With EBITDA margins trailing the competition by an average of 500bps, some shareholder pressure should not be a surprise. But will the new Activist be successful?

We’ve long thought that BYD was ripe for activist shareholder involvement. In fact, we’ve had discussions with such activists but the major push back has been major insider ownership - around 40%. BYD is an operational underperformer and should either put the right management team in place or sell the company to a better operator. Will Bill Boyd acquiesce or even sell? That remains to be seen but he is in control.

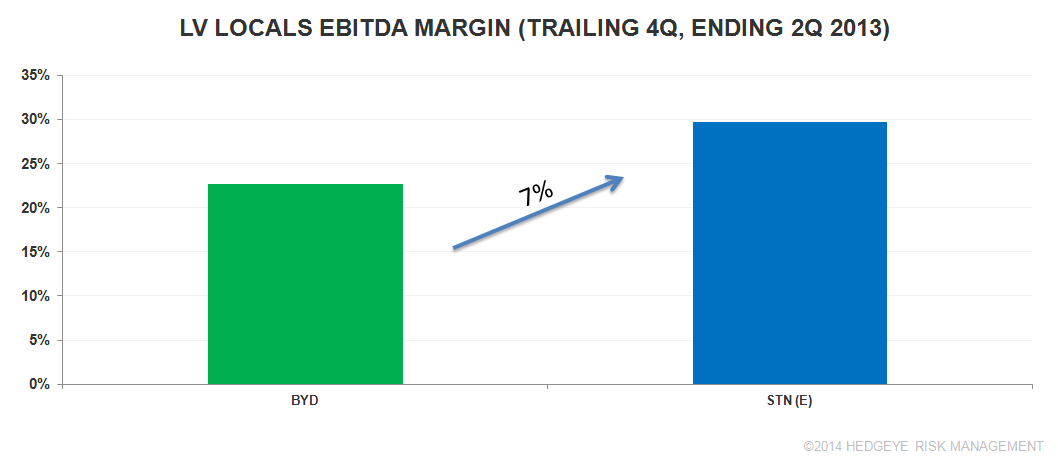

The reality is that BYD underperforms its competition both at the company level in terms of EBITDA margin as well in each of its markets. BYD’s property EBITDA margin trails the average competitor in most of the company’s markets by 200-800bps. Moreover, gaming revenue per position also falls short of the competition by up to 10%.

With the right operating team in place, we estimate BYD could enhance EBITDA by $110 million to $150 million, or $8 to $10 of equity value. BYD closed at $11.80 yesterday and while the stock will no doubt be up in the morning, considerable upside will still remain if operational changes are made and even more through the sale of the company. We’re pretty sure GLPI would take a look.

For an activist looking for BYD to pursue its own REIT split, we would view that as unlikely. BYD's debt levels are too high and significant NOLs remain. BYD is likely 3 years away from even considering that option

The following charts show BYD’s underperformance. Note that the data used for this analysis covers 2013/2013. Given the PNK acquisition of ASCA and the PENN/GLPI split, it seemed more comparable and easier to present. We believe the margin differential hasn’t changed much.