TODAY’S S&P 500 SET-UP – March 6, 2014

As we look at today's setup for the S&P 500, the range is 31 points or 1.38% downside to 1848 and 0.28% upside to 1879.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.38 from 2.37

- VIX closed at 13.89 1 day percent change of -1.49%

MACRO DATA POINTS (Bloomberg Estimates):

• 7am: RBC Consumer Outlook Index, March (est. 50.4)

• 7:30am: Challenger Job Cuts y/y, Feb. (prior 11.6%)

• 8:15am: Fed’s Dudley at Wall St. Journal event in New York

• 8:30am: Non-Farm Productivity, 4Q final, est. 2.2% (pr 3.2%)

• 8:30am: Initial Jobless Claims, Feb 28, est. 336k (prior 348k)

• 9:45am: Bloomberg Consumer Comfort, March 2 (prior -28.6)

• 10am: Factory Orders, Jan., est. -0.5% (prior -1.5%)

• 10am: Freddie Mac mortgage rates

• 10:30am: EIA natural-gas storage change

• 12pm: Household Change in Net Worth, 4Q (prior $1.922t)

• 1pm: Fed’s Plosser speaks in London

• 6pm: Fed’s Lockhart speaks in Washington

GOVERNMENT:

- President Obama to speak on economy, healthcare

- 9am: House Foreign Affairs Cmte hears Treasury, State, USAID officials on U.S. foreign policy, Ukraine

- 9:30am Jack Lew testifies on FY15 budget at House Ways & Means Cmte

- 9:30am: Defense Sec. Chuck Hagel at House Armed Svcs Cmte

- 10am: House Small Business workforce subcommittee holds hearing, “ObamaCare and the Self-Employed: What About Us?”

- 10am: Medicare Payment Advisory Commission meets

- 12pm: Airline Pilots Assn President Lee Moak discusses state of airline industry at National Economists Club

- Election Wrap: Romney backs Ernst in Iowa, Texas Primary

WHAT TO WATCH:

- EU to consider Ukraine sanctions; Russia spurns U.S. diplomacy

- Buffett cuts bond allocation as Berkshire warns on low yields

- Bouygues offers $14.4b cash for SFR to rival Drahi’s bid

- IMF said to demand greater say on Greek banks in ECB wrangle

- GM weighs increasing South Korean car exports to Australia

- Sinclair TV ownership model said targeted for breakup by FCC

- Darden cancels analyst, investor mtg amid pressure: Reuters

- Virgin America CEO Cush sees IPO late 3Q: Reuters

- Jack Lew testifies on FY15 budget proposal

- Feb. U.S. retail sales likely “lackluster,” hurt by weather

- VTB cancels NY forum as U.S. relations over Ukraine sour

- Multi-billion dollar LNG plants at risk over fuel price tussle

- Rolls-Royce says DOJ probing bribery allegations: Telegraph

AM EARNS:

- Canadian Western Bank (CWB CN) 8:30am, C$0.65 - Preview

- Ciena (CIEN) 7am, $0.06 - Preview

- CST Brands (CST) 7am, $0.51

- Joy Global (JOY) 6am, $0.65 - Preview

- Kroger (KR) 8:45am, $0.72 - Preview

- Pinnacle Foods (PF) 8am, $0.58

- SNC-Lavalin Group (SNC CN) 8:27am, C$0.64

- Stage Stores (SSI) 6am, $0.99

- Staples (SPLS) 6am, $0.39 - Preview

PM EARNS:

- Alon USA Energy (ALJ) 6pm, ($0.14)

- Ambarella (AMBA) 4:05pm, $0.19

- Analogic (ALOG) 4:15pm, $1.20

- Checkpoint Systems (CKP) 4:02pm, $0.31

- Constellation Software/Can (CSU CN) 4:30pm, $2.50

- Cooper Cos. (COO) 4:01pm, $1.46

- Finisar (FNSR) 4pm, $0.44

- Fresh Market (TFM) 4:02pm, $0.42

- H&R Block (HRB) 4:03pm, ($0.11)

- Korn/Ferry International (KFY) 4:01pm, $0.34

- Quiksilver (ZQK) 4:01pm, ($0.06)

- Spectrum Pharmaceuticals (SPPI) 4pm, ($0.11)

- Thor Industries (THO) 4:15pm, $0.34

- W&T Offshore (WTI) 5:20pm, ($0.14)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Ukraine’s Revolutionary Farmers Back Home in Time to Plant Crops

- Chinalco’s Sun Sees Aluminum Industry ‘Shakeout’ as Prices Drop

- WTI Falls for Third Day as U.S. Oil Supplies Gain; Brent Stable

- Syrup Sours as Rules Menace World’s Oldest Branding: Commodities

- Palm Reserves in Malaysia Falling to Five-Month Low; Prices Rise

- Copper Trades Below One-Week High Amid China Growth Concern

- Gold Trades Below Four-Month High as Investors Weigh Ukraine

- Coffee Tops $2 in Surge to Two-Year High on Brazil Drought Woes

- India Mills Cut Sugar Production Estimate 4.8% to 23.8 Mln Tons

- Off-Radar Iron Ore Exports Helping Hasten Global Market Glut

- Frackers May Gain From U.S.-EU Free Trade Accord, Opponents Say

- Europe’s Russia Gas Flows Jump to Month High as Buyers Hoard

- Crude Gains Evaporate as Russia Seen Too Big to Sanction: Energy

- Sugar Mills in India Reduce Output Estimate as Rains Hurt Yields

CURRENCIES

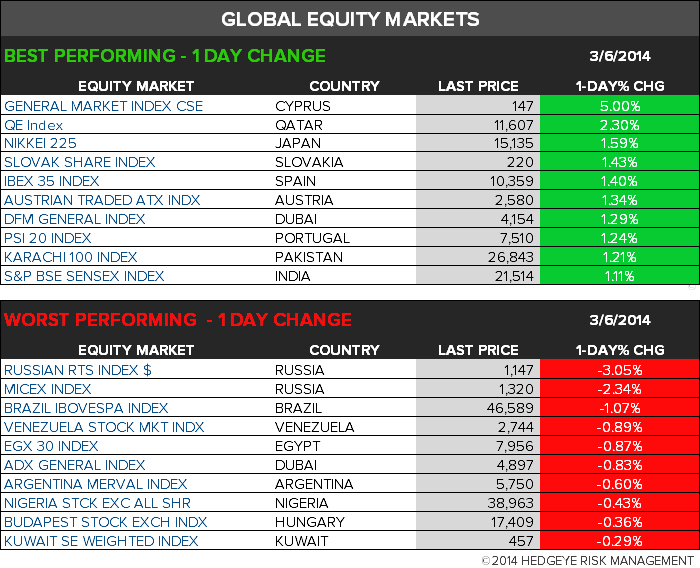

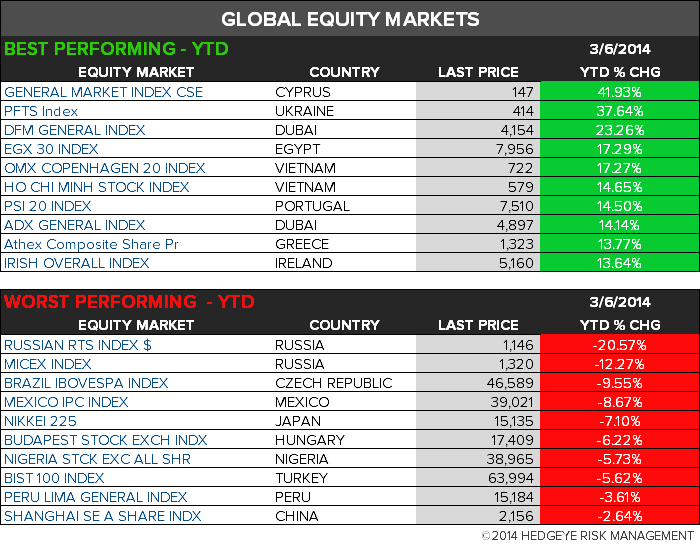

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team