EVENTS TO WATCH

- DECK - Earnings Call: Thursday 2/27, 4:30pm

- GPS - Earnings Call: Thursday 2/27, 5:00pm

COMPANY NEWS

NKE - Manu Ginobili Rips Through His Shoe While Playing Defense

(http://bleacherreport.com/articles/1975034-manu-ginobili-rips-through-his-shoe-while-playing-defense)

Takeaway: Seriously, is that even possible? Nike is going to have a PR field day with this one. No doubt that Manu will want some special mock-up of a shoe design to ensure that this never happens again. UnderArmour and AdiBok must be pumped.

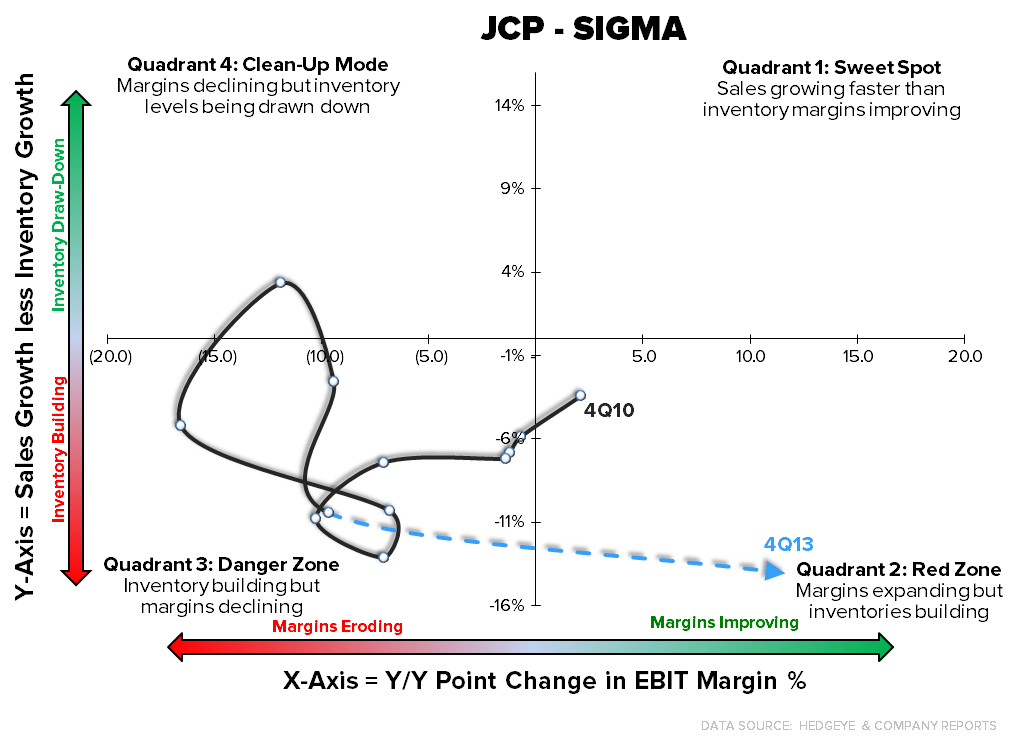

JCP - 4Q Earnings

JCP bulls were definitely due for a win, and they definitely got one today. The quarter itself was nothing to write home about, but the reality is that several key line items improved on the margin -- and for a company like JCP, that's all that matters. We were less thrilled with elements of the company's cash flow, but net/net still think this was a positive event -- especially given the carnage in the retail space. *Link to our note on JCP (JCP: The Scoreboard Doesn't Lie)

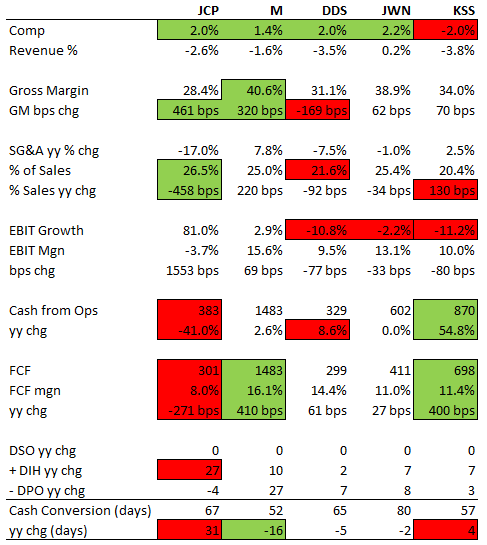

DEPARTMENT STORE 4Q COMPARATIVE ANALYSIS

SHLD - 4Q Earnings

SHLD's print was a little like JCP's but with far less emotion on the short side. It bear revenue estimates, which is the first time we've seen that in a while from SHLD, though it was in the context of a -6.4% comp -- by far the worst out of the department store group. EBITDA was $12mm vs $429mm last year -- no that's not a typo. They printed a loss of $0.96, which is far better than the Street at -$1.60. But in fairness, the Street was only 2 estimates.

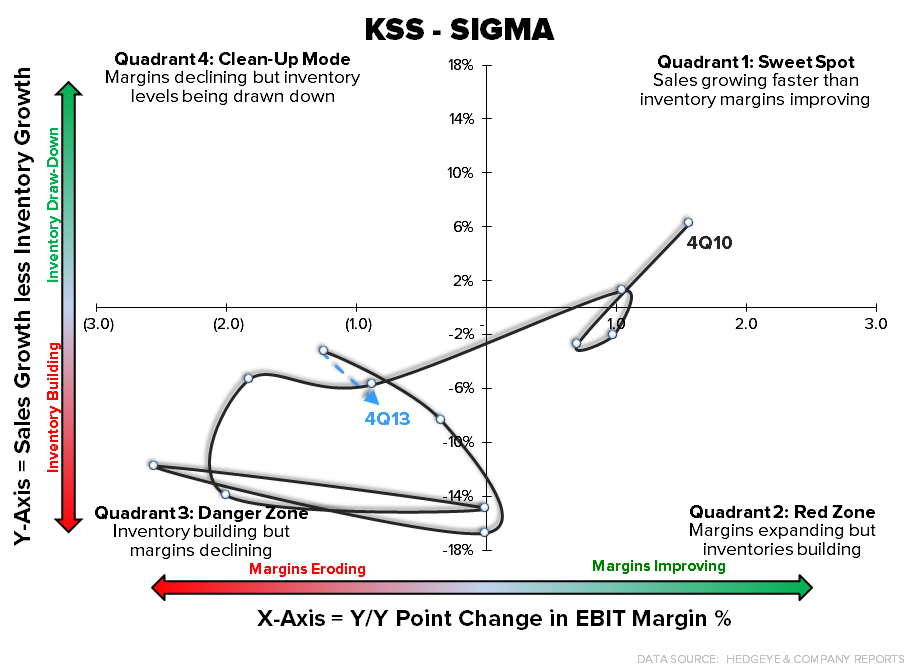

KSS - 4Q Earnings

KSS' 4Q was the most in-line out of its peer group. One standout is that comps were -2%, but every other department store (sans SHLD) was within 40bps of +2%. KSS definitely broke that trend. We're most concerned with guidance, which stands at 0.5%-2.5% comp growth for the year. Please, timestamp us on this one…there's no way that comps are positive in 2014. The only way we get there is if there is a meaningful decline in Gross Margin, which KSS didn't exactly forecast either. The crux of our argument rests in our work that shows that KSS took upwards of $800mm in share away from JCP over the past two years. JCP wants it back. It will either a) succeed, or b) drive down KSS' gross margins while it tries. Either way, it's not a pretty ending.

MW, JOSB - Financing for Eddie Bauer Buyout Gets Delayed

(http://blogs.wsj.com/moneybeat/2014/02/26/financing-for-eddie-bauer-buyout-gets-delayed/)

- "Goldman Sachs Group Inc. has postponed its efforts to syndicate a $400 million loan that would help finance Jos. A. Bank Clothiers Inc.’s acquisition of fellow retailer Eddie Bauer, according to people familiar with the matter, after the proposed takeover was challenged in court."

- "The people didn’t give a reason for the postponement, but it comes after a development in a court case that cast the timing of the Eddie Bauer deal in doubt."

Takeaway: Financing gets delayed because the deal should never have happened -- and it won't happen -- either because of Men's Wearhouse, or the courts.

BBY - Best Buy cutting 2,000 managers

(http://nypost.com/2014/02/26/best-buy-cutting-2000-managers/)

- "The nation’s biggest electronics chain...has begun laying off thousands of midlevel managers nationwide as it girds for even more competition, The Post has learned."

- "No store closings are planned in this latest round of cuts, and the exact number of pink slips hasn’t yet been confirmed. But one insider said layoffs could affect upward of 2,000 managers and supervisors."

BBBY - Bed Bath & Beyond Inc. Names Eugene A. Castagna - Chief Operating Officer, Susan E. Lattmann - Chief Financial Officer, Renews Employment Agreements With Co-Chairmen

(http://phx.corporate-ir.net/phoenix.zhtml?c=97860&p=irol-newsArticle&ID=1903979&highlight=)

- "Bed Bath & Beyond Inc. today announced the promotion of Eugene A. Castagna, previously the Company's Chief Financial Officer and Treasurer, to the role of Chief Operating Officer. Susan E. Lattmann, formerly the Company's Vice President – Finance, has been promoted to Chief Financial Officer and Treasurer."

Versace - Blackstone nears deal to buy into Versace

(http://www.ft.com/intl/cms/s/0/c5afd514-9f21-11e3-84feab7de.html?siteedition=intl#axzz2uT0xMgXg)

- "...Blackstone is nearing agreement to buy a minority stake in Italian luxury group Versace...The Versace family, led by creative designer Donatella Versace, was on Wednesday expected to grant exclusivity to the New York-based fund manager to purchase a 20 per cent stake in the company, said two people with knowledge of the talks."

- "Blackstone’s offer may value the Milan-based designer at as much as €1bn including debt, one of the people said. A deal has yet to be finalized, however, one of the people cautioned."

DLIA - Valinor Management Takes Stake in Delia's

(http://www.wwd.com/fashion-news/fashion-scoops/valinor-management-takes-stake-in-delias-7515889)

- "Valinor Management LLC has picked up an 18.7 percent stake in teen/tween specialty store Delia’s Inc. and will nominate two individuals, including Valinor’s Seth Cohen, to the firm’s board of directors."

- "Valinor disclosed the stake of nearly 14.4 million shares in the retailer in a regulatory filing with the Securities and Exchange Commission Wednesday. The second board nominee will be from outside Valinor but approved by Tracy Gardner, Delia’s chief executive officer."