TODAY’S S&P 500 SET-UP – March 18, 2014

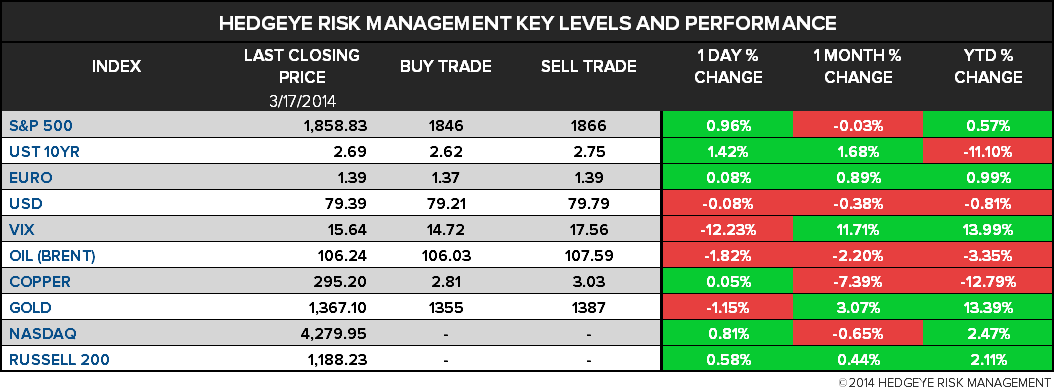

As we look at today's setup for the S&P 500, the range is 20 points or 0.69% downside to 1846 and 0.39% upside to 1866.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.32 from 2.33

- VIX closed at 15.64 1 day percent change of -12.23%

MACRO DATA POINTS (Bloomberg Estimates):

- Federal Open Market Cmte begins 2-day mtg

- 7:45am: ICSC weekly sales

- 8:30am: CPI m/m, Feb., est. 0.1% (prior 0.1%)

- CPI Ex Food and Energy m/m, Feb., est. 0.1% (prior 0.1%)

- 8:30am: Housing Starts, Feb., est. 910k (prior 880k)

- 8:30am: Building Permits, Feb., est. 960k (prior 937k, revised 945k)

- 8:55am: Redbook weekly sales

- 9am: Net Long-term TIC Flows, Jan., est. $40.0b (pr -$45.9b)

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- 8am: SEC Chief Economist Craig Lewis speaks at ICI

- 8:30am: David S. Cohen, U.S. Treasury undersecretary for terrorism & financial intelligence speaks on virtual currencies at Bloomberg event

- 9am: RNC Chairman Reince Priebus at Christian Science Monitor

- 10am: DNC Chairwoman Rep. Debbie Wasserman Schultz at Natl Press Club

- US. Election Wrap: Illinois Race; Ads by Billionaires

WHAT TO WATCH:

- Federal Open Market Cmte begins 2-day mtg

- High-speed trading said to face New York probe over fairness

- Russia creeps towards economic crisis as sanctions near

- Malaysia Air disappearance among longest in modern aviation

- Obamacare reshuffles insurance market share, report says

- Wal-Mart plans video-game trade-in service March 26

- Amazon to start selling video-streaming device in April: WSJ

- Microsoft said to unveil Office for IPad on March 27

- Target to sell products simultaneously with TV shows: NYT

- Rep. Camp’s bank tax plan under attack from Wall St.: WSJ

- Shell, Phillips 66 purchase majority of SPR oil sale

- Italy may cut F-35 JSF order to 45 vs 90, Corriere says

EARNINGS:

- Adobe Systems (ADBE) 4:05pm, $0.25 - Preview

- Alimentation Couche Tard (ATD/B CN) 8:40am, $0.92

- DSW (DSW) 7am, $0.29

- FactSet Research Systems (FDS) 7am, $1.22

- Hertz Global Holdings (HTZ) 6am, $0.32

- Oracle (ORCL) 4:01pm, $0.70 - Preview

- Pacific Sunwear of California (PSUN) 4pm, ($0.19)

- Renren (RENN) 6pm, ($0.12)

- Yingli Green Energy Holding Co (YGE) 6am, ($0.18)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Extends Retreat From Highest in Six Months Before Fed Meets

- Gold-Mining ETF Outshines Bullion Fund as Haven Bet: Commodities

- Brent Trades Near Six-Week Low as Crimea Risk Fades; WTI Steady

- Nickel Heads for Bull Market as Russia Clouds Supply Outlook

- Corn Rebounds in Chicago Trading, Erasing Earlier Declines

- StanChart Sees Global Sugar Deficit in 2014-15 of 1 Mln Tons

- Ukraine Tackling Gas Corruption Means Potatoes for Poor: Energy

- Default Risk for China Copper Financing Seen Low: StanChart

- European LNG Imports Fell to 9-Yr Low in 2013 as Prices Rose: BG

- French Flour Miller Vivescia Sees Market for Sustainable Wheat

- April Jet Fuel Swaps Drop to Eight-Month Low: Asia Distillates

- EU Mulls Renewables-Linked Aid to 62 Industries, Draft Shows

- Thai Rice Crops Damaged as Drought Spreads Across 28 Provinces

- Rebar Rises 1st Time in 3 Days on China Seasonal Demand Outlook

- Agricultural Commodities Could Be “Next Big Story,” HSBC Says

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team