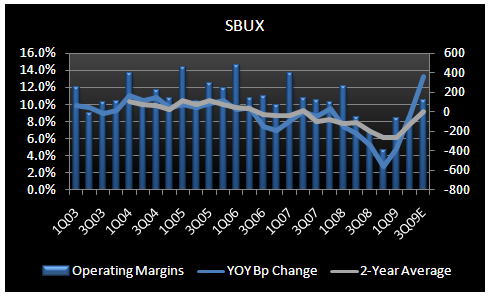

SBUX is scheduled to report fiscal 3Q09 numbers after the close next Tuesday, July 21 and I would expect the company to continue the trend of beating EPS expectations ($0.22E vs. consensus of $0.19) despite continued weakness in top-line numbers. Fiscal 3Q09 should mark a return to double digit operating margins, the first quarter of YOY operating margin improvement for SBUX since 4Q07 and the company's U.S. segment should post its first quarter of margin expansion following 12 quarters of declines. And, this is based on my expectation of a 5%-6% decline in U.S. same-store sales, which would signal a sequential improvement from the 8% decline in 2Q09.

The real benefit to margins in the quarter and going forward will stem from the company's goal to eliminate $500 million of costs in FY09, $345 million of which should be implemented by the end of 3Q09. Although SBUX will continue to feel some pressure on the cost of sales line as a result of the fixed cost nature of occupancy costs, lower dairy and coffee prices should minimize the deleveraging effect of continued same-store sale declines.

With the company having launched its first national advertising campaign in May (mid Q3), I am most interested in hearing about how the campaign is being received and the impact it is having on driving customer traffic. Specifically, was the company successful in continuing its trend from 2Q of reducing traffic losses on a sequential basis? My 5%-6% U.S. same-store sales decline estimate relies on a quarterly sequential improvement in traffic. Easier YOY comparisons, new advertising, the company's first limited time promotion of iced coffee for $1.95 (initiated in May through the end of the quarter) and the results from my May "Grass Roots Survey" all make me comfortable with this assumption.

SBUX management commented on last quarter's earnings call that the marketing campaign "will build over time" so I am not expecting that the marketing will have made a big impact on Q3 results, but increased communication to consumers can only help. The company did state that it is not significantly increasing its advertising spend and instead, it is making a long-term investment. As I have said before, I think SBUX needs to spend $300-$400 million in the U.S. to have a share of voice that will make it competitive with its peers. Although Starbucks will not get to this level of spending right away, I would like to hear more about the direction and magnitude of the new advertising campaign, which I think is essential to the long-term success of the brand.

From a cash flow perspective, SBUX should continue to demonstrate its ability to generate significant cash even in a tough environment. With an estimated 25% YOY decline in capital spending, SBUX should be able to pay down more debt in the quarter and further strengthen its balance sheet.