RETAIL FIRST LOOK: EXPECT THE UNEXPECTED

20 JULY 2009

TODAY’S CALL OUT

What are the stocks discounting from earnings season? Interestingly enough, they appear to be discounting that current earnings expectations are correct. It’s odd that we approach an earnings season and the earnings revision factor and stock performance are so closely in synch. That begs the question as to whether we will be sitting here in another month saying “gee, this earnings season was exactly in line with where every Tom, Dick and Harry thought it would be.” Something tells me that the answer here is an overwhelming ‘No.’ We’re officially entering the period where there will be meaningful bifurcations by company, and this will accelerate throughout the remainder of the year. It’s a stock-pickers game again, folks. This is where you get paid to know your companies, be meaningfully different than consensus (when appropriate), and most importantly, be right. We’ll be out with written comments on many of these in advance of earnings. Premium subscribers…you know where to reach me to discuss live.

LEVINE’S LOW DOWN

Some Notable Call Outs

- It looks like VF Corp will not announce that it won Eddie Bauer assets with its earnings release tonight. Golden Gate capital has emerged the winner at $286mm. Ironically, this is the same exact size bid it made 2-years ago, but was rejected by a judge. It looks like the economy has changed the rules of engagement. Yes, that seems low on a base of $1bn in revenue. But this is about 7x EBITDA on a grossly mismanaged asset whose relevance is in question. Should the brand exist? Probably. With more than $500mm in revs? Not so sure…

-CIT is getting all the press, but Steve Madden (SHOO) has dumped GMAC as its factor. That’s a shocker to me. Looks like SHOO is shifting away from factoring en masse and more towards utilizing its stellar balance sheet to sidestep and perceived ‘factor’ risk. You’ll see more of this from many mid-size companies that can afford to do so.

- In an unusual move within the Nike, Inc portfolio, Dwyane Wade switched from Converse to Brand Jordan. The move did not surprise me as much as the accompanying statement… "I didn't want to be in the Converse brand anymore because it seemed like they didn't know what to do with me." Could this be a sign of Converse reallocating capital from the performance business over to the classic segment in which it dominates? As evidenced by the deal with Target for expansion of One Star, I’m inclined to say yes. Don’t get me wrong, it’s tough to fault Converse for almost anything. People thought that Nike was foolish for buying the company 2 years after it otherwise could have scooped it up out of bankruptcy at half the price. But Nike is not good at fixing things. They’d rather pay more and not have to fix anything. The result? A near triple-digit return on its original investment. Nonetheless, let’s keep an eye on clearer definition between Converse and other Nike, Inc brands.

- As retailers and brands work to find the best use of social media, we are seeing companies actually reach out to their customers in new ways. It was reported on Friday, that privately held fast fashion retailer, Forever 21, asked its Twitter followers if they would be interested in a Forever 21 magazine. The questions even dug deeper asking what features and content these loyal customers would like to see in the “hypothetical” publication. Expect to see much more of this outreach as it presents a larger, cheaper, and potentially more targeted way for companies to reach their core constituents.

- Late last week the legal battle between Ebay and Tiffany re-emerged. In an effort to appeal a ruling from last year that favored Ebay, Tiffany presented its arguments claiming that Ebay should enforce more vigorous counterfeit controls. The judge ruled last year that Tiffany should be responsible for protecting its own trademarks. The appeals case was presented before a packed court house and is being watched closely. If the original ruling were to be overturned, it would be viewed as a monumental change in the balance of responsibility for fighting counterfeiting and huge victory for the trademark holders which historically have spent all of their own capital on countering the sale of fake products.

MORNING NEWS

- The controlling shareholders of Hong Kong-based sourcing giant Li & Fung are branching off into India's modern retail market - Fung Capital, controlled by Li & Fung’s controlling shareholders Victor and William Fung, said it would invest $30 million in Future Logistic Solutions Limited, which specializes in supplying fashion and other products to 1,100 retail doors. In a statement, they described the move as “unrelated to any of the Li & Fung Group companies.”Future Logistics, part of Future Group, operates 30 supply chains in fashion, food, home products and general merchandise. It also has joint-venture partnerships with stationery retailer Staples and French fashion chain Celio. Future Group is best known for Pantaloon Retail, one of India’s largest operators. India’s logistics market is valued at about $100 billion. <wwd.com/business-news>

- India has no intention of allowing foreign direct investment in retail - India has no plans to allow foreign direct investment in multi-brand retail trade, the country's junior commerce and industry minister said Monday. Under current policy, foreign direct investment is not permitted in retail trade except in single-brand product retailing where foreign investment up to 51% is allowed. "Government fully recognizes the need to ensure that small retailers are not adversely affected by the growing organized retail and that there is no adverse effect on employment," Mr. Scindia said. <online.wsj.com>

- Retailers report increased sales, conversions and return on ad spend - Online marketing company Channel Intelligence says its jewelry, apparel and sporting goods retail clients increased their return on ad spend in Q2 compared to Q1. <internetretailer.com>

- RVS buys Ellen Tracy brand from Brand Matter LLC - Brand Matter LLC has sold the operational part of the Ellen Tracy business to RVC Enterprises and licensed RVC for use of the brand for women’s sportswear in both the better and bridge categories. Mark Mendelson, president and chief executive officer of Ellen Tracy, will become president of the Ellen Tracy division of RVC. The operations will remain in Manhattan, where RVC is located. Market sources said there have been discussions for an Ellen Tracy line in the better category at Macy’s. But Brand Matter president Rick Platt said Ellen Tracy’s management has had conversations with a variety of retailers. <wwd.com/business-news>

- Geox North America plans - Six months after taking the helm at Geox North America, Gary Champion is working to invigorate the brand with fresh styling, new marketing and an aggressive retail push. The former Clarks executive, who joined the Italy-based label in February, told Footwear News he aims to “introduce the U.S. customer to the Geox brand.” The market has been a challenge for the company since its debut here five years ago — of Geox’s $1.2 billion in annual sales, North America accounts for less than 5%. The COO’s first move has been to strengthen the product. For spring ’10, the brand initiated its first collection made specifically for North America. It also moved away from traditional Euro-comfort styling to infuse more fashion into the line. “We did three different heights of wedge heels, with three to four patterns on each height,” Champion said. Price points will remain unchanged, in the $120-to-150 range, and Champion said he sees Tory Burch, Cole Haan and Sofft as the brand’s main competitors. To support the product overhaul, the North American team is strengthening product merchandising, starting in its own stores. (It has 30 to 35 in the U.S., with two dozen more slated to open in North America this year.) Champion said Geox will adjust the way product is displayed, in addition to implementing lifestyle messaging. <wwd.com/footwear-news>

- U.S. retailers may see spending drop in the back-to-school shopping season - 32% of U.S. consumers said they are saving more, up 10% from a year earlier, according to a survey being released today by Deloitte LLP. 64% said they would spend less on back-to-school items, compared with 71% last year. 22% said they would spend less because of a job loss in the household, Deloitte said in an e-mailed statement. Deloitte counts the back-to-school shopping period as running from the July 4 weekend to Labor Day in September. 65% said they will only buy what the family needs, according to the survey. That means spending less on clothes and shoes. Another 74% said that they will buy more of their items on sale. Consumers plan to seek out stores offering value. 90% of those surveyed said they will shop at discount department stores and 40% at dollar stores. Retailers need to be creative in promoting loyalty programs and offering coupons, Janiak said. More than three-quarters of shoppers will do the bulk of their shopping in August, she said. “Although retailers may not see as many wallets snapping shut as they did in late 2008, consumers still plan to stretch their dollars, telling us that their shopping remains constrained,” Janiak said in the statement. “Retailers should focus on delivering the best incentives and in-store experiences to get the most out of the back-to-school season.” <bloomberg.com>

- Philippines' Richest Man Henry Sy Plans to Expand Retail Empire in China - Billionaire Henry Sy, whose retail empire has made him the richest man in the Philippines, may build as many as three malls a year in China to expand in the first major economy to rebound from the global recession. <bloomberg.com>

- Urban Outfitters Would Consider Lending to Its Vendors if CIT Collapses - Urban Outfitters Inc., the clothing and housewares retailer, may consider providing short-term financing to some of its vendors should CIT Group Inc. collapse. <bloomberg.com/news>

- As consumer confidence continues to hit all-time lows, more marketers are getting into the insurance business - Last week, for instance, Hewlett-Packard began offering a “printing payback guarantee” which promises consumers a check if its printing solutions don’t deliver the recommended cost savings in a year. Earlier this month, Sears launched its “Buyer Protection Program,” which lets buyers keep an appliance purchased for more than $399 with a Sears card if the consumer loses his or her job. “Get a new appliance. Get peace of mind,” the program’s landing page proclaims, adding, “The Sears Blue Appliance Crew has got your back.” Kevin Brown, CMO for Sears’ home appliances division, said the incentive was necessary to get consumers to buy. “It really came from listening to our customers who have been telling us that…they’re worrying about their jobs and the economy,” Brown said, noting that consumers are “deferring much needed appliances and bigger ticket purchases.” Sears and HP aren’t the first to try to address consumers’ sagging confidence. Brands ranging from Virgin Mobile to men’s clothing retailer Jos. A. Bank have been running similar offers in recent months. The catalyst appears to be Hyundai, which trumpeted the idea the loudest with its Super Bowl “Assurance” spot, which outlined a program in which the automaker offered to buy back consumers’ cars should they lose their jobs within a year. Addressing consumers’ concerns about their jobs is an unusual marketing tack. Jack Trout, president of Trout & Partners, said he has never seen anyone making such offers before in previous recessions. “It just shows you how tough it is out there,” he said. “It shows you how people’s minds have changed.” Yet programs essentially telling consumers, “We’ve got your back,” have emerged in large numbers. <brandweek.com>

- London retail sales boosted by good weather- Clothing and footwear sales also benefited from discounting and Sales, according to BRC/KPMG’s London Retail Sales Monitor. The sales increase bucked the overall trend in the UK which saw an increase of 1.4% in June. The figures also showed that footfall in central London in June was up on last year. The BRC added that the sterling’s weakness against the euro had continued to attract international visitors to the capital, especially from Western Europe. However, it added that tourists were more cautious with their spending. BRC director general Stephen Robertson said: “Sunshine and sales helped boost London retail sales. Footfall in the capital was well up on a year ago, as shoppers sought out summer clothes, sandals and other goods.” “The pound’s weakness against the euro continued to attract shoppers from western Europe. And sales in the capital were also helped by Middle Eastern visitors. Although individual tourists have become more cautious, there are more of them which produced sales gains.” For the three months from April to June, like-for-like retail sales in London rose 3.9%. <drapersonline.com>

- The European managing director of Crocs has spoken out against negative reports - US newspaper The Washington Post wrote an article last week suggesting that the brightly coloured footwear phenomena may have reached its maturity in the market place and could be on its last legs. Other newspapers suggested that the iconic footwear brand, which launched just seven years ago, was close to bankruptcy, claiming that because the shoes hardly ever wore out there was no need for repeat purchases by customers. In response to the article, managing director of Crocs Europe, Robin Akeroyd issued a statement which said he was “extremely confident” in the future of the company. He added: “Crocs is here to stay and has continually invested in product development which has generated constant demand. <drapersonline.com>

- One Star, a new fall apparel collection by Converse, will be available exclusively at Target stores this September - The all-American sportswear line will include men's and women's apparel and accessories, including denim, graphic tees, plaid tops, zip-ups, dresses, outerwear, fringed scarves and hobo bags. Footwear also will roll out for men, women and children. Converse's One Star for Target debuted in February 2008. <licensemag.com>

- Retail stocks see new calculus on investors' hopes - Frugal shoppers are still fixated on discounters, not their upscale fashion and home furnishings competitors. Investors, however, are no longer so certain. Mall-based purveyors like J.C. Penney and Macy's Inc. are now back on the hot list of investors, who have pushed prices up in recent months as they turn to the beaten-down shares in the belief they don't have much farther to fall and could be big winners in a rebound. Still, shares of many of these mall-based merchants are still far below the levels they traded at since the recession started in late 2007. And analysts say their honeymoon may soon be over as investors grow impatient with the persistent sales slump and profit declines. "Retailers have to show investors the money," said Ken Perkins, president of retail consulting firm Retail Metrics LLC. "At some point, they have to show (profit) growth." Perkins estimated that the retail industry is expected to record an earnings decline of 11.6 percent for the second quarter compared with a year ago, marking the ninth consecutive quarter of earnings declines. Excluding Wal-Mart Stores Inc., that decrease would be almost 18 percent. While the earnings declines have moderated in recent quarters, investors are concerned about the financial health of retailers and are hoping for some signs of a turnaround this back-to-school season. <boston.com/business/articles>

- Footwear brands expanding scope into accessories - Having options is a mantra that footwear brands, from Steve Madden to Salvatore Ferragamo, are embracing as they branch further into categories that don’t have anything to do with feet. Even as an unstable economy rocked the retail market this past year, Steve Madden developed a line of bedding targeted to college-age girls, and Ferragamo expanded its fragrance collection to include home offerings such as candles and room spray. For spring ’10, Shane and Shawn Ward are tackling timepieces, while Tory Burch continues to build her lifestyle empire, with eyewear for fall. And designers Elizabeth Brady and Matt Bernson have spun out into handbags and jewelry, respectively. “Brands are trying to find an opportunity to sustain their volume and keep the cachet of their brand alive,” said Marshal Cohen, chief industry analyst at The NPD Group. “But stretching out into other categories doesn’t always mean a home run.” While the risks include diluting the brand message and tainting relationships with retailers that expect a focused story, Cohen said, product expansion could boost sales, particularly among consumers already buying into the brand. “That’s where most of the growth will come from,” he said. “You’ve already convinced them you are the brand for them.” <wwd.com/footwear-news>

- Outdoor companies focusing a bit more on the female consumer style - Whitney Conner said she first knew something needed to change during a visit to the Patagonia campus. Conner, the brand manager for Patagonia footwear, noticed that none of the female staffers at Patagonia’s Ventura, Calif., headquarters were wearing the brand’s more outdoorsy casual footwear. To get them and other women excited about its shoe collection, the brand this season will debut its new Elegance casual line, featuring more dressed-up, fashion-conscious silhouettes. And Patagonia isn’t the only one. Many leading outdoor firms are taking another look at their women’s casuals, aligning them more with current trends and giving the traditionally rugged styles a more feminine, polished look. Brand executives said the new direction better suits their female consumers’ need for style and functionality — and updated styles and colors give them a reason to buy. Portland, Ore.-based Keen’s ongoing push toenhance its feminine styling has ramped up this season. For Patagonia, the wakeup call led to a new direction: making the footwear collection better sync up with the dresses being shown in the apparel line. “When we looked at trending things, it became clear it was time to step away from the Outdoor Group and get into a more feminine, sophisticated look that matched the Patagonia dress line,” Conner said. <wwd.com/footwear-news>

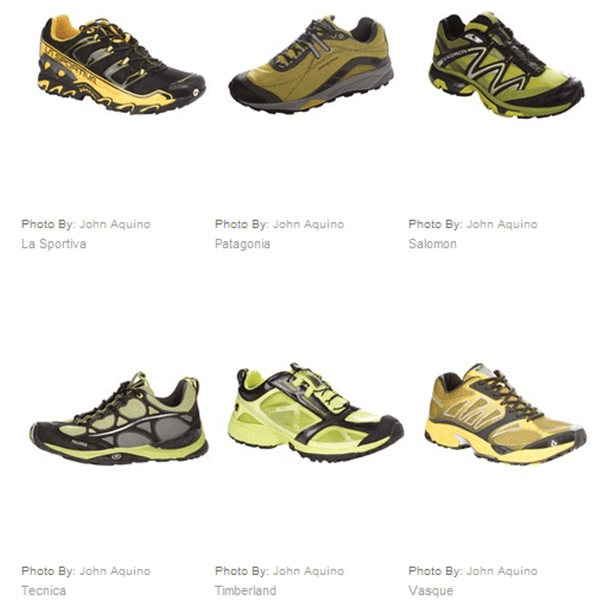

- Outdoor Trend: Bright Colored Shoes - Runners taking to the trails for spring will be doing everything but blending into the scenery. Bright citrus shades of lemon-yellow and lime-green are juicing up performance trail runners.

INSIDER TRADING ACTIVITY:

ROST: Gary Cribb, Executive VP & COO, sold 90,057shs ($4.1mm) after exercising the right to buy 90,057shs less than 20% of common holdings.

ROST: Lisa Panattoni, Executive VP of Merchandising, sold 40,000shs ($1.7mm) after exercising the right to buy 40,000shs less than 20% of common holdings.

ROST: Barbara Rentler, Executive VP of Merchandising, sold 58,557shs ($2.5mm) after exercising the right to buy 58,557shs less than 20% of common holdings.

RBI: Williams Lockhart, Director, purchased 2,304shs ($20k) increasing common holdings by ~100%.

TJK: Ernie Herrman, SEVP & Group President, sold 20,000shs ($68k) after exercising the right to buy 20,000shs representing less than 20% of common holdings.

MACRO SECTOR VIEW AND TRADING CALL OUTS