This year we've been cautious in pointing out the risk premium associated with owning Russia, yet assertive that Russia's commodity based economy stands to benefit greatly from commodity reflation, a major theme of ours in the first half of this year.

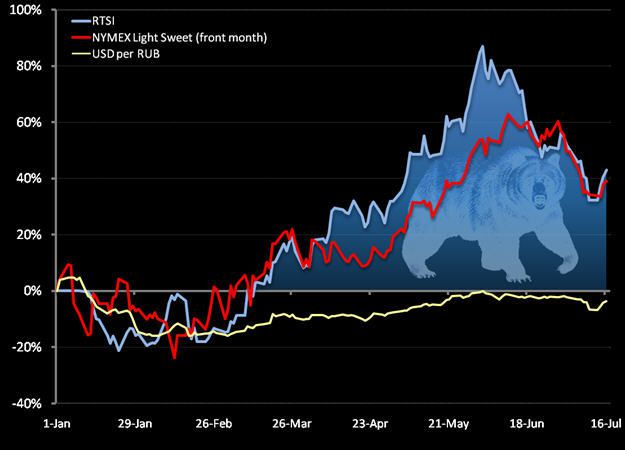

The Russian stock market (much like other countries that are paid in petrodollars) has followed the price of oil like a hawk year to date, with a correlation coefficient (R squared) of .94 between the RTSI and the continuous front month light sweet crude contract (see chart). This year we've frequently commented on Russia's performance as it vied for the best performing global market with the other BRIC components, until it began pulling back in concert with oil. Starting June 1st the RTS declined 28.5% with oil down 12.0% in the same period, before catching a bid this week, up 10.6% on oil's 6.4% run.

While the price of energy commodities and metals remain the central catalyst for the Russian market, we're equally watching the country's underlying economic fundaments as we believe they'll drag down performance on an intermediate and TAIL (3 years or less) basis, especially should oil stay under our TAIL resistance level of $67.78/barrel.

This week the Russia's Economy Ministry updated its economic forecast. Whether the information is completely creditable or not is a matter of discussion in itself, however the Ministry reported that GDP may decline 8.5% this year, after contracting 9.8% Y/Y in Q1 (the most in 15 years) and that Russia may not match last year's growth until 2012.

On the ground industrial production was down 17% in May, with the IMF forecasting unemployment at 13% this year. Wage arrears rose 10.8% and according to a study by Moscow's Higher School of Economics--and not surprisingly--Russia is seeing a rise in labor unrest with a recorded 99 labor disputes in the first five months (nearly the same level as in all of last year).

While the data may be questionable, the country's demographics support a grim picture for future growth. The World Bank reported that by the end of this year 17.4% of the population (24.6 Million) will live beneath the subsistence level of $185 per month, about 5% more than before the crisis. Additionally the Economy Ministry said Russia's working population will annually decrease by ~1 Million every year over the next three, and the population will continue to decline, as it has over the last 14 years; last year the population stood at 141.9 Million.

From a fiscal and monetary perspective Russia is certainly trying to weather the storm, but we'd argue that the Kremlin is not doing enough. The country issued a stimulus package of more than 2.5 Trillion Rubles ($80 Billion -a puny amount in context), and has reduced interest rates to stem the blockage in credit lending. Over the last three months Bank Rossii has cut interest rates three times, shaving off 50bps to 11% in its last cut on July 10th.

The chart below helps to frame the USD-RUB dynamic along with the price of oil. Certainly the Central Bank has played a large role in manipulating the Ruble's value over the last year, having drained some $200 Billion (1/3 of the country's foreign-exchange reserves) from August to January to stem the Ruble's slide versus the dollar as oil came down off its summer highs. Most recently, the bank reported that international reserves slid by $8.4 Billion to $400.7 Billion last week, the largest decline in almost in six months, as the Bank attempts to strengthen the Ruble.

All of this action begs the question: to what extent the Central bank is willing to support a strong Ruble policy (and ensure it trades below the high side of its trading band of 26 to 41 against a basket of Euros and Dollars) if oil continues to fall? On one hand, Russia has the reserves to support currency, yet the bank has no control over investors who may flee due to the volatility of a economy levered to energy prices.

Make no mistake, the Russian stock market is focused squarely on Oil and Gas, yet our work in global macro has taught us that a country's fundamentals drive market performance in the long run. As outlined, on the TAIL there are real risks in the Russian economy and, perhaps more importantly, real political risks to investing there.

In the immediate term, we will continue to analyze all data points -large or small, made up or not, as we look for signals on the margin that may change our stance.

Matthew Hedrick

Analyst