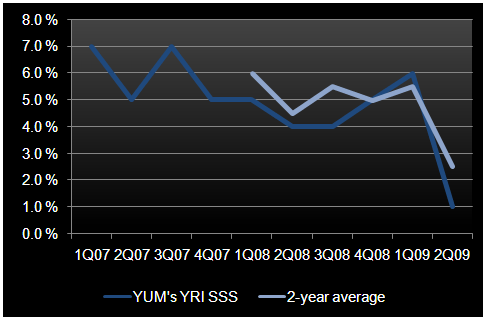

YUM management can talk all it wants about what it is going to do to fix KFC and Pizza Hut, but the reality is that the company needs to slow its growth. Same-store sales are one of the factors that make up the sustainability model and with trends like you see below it should be done sooner rather than later. Senior management compensation is dependent on growth in system wide sales, so it is not likely to change its tone any time soon. Unfortunately, the longer YUM grows without acknowledging the real issues, the worse things will get.

With the stock looking down today following YUM's beating 2Q EPS expectations but missing on the top-line, we are seeing a shift in pattern as the trend has been for companies' stock prices to outperform after reporting weaker than expected revenue performance but having cut costs enough to report in line or better than expected earnings.