TODAY’S S&P 500 SET-UP – March 3, 2014

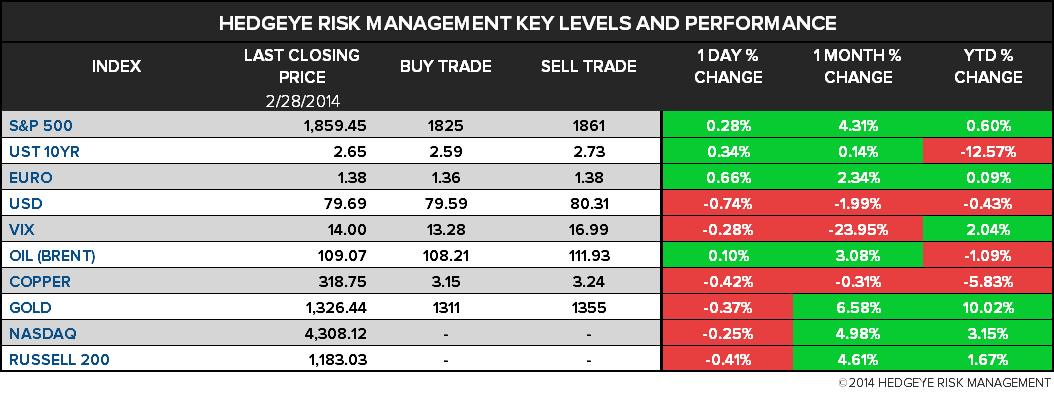

As we look at today's setup for the S&P 500, the range is 36 points or 1.85% downside to 1825 and 0.08% upside to 1861.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.30 from 2.33

- VIX closed at 14 1 day percent change of -0.28%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Personal Income, Jan., est. 0.2% (prior 0.0%)

- 8:30am: Personal Spending, Jan., est. 0.1% (prior 0.4%)

- 8:58am: Markit U.S. PMI Final, Feb., est. 56.7

- 10am: ISM Manufacturing, Feb., est. 52 (prior 51.3)

- 10am: Construction Spending m/m, Jan., est. -0.5% (prior 0.1%)

GOVERNMENT:

- U.S. government to close D.C. offices on weather. Events may be delayed or postponed.

- Obama urges Netanyahu to make Mideast peace now

- Xi seeks terrorism crackdown after deadly China knife attack

- N. Korea fires 2 short-range missiles off E. Coast: South

- 8:30am: Netanyahu, Senate Foreign Relations Cmte Chairman Robert Menendez deliver remarks during morning session of American Israeli Political Action Cmte policy conf.

- 11am: House Ways and Means Chairman Dave Camp attends briefing on tax code changes hosted by Institute for Policy Innovation

- 3:30pm Energy Dept holds FY 2015 budget briefing

- Obama, Netanyahu meet to discuss Israeli-Palestinian peace talks, Iran

WHAT TO WATCH:

- Kerry heads to Ukraine as U.S. considering Russia sanctions

- PepsiCo, Gazprom face sales threat on Ukraine standoff

- Putin grab for Crimea shows trail of signs West ignored

- Ukraine tension seen stoking energy costs on supply concern

- Riverbed said to get buyout interest above Elliott’s offer

- Banks’ corporate-bond sales said to face SEC favoritism probe

- Google, Samsung said to express MSFT-Nokia concern to China

- J. Crew said to hold sale talks with Fast Retailing

- Uniqlo billionaire push for global crown fuels J. Crew talks

- Buffett sets fresh goal as Berkshire misses 5-yr target

- Roche to halt MetMab lung cancer trial after study failure

- Obama said to trim budget request for struggling CFTC

- Sbarro said to ready bankruptcy filing as mall traffic slows

- Mexico said to question Citi workers in Oceanografia probe

- Home Depot’s new president said to be groomed as CEO successor

- Microsoft’s Nadella said to shake up staff with Penn role

- Gap plans to expand in China w/up to 35 new stores: WSJ

- Tablet sales rise 68% in 2013, Apple mkt share falls: Gartner

- EPA said poised to lower U.S. sulfur limits on fuel

- HSBC China Feb. manufacturing PMI 48.5, matching estimate

- Macau casino rev. jumps to record after Chinese new year

- Neeson’s ‘Non-Stop’ tops Lego film for N.A. box office lead

- ‘12 Years a Slave’ Wins Academy Award for 2013 Best Picture

- Winter storm missing New York set to bring worst to Washington

- Feb. U.S. auto sales: Chrysler ~8am, Ford ~9:30am, GM ~10am

AM EARNS:

- Akorn (AKRX) 6am, $0.14

- Celldex Therapeutics (CLDX) 8:03am, ($0.28)

- Rockwood Holdings (ROC) 6:30am, $0.32

- Stillwater Mining Co (SWC) 8am, $0.06

- Stratasys (SSYS) 6:30am, $0.49

- WP Carey (WPC) 8am, $0.57

PM EARNS:

- Ascena Retail Group (ASNA) 4:02pm, $0.21

- AuRico Gold (AUQ CN) 4:37pm, break-even

- Guidewire Software (GWRE) 4:01pm, $0.02

- MBIA (MBI) 4:01pm, $0.17

- McDermott International (MDR) 4:10pm, $0.16

- PDL BioPharma (PDLI) 4:02pm, $0.41

- URS (URS) 4:05pm, $0.18

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Commodities Climb to Six-Month High as Oil, Corn Rise on Ukraine

- Brent Crude Surges as Ukraine Tension Escalates; WTI Advances

- Hedge Funds Most Bullish on Gold Rally in 14 Months: Commodities

- Copper Reaches Three-Month Low as Manufacturing Slows in China

- Palm Oil Export Growth Stalling in Indonesia on Biodiesel Surge

- Gold Climbs to Four-Month High as Ukraine Tension Boosts Demand

- Sugar Falls as Delivery Seen Showing ‘Dire’ Demand; Coffee Rises

- Wheat Advances With Corn as Ukraine Crisis Threatens Shipments

- Rebar in Shanghai Rises as Chinese Lawmakers Meet on Policies

- U.S. Natural Gas Rises a Second Day on Storm, Ukraine Escalation

- Ukraine Tension Seen Stoking Oil, Gas Prices on Supply Risk

- Gold Miners See Looming Output Drop After Cut in Spending

- Oil at $100 Loss Warning Rejected by Norges Bank: Nordic Credit

- Iron Ore Supply May Increase 50% by 2018, Model Shows

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team