“The future is here. It’s just not evenly distributed yet.”

-William Gibson

While you might think it’s 1999. It’s not, yet. According to the Wall Street Journal yesterday, 74% of companies that have come public in the last 6 months don’t make money. So it’s not the mother of all bubbles, yet – because in 2000, that percentage was 80%.

The aforementioned quote comes from the beginning of chapter 1 of a fantastic book I reviewed in the Early Look a few years ago titled, The World in 2050 – Four Forces Shaping Civilization’s Northern Future, by Laurence C. Smith.

My defense partner, Daryl G. Jones, will be hosting Mr. Smith on an Institutional Conference Call at 1PM EST today. Please ping if you’d like access. Global water shortages and NORCs (Northern Rim Countries) will be focus topics, not Candy Crush’s pending $7 billion dollar back-to-the-future-bubble IPO.

Back to the Global Macro Grind…

The Dow Jones Index is -1.4% YTD and Gold is ripping (+14.1% YTD). The US Dollar is being burnt to a crisp (fresh YTD lows) this morning too. Calling the froth in the US equity market (companies trading at 20x revenues with no earnings) is getting easier, by the day.

But have no fear, the future of America is here.

And it’s definitely not evenly distributed. That’s why the politicians who have devalued America’s currency are focused on whining about the “inequality” that their policies created. That’s what Policies to Inflate do. They pay the bailed out banker who is bringing Crush public, and they pulverize the poor.

But everyone reading this rant is rich, right? So just suck it up and buy inflation protection (TIP) or Gold (GLD) or anything that looks like a bond (Utilities, XLU) as you try to keep up with Elmer Fudd’s pesky wabbit (inflation).

But, but, the SP500 rallied into the close yesterday (on no-volume), and is up +1% YTD:

- Yep, who cares?

- It was led by Utilities (XLU) which ripped a +1.3% move for the home team on the day (+6.1% YTD)

- And Consumer Discretionary (XLY) stocks closed down -0.15% to -0.16% YTD

That’s right, “Duck Wabbit, Duck!”

You can go back to the future and remind yourself that this happened in both Q1 of 2008 and 2011. If you’re American, your economy is now the rabbit. You have to burn your savings and just buy whatever you can that will inflate at a faster rate.

Cool, eh? Go flip a house before prices crash again.

Larry Smith will walk through the nonsense of all this groupthink on our conference call today, but here’s the upshot about civilizations who starve long-term investment for the sake of short-term-pay-me-now-Kinder-Morgan-dividend pops….

- They create unintended consequences (i.e. underinvestment in long-term fixed capital projects that have positive ROIC)

- Which, in turn, create shortages in critical capacity

- Which then perpetuate #InflationAccelerating

I know, paying $2.89 for a bottle of water isn’t inflationary. Eat an iPad.

And if you’re not into the whole Republican/Democrat, Nixon-Carter, Burning Buck and US Debt Monetization thing, move to a country that gets what both Reagan and Clinton did – like New Zealand!

BREAKING NEWS: New Zealand Raises Key Rate to Become 1st Developed Nation To Tighten

Love that.

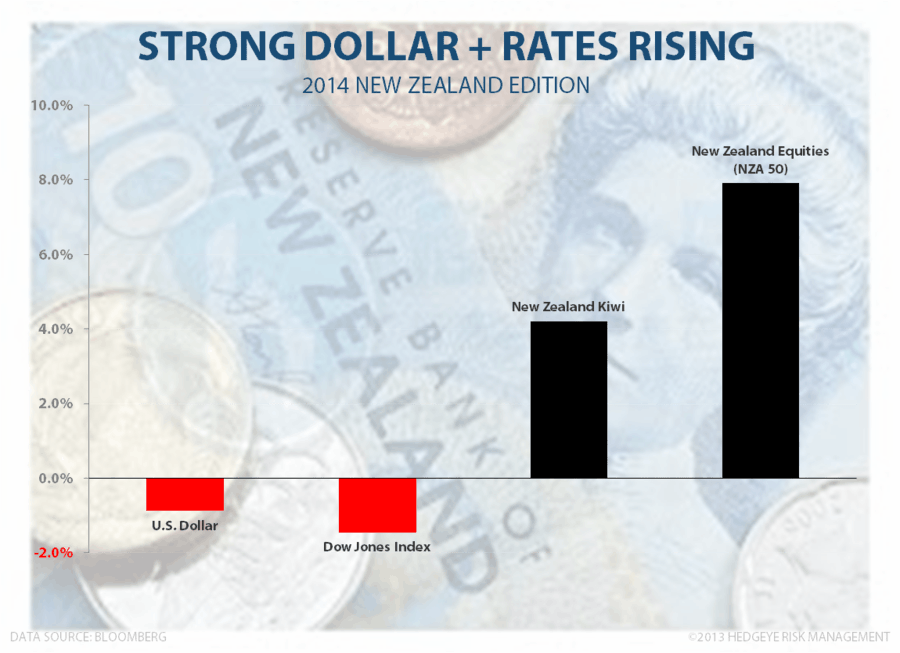

Oh, and the New Zealand stock market must have gotten crushed on #RatesRising, right?

Nope:

- New Zealand raised rates on savings accounts with a +25 beep bump to 2.75% on its base rate

- The New Zealand Kiwi (it’s currency) strengthened alongside interest rates

- The New Zealand stock market closed UP on the day to +7.9% YTD

So why bang your head against a wall trying to call the Dow “cheap” when its down YTD and you can buy a country’s currency and stock market that is emulating the best of the best in American pro-growth 1980s and 1990s policy history?

As Marty (Michael J. Fox) said in Back To The Future, “maybe you weren’t ready for that… but your kids are going to love it.”

Our immediate-term TRADE risk ranges across Global Macro are now as follows:

UST 10yr Yield 2.60-2.80%

SPX 1

VIX 13.18-15.75

USD 79.31-80.11

Brent 106.37-110.44

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer