We were recently given a look at February sales trends, which are, on the margin, negative for the casual dining industry. Same-restaurant sales and same-restaurant traffic trends declined during the month and were down sequentially from January. Before we delve further into the details, we thought it would be useful to highlight which casual dining chains had CQ (current quarter) same-restaurant sales estimates adjusted since February 3rd.

None of the casual dining companies we track had CQ same-restaurant sales estimates revised up over the course of February.

The following companies had CQ same-restaurant sales estimates unchanged over the course of February: EAT, KONA

The following companies had CQ same-restaurant sales estimates revised down over the course of February: BBRG, BJRI, BLMN, BWLD, CAKE, CBRL, CHUY, DRI, DFRG, DIN, IRG, RRGB, RT, RUTH, TXRH

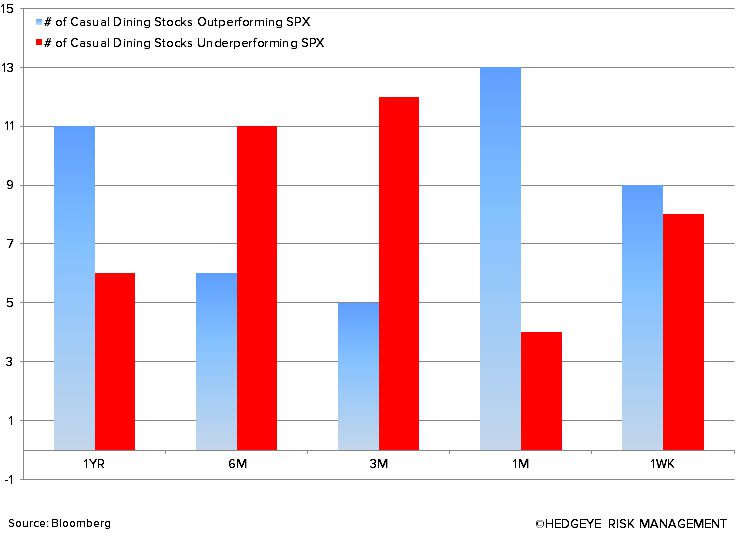

Despite these negative revisions, casual dining stocks have outperformed the SPX meaningfully over the past month, which implies, to us, that the street has accepted the fact that 1Q will be a difficult quarter. More importantly, it also implies that expectations are high for the remainder of 2014.

February marks the third consecutive month of decreasing same-restaurant sales and traffic for the industry. As we wrote last week, Knapp estimates same-restaurant sales and traffic declined -1.5% and -4%, respectively, during the month. In addition, Black Box Intelligence, which excludes DRI, estimates same-restaurant sales and traffic declined -0.7% and -3.2%, respectively, during the month. February numbers contracted on a year-over-year basis despite facing some of the easiest comparisons in over three years. According to historical Black Box data, same-restaurant sales and traffic declined -5% and -6.2%, respectively, in February 2013.

After a tumultuous January, New England was surprisingly the best performing region during the February month with Black Box estimating same-restaurant sales and traffic increased +2.2% and 0%, respectively. The West Region, on the other hand, was the weakest performing market with Black Box estimating same-restaurant sales and traffic declined -3.7% and -5.8%, respectively, in February.

Overall, trends in the casual dining industry are unsettling and continue to indicate what we believe is a secular decline in the industry as the rise of fast casual and evolution of traditional quick-service continue to steal share from the industry. Despite this, the market has shrugged off any weakness as weather-related.

To be clear, we believe 1Q14 has been negatively impacted by weather, but to what extent is largely unknown. With that being said, we believe the street has appropriately taken down 1Q14 estimates to a reasonable level. Although January and February were difficult months for the industry, we believe March will provide some back end support to aggregate first quarter numbers.

2Q14 estimates currently appear aggressive to the naked eye, but we will reserve judgment until March numbers are released as we expect it to be a telling month for the industry overall. Will the industry get a boost from all the “pent-up demand” we are hearing about or will the secular decline persist? Unfortunately, we don’t yet have an answer to this, but we will continue to monitor the situation closely and comment upon any indicators that may suggest one or the other.

Howard Penney

Managing Director

Fred Masotta

Analyst