TODAY’S S&P 500 SET-UP – April 3, 2014

As we look at today's setup for the S&P 500, the range is 29 points or 1.37% downside to 1865 and 0.16% upside to 1894.

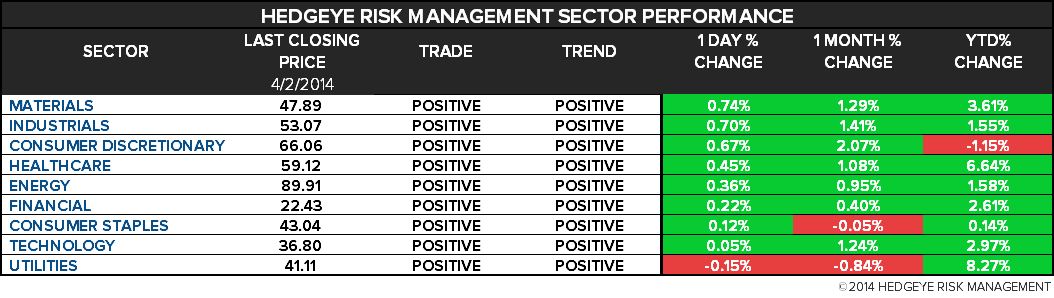

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.34 from 2.35

- VIX closed at 13.09 1 day percent change of -0.08%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: Challenger Job Cuts, y/y, March (prior -24.4%)

- 7:30am: RBC Consumer Outlook Index, April (prior 51.8)

- 8:30am: Trade Balance, Feb., est. -$38.5b (prior -$39.1b)

- 8:30am: Jobless Claims, March 29, est. 319k (prior 311k)

- Continuing Claims, March 22, est. 2.843m (prior 2.823m)

- Jobless claims benchmark revisions 2009-2013

- 9:45am: Bloomberg Consumer Comfort, March 30 (prior -31.5)

- 9:45am: Markit U.S. Services PMI, March final, est. 55.5 (prior 55.5)

- Markit U.S. Composite PMI, March final (prior 55.8)

- 10am: ISM Non-Manufacturing Index, March, est. 53.5 (prior 51.6)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

GOVERNMENT:

- 8am: U.S. Chamber of Commerce Foundation Aviation Summit

- Attendees incl: TSA Administrator Pistole, Delta CEO Anderson, Virgin founder Branson, Southwest CEO Kelly, Airbus Americas chairman T. Allan McArtor,W. Douglas Parker

- 9:30am: House Ways and Means Cmte holds hearing on Obama’s trade policy w/U.S. Trade Rep. Michael Froman

- 9:30am: CFTC to hold public roundtable to discuss Dodd-Frank

- Budget panels/testimony:

- 10am: House Energy and Commerce panel: Energy Sec. Ernest Moniz

- Senate Env./Public Wks Cmte considers drinking water protection bill (S. 1961)

- U.S. ELECTION WRAP: Donation Ruling May Aid GOP, Sunlight Says

WHAT TO WATCH:

- Draghi seen defying deflation risk in ECB decision

- China plans to support growth with rail spending, tax cuts

- Fed’s Bullard says inflation slowing may prompt taper delay

- Google trading symbols change today

- Credit Suisse restates 4Q loss U.S. tax probe charge

- NATO warns Russia force on Ukraine border building up

- U.S. opens criminal inquiry into Citigroup Mexico unit: NYT

- U.S. secretly financed social network in Cuba: AP

- Mobius says MSCI plan to add China domestic shrs is bad idea

- Sinopec said to pick Goldman Sachs for $30b retail sale

- Outbrain hires Goldman, JPMorgan for IPO in U.S.: FT

- Senate Finance Committee marks up tax extenders bill

- Iraq veteran kills 3 soldiers, self at Fort Hood in Texas

AM EARNS:

- Greenbrier (GBX) 6am, $0.61

- Hudson’s Bay (HBC CN) 7am, C$0.50

- Perry Ellis International (PERY) 7am, $0.03

- RPM International (RPM) 7:30am, $0.09

- Schnitzer Steel Industries (SCHN) 8:30am, $0.08

PM EARNS:

- Global Payments (GPN) 4:01pm, $0.95

- Micron Technology (MU) 4:05pm, $0.59 - Preview

- Seachange International (SEAC) 4:02pm, $0.02

- Synnex (SNX) 4:01pm, $0.94

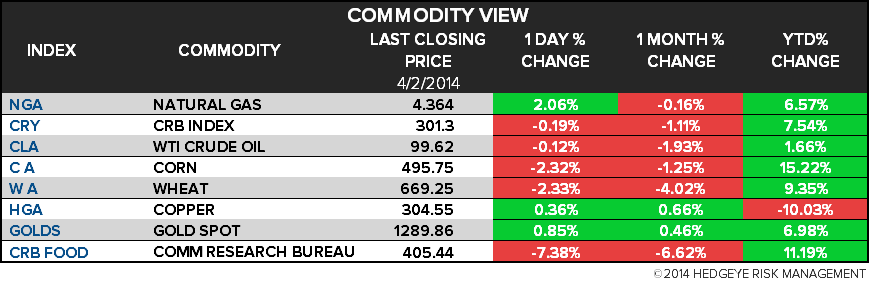

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Crude’s Premium to WTI Near Six-Month Low Amid Libya Talks

- Food Costs Jump to 10-Month High as Weather Hurts Beef to Wheat

- Pricey Wagyu Steaks Are Abe Answer to Cheap Imports: Commodities

- Tin Advances Most in Four Weeks as Withdrawal Orders Increase

- Gold Trades Near Seven-Week Low as Demand Weighed Against Data

- Wheat Extends Biggest Drop in Five Weeks as Rains May Aid Crops

- Sugar Declines for the Fourth Session; Cocoa Rises in New York

- Iron Ore Swaps Trading Rises to Record on Bets for China Growth

- Yamana Poised to Best Goldcorp in Osisko Bid: Corporate Canada

- Price War Seen as Thai Rice Glut Swamps Market: Southeast Asia

- Foreign Frackers Now Find Comfort in Water-Hungry Spain: Energy

- Gazprom’s $910 Billion Gaffe Shows Putin Economy Eroding Wealth

- Asia LNG Prices May Fall as Gail, Chubu Lead Joint Purchasing

- Rebar in Shanghai Climbs to 1-Month High on China Stimulus Plans

CURRENCIES

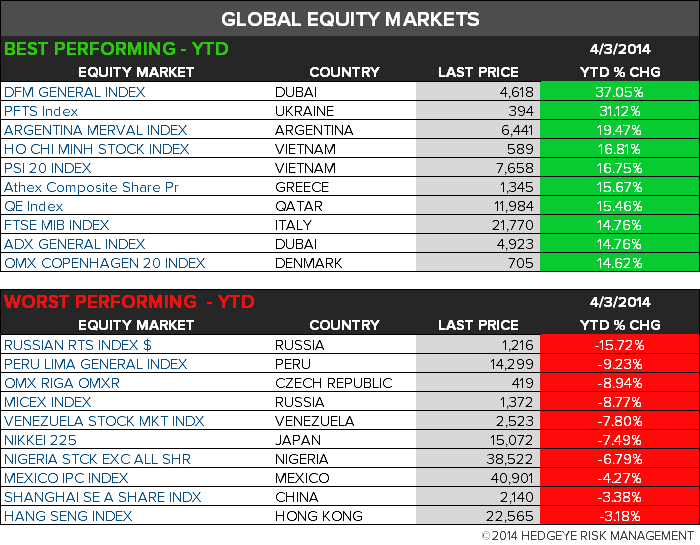

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team