Summary:

- Both incomes and spending decelerated in February while Core PCE inflation was static at a dovish, stall speed of just 1.1%.

- The income/spending deceleration was broad based with some negative weather drag, but the trend is one of deceleration and the primary pockets of spending strength in February are likely to be ephemeral.

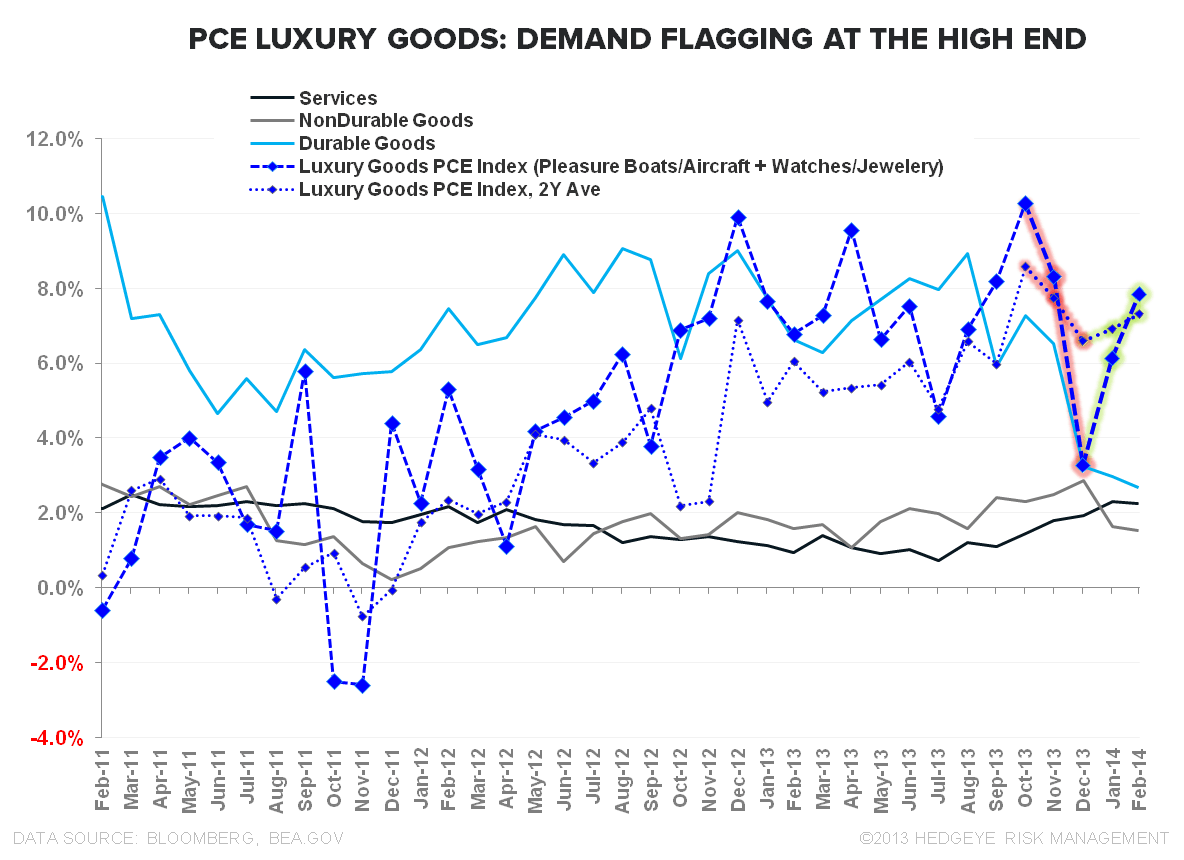

- High End Demand: It turns out that the rich are still pretty rich and high ticket discretionary spending saw a moderate bounce in February. Wealth effect spending, however, probably continues to ebb.

- Healthcare Spending: At ~19% of Total household expenditures, spending on Medical Care matters, and Obamacare is distorting the numbers.

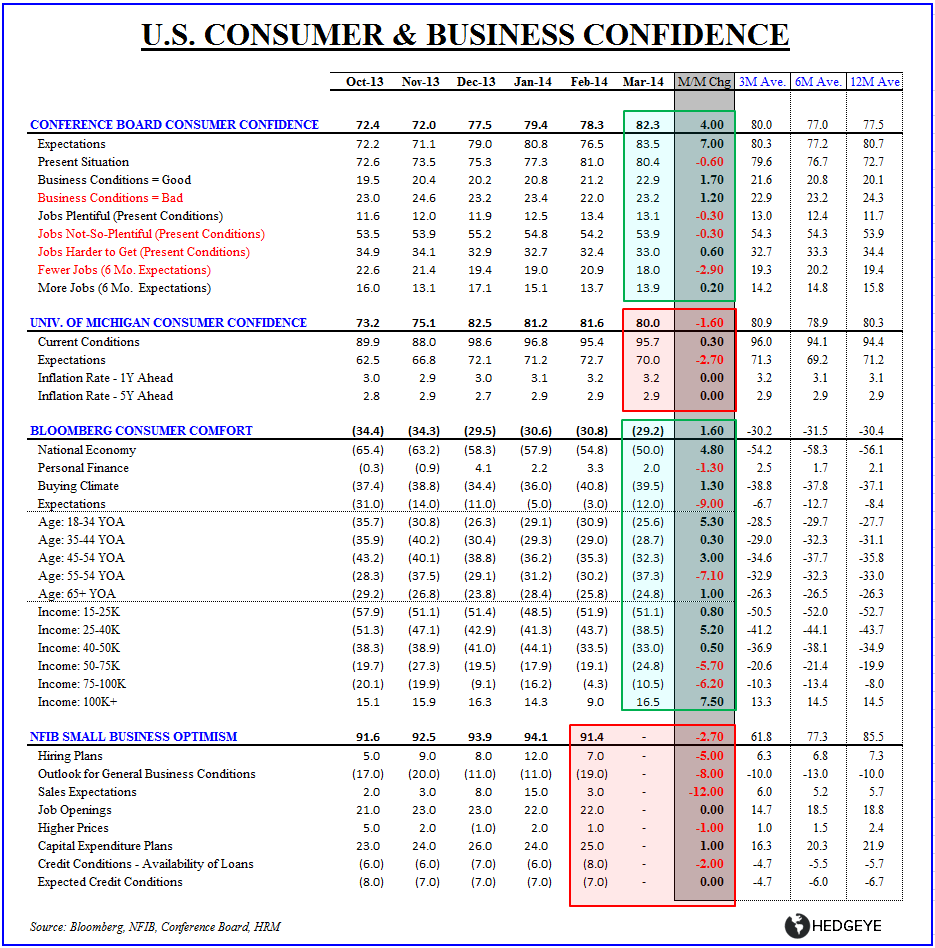

- Confidence: March marked a second month of mixed consumer confidence reports. Sentiment continues to meander alongside the dollars descent.

- FINALLY!: Outside of some lagging housing data, all the material domestic, fundamental macro data for February has been reported….enjoy the oversold bounce and blithely enter the weekend knowing the vexatious ubiquity of weather caveat-ed macro releases has finally ended.

PERSONAL INCOME: 3 Months of Deceleration

Weather probably served as a negative distortion on reported, aggregate personal income in February, but with total Personal Income, Disposable Personal Income (DPI), DPI per capita and Private Sector Salary & Wage growth all decelerating for the 3rd consecutive month in February it feels hard to argue that weather is masking a strong underlying trend of acceleration.

Private Sector Salaries and Wages decelerated by -60bps and -50bps on a YoY and 2Y basis, respectively, while aggregate government sourced wage income accelerated 30bps on a 1Y while holding flat sequentially on a 2Y basis.

Alongside the spending friendly budget deal and ongoing positive state & local government employment growth, we continue to expect government salary and wage income to provide some modest upside to income growth in 2014.

The savings rate ticked up to 4.3% from 4.2% but remains near historical trough levels.

The capacity for a further decline in savings to support incremental consumption growth remains very much constrained at current levels.

CONSUMER SPENDING: Healthcare & High End Discretionary supported February consumption expenditures. The former is either transient or likely to be revised significantly and the latter isn’t likely to repeat last year’s performance.

HIGH END DEMAND: Last month we highlighted the deceleration in demand at the high end as implied by the slowdown in spending on luxury durables.

As it turns out, however, the rich are still pretty rich and high ticket discretionary spending saw a moderate bounce in February (see yesterday’s note for more on the latest income division dynamics - INFLECTIONS OR FALSE POSITIVES?).

The read through here is mixed as the contribution to total durables growth from higher-end discretionary helped mask more broader weakness.

Further, with stocks flat YTD, housing decelerating and the Fed beginning to reign in their explicit, asset re-flation (i.e. wealth effect) policy agenda, the probability for the top income quartiles to provide incremental demand growth (in similar magnitude to last year) seems to be diminishing.

HEALTHCARE SPENDING: DISTORTED, TRANSIENT OR BOTH?

Spending on Healthcare Services has been the notable positive outlier over the last few month and the effect stems largely from the implementation of Obamacare.

The reported figures are very much an estimate and the preliminary data are likely to be revised significantly over time as the Census bureau’s quarterly QSS and annual SAS survey’s provide harder data.

With reported Hospital and Outpatient spending both accelerating materially, it could also be that individuals are accelerating medical consumption ahead of ACA implementation and uncertainty around coverage changes.

Either way, in the context of the broader spending data, the takeaway is pretty straightforward – Healthcare Services represent ~19% of total household consumption expenditures and certainly impacts the direction of reported, headline consumption growth.

To the extent that deceleration is the larger trend across the balance of services, a mis-estimation of ACA related spending and/or a significant, transient pull-forward in medical consumption could be materially distorting the prevailing, underlying trend.

Unfortunately, like the now ubiquitous weather asterisk, we’ll just have to hurry up and wait to get a clearer read on the magnitude of the impact.

CONSUMER CONFIDENCE: Across the primary survey's, March proved to be a second straight month of meandering for consumer confidence.

The final University of Michigan Consumer Sentiment reading for March declined -1.6pts sequentially to 80.0 – the worst reading in 4 months.

The conference board and Bloomberg Surveys, meanwhile, showed consumer confidence improving by 4pts and 1.6pts, respectively, in March.

Notably, the relationship between the $USD and confidence remains reasonably strong. The dollar is currently in Bearish Formation (Broken Trade, Trend & Tail) and with growth slowing and commodity inflation accelerating the balance of risk for the currency remains to the downside, in our view.

Christian B. Drake

@HedgeyeUSA