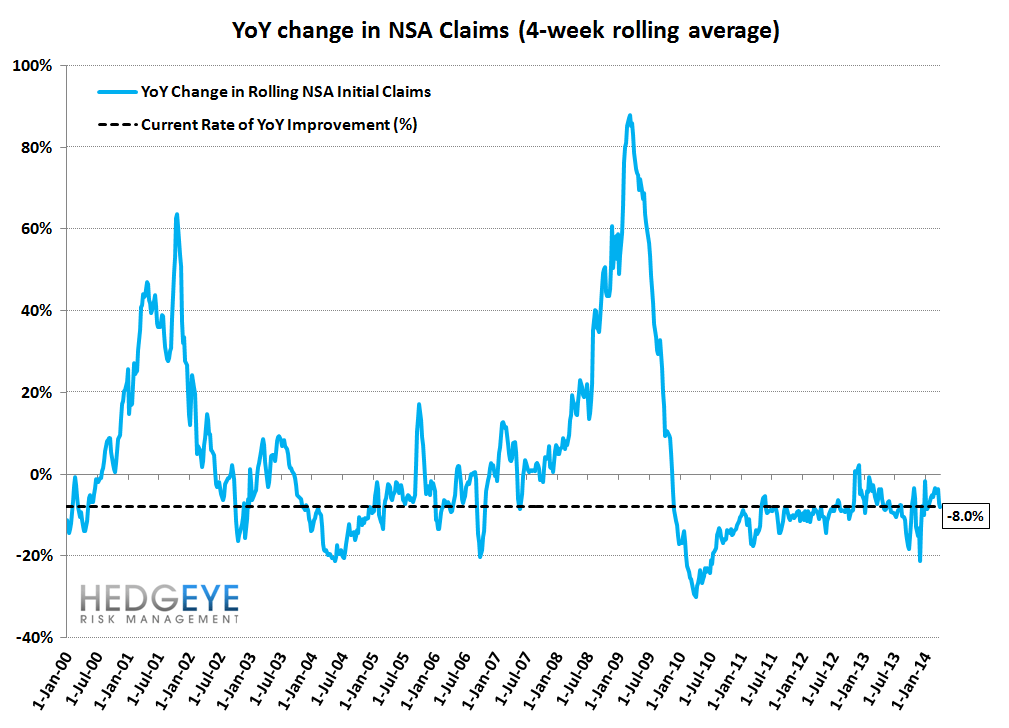

Today's initial jobless claims data is positive and marks a continuation of the positive inflection in labor market data seen last week, bringing the new trend to two weeks. As a reminder, we focus on the year-over-year rate of change in the rolling, non-seasonally adjusted data. This week, claims were lower by 8.0% y/y, which is better vs the prior week's 7.1% improvement y/y. More importantly, the trend had been deteriorating in the YTD period until the inflection two weeks ago. We've now seen positive data for two weeks in a row, which matters because we it may shed some light on the ongoing debate about what role weather may or may not be playing in the economic data.

As we said last week:

One of the arguments put forward in support of the generally weak 1QTD data has been weather. If weather is playing a role in suppressing the strength of the data then one would expect that as we move from the winter to the spring months we could reasonably expect to see improvement in the data. The next few weeks of data should be important in this regard, as they may serve to answer this fundamental question.

As a reminder, one of our favorite intermediate-term trade ideas on the long side remains Capital One (COF). We initiated that call in late January on the basis that seemingly every year Cap One misses 4Q and crushes 1Q. We argued for buying it post the 4Q wash-out, holding it through 1Q14 results and exiting ahead of 2Q results. The claims data this morning adds further support to that call. Almost all new loss content comes from newly unemployed people with the balance coming from divorce and illness (major medical expenses). Unsecured lenders like Capital One are hugely correlated with initial claims data, and claims tend to lead the fundamentals by ~13 weeks giving some visibility into what's coming down the pike.

The Data

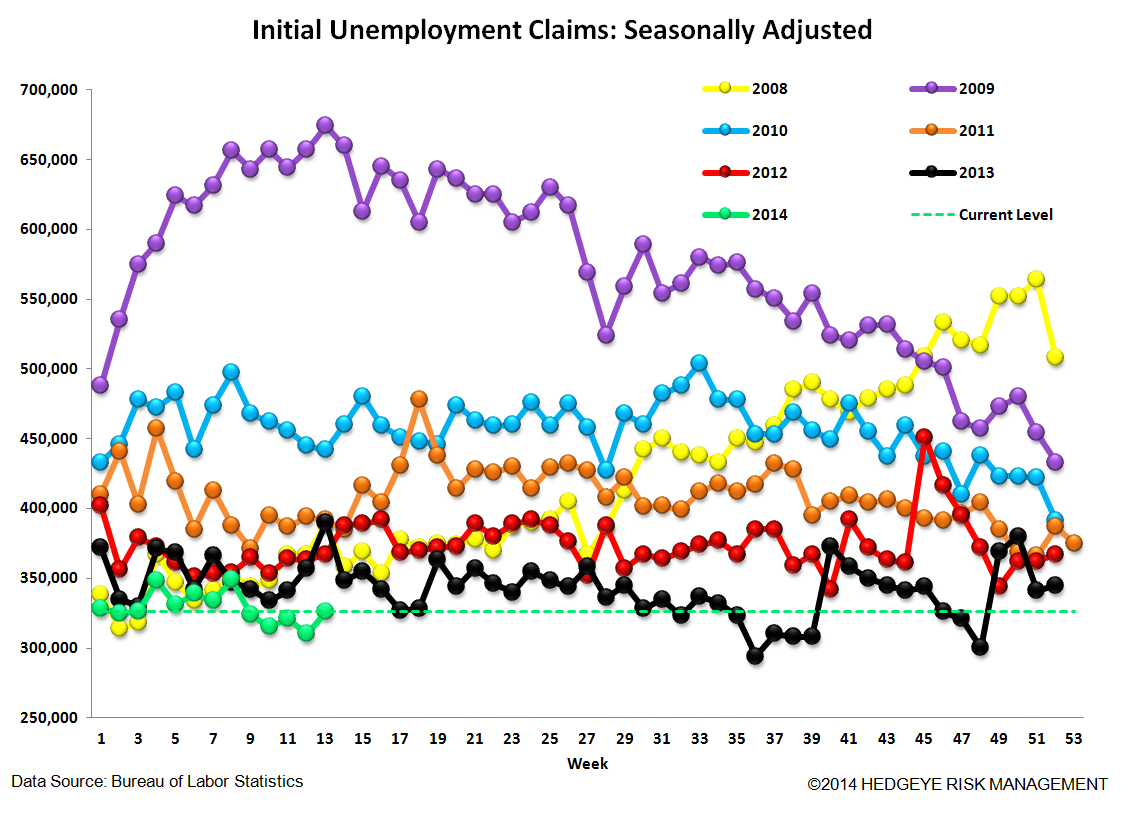

Prior to revision, initial jobless claims rose 15k to 326k from 311k WoW, as the prior week's number was revised down by -1k to 310k.

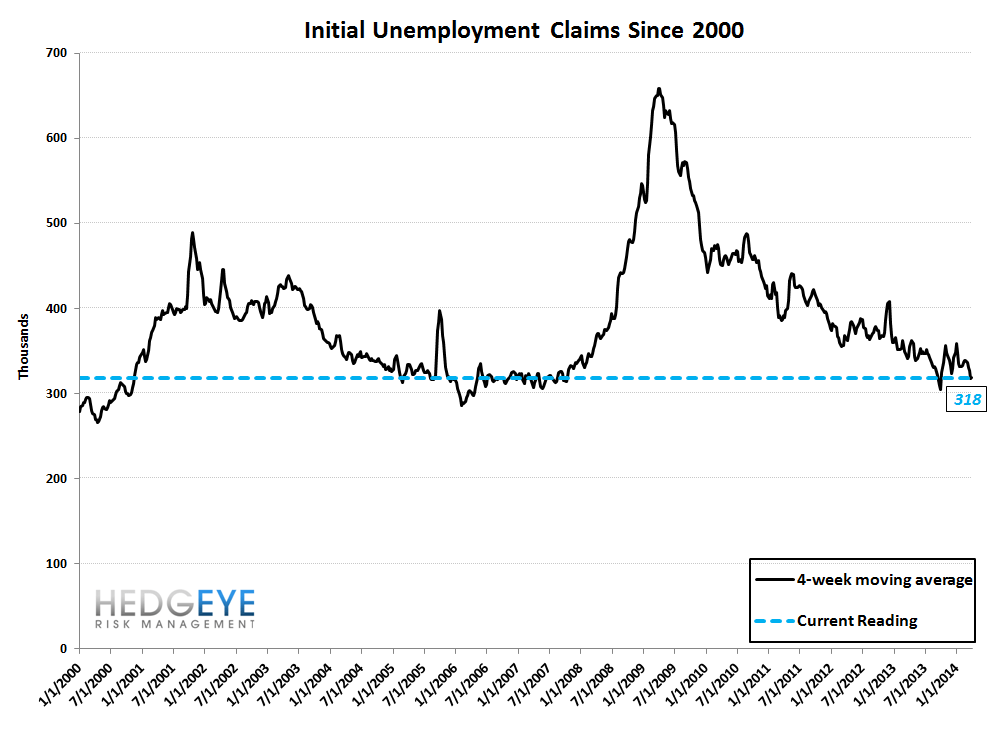

The headline (unrevised) number shows claims were higher by 16k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 0.5k WoW to 318k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -8.0% lower YoY, which is a sequential improvement versus the previous week's YoY change of -7.1%

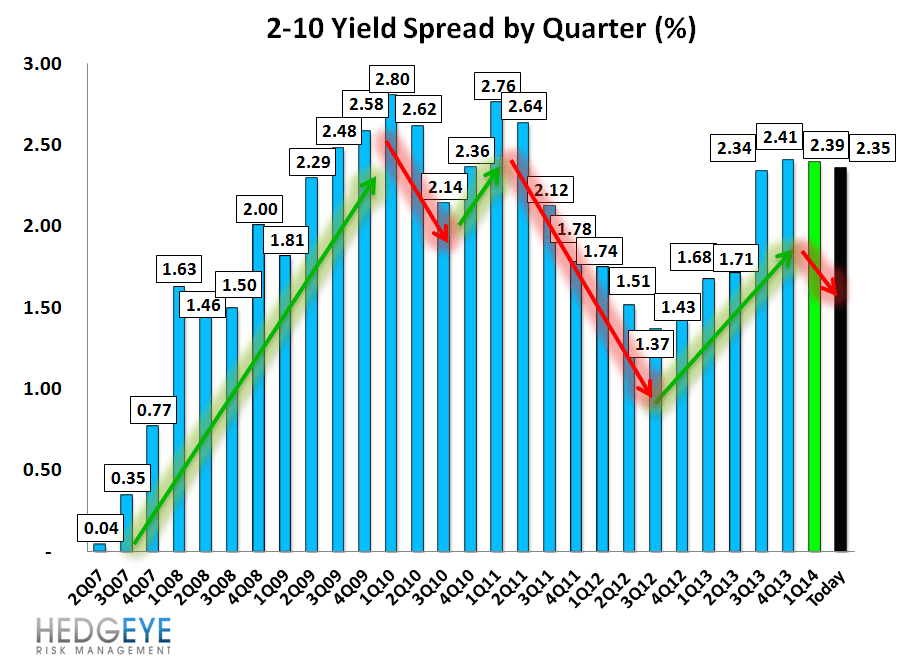

Yield Spreads

The 2-10 spread rose 10 basis points WoW to 235 bps. 1Q14TD, the 2-10 spread is averaging 239 bps, which is lower by -2 bps relative to 4Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT