Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

---

Not So Fast:

Just when it was looking like it was safe to get back in the water. The Ukraine suddenly matters (a lot) to investors, with Europe off 2-3% and S&P 500 futures down ~20 handles. We've been, on the margin, arguing for a more defensive posturing in light of what had been rising interbank, systemic risk measures, rising commodity prices and falling yield spreads. The concerns were initially prompted by the EM fears that surfaced roughly a month ago. Since then we've been erring on the side of caution while the XLF has grinded a few percent higher. This morning, serendipitously, that call appears to have been right. The reality is that through the end of last week some of the risk measures we track were starting to flash the all clear, but in light of the Ukraine situation, we'll hold the line. It doesn't hurt to wait and watch in the short term.

European Financial CDS - Aside from a few minor exceptions, European bank swaps were tighter last week, compressing by an average 3 bps (2 bps median decline). The month-over-month change in Europe is more impressive, as much of the Continent's banking system is now seeing double digit M/M declines.

Sovereign CDS – Sovereign swaps across Europe tightened notably last week, while the rest of the world was largely uneventful with the US and Japan widening just one basis point.

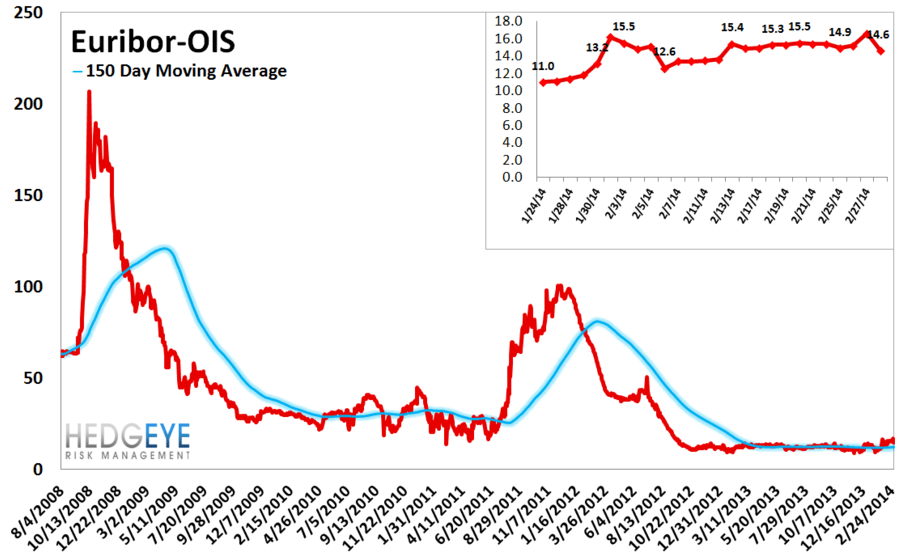

Euribor-OIS Spread – The Euribor-OIS spread tightened by 1 bps to 15 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

Matthew Hedrick

Associate