Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

---

Relative Differences

The Russia/Ukraine/Crimea situation continues driving relative performance differences within the US Financials sector. Note the first callout below. The US global banks are underperforming while the domestically-focused institutions are outperforming, which is essentially the opposite of our preferred positioning. Meanwhile, Sberbank of Russia, which is essentially the Russian banking system, is seeing its CDS rise dramatically. Separately, the yield spread is compressed markedly last week.

If there is one silver lining domestically it is that commodity prices finally stopped going up, posting a 1% decline for the week. It's also worth mentioning that the US and EU interbank markets remain benign.

European Financial CDS - Swaps mostly widened in Europe last week. Sberbank of Russia widened significantly, increasing 54 bps to 340 bps and finds itself now squarely in the red zone of +300 bps. Sberbank swaps are now wider by 103 bps month-over-month. Consider that Sberbank is to Russian banking what JPMorgan, BofA, Citi and Wells Fargo combined are to the US from a market share standpoint. Sberbank's credit default swaps are a helpful proxy for the Crimea situation.

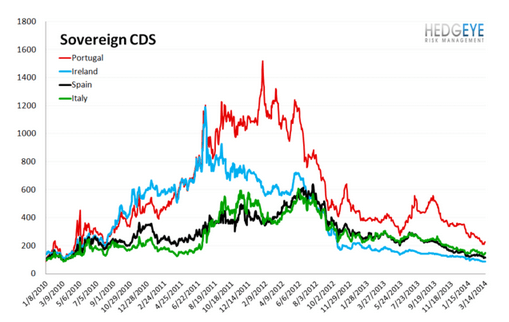

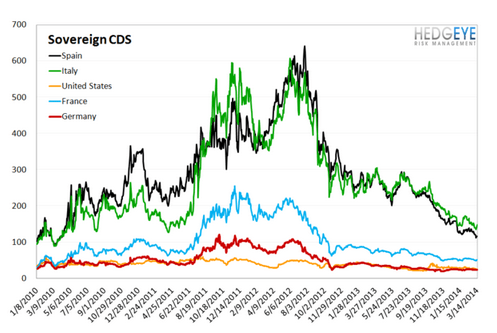

Sovereign CDS – Sovereign swaps mostly widened over last week. The two exceptions included the US, which tightened 1 bp and Spain, which tightened 5 bps.

Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 2 bps to 14 bps.

Matthew Hedrick

Associate