“The important thing in life is not victory but combat; it is not to have vanquished but to have fought well.”

- Pierre de Coubertin

We’ve been a little quiet commenting on the ongoing Winter Olympics in Sochi, Russia. For Keith and me, it is probably nervousness over whether our native Canada can defend her Olympic gold, despite a lackluster preliminary round performance (lackluster in the sense that Canada is the first nation of hockey). More broadly, though, the paradoxical nature of global markets has kept us busy.

In part, the Sochi Olympics represent this paradox. Admittedly, from a security perspective, the games have been much more successful than anyone expected. (As far as I can tell, the one downside is that most hotels rooms have a picture of Russia President Vladimir Putin.) The flip side to the better than expected security (except perhaps in the Ukraine), is that many venues have been disappointing.

This of course goes to the heart of the paradox of the winter Olympics in Sochi, which is that Sochi is actually a beach resort. Our partner in the Phoenix Coyotes, George Gosbee, has been in Russia since the start of the games. He took a fantastic picture that was picked up by Reuters (see below) showing the beautiful Sochi beach line that spectators walk on to get to the hockey arenas.

We will be doing an Olympic hockey pool later this week at Hedgeye and the odds are that our own Bob Brooke has the inside edge given his experience playing for the U.S.A. at the Sarajevo Olympics in 1984, but here are my picks:

- Gold – U.S.A.

- Silver – Canada

- Bronze – Russia

- Sweden

While it is paradoxical for a Canadian to pick the U.S. to win gold, they have looked much better, so I’m not going to let my emotions rule the day. What are your picks?

Back to the Global Macro Grind . . .

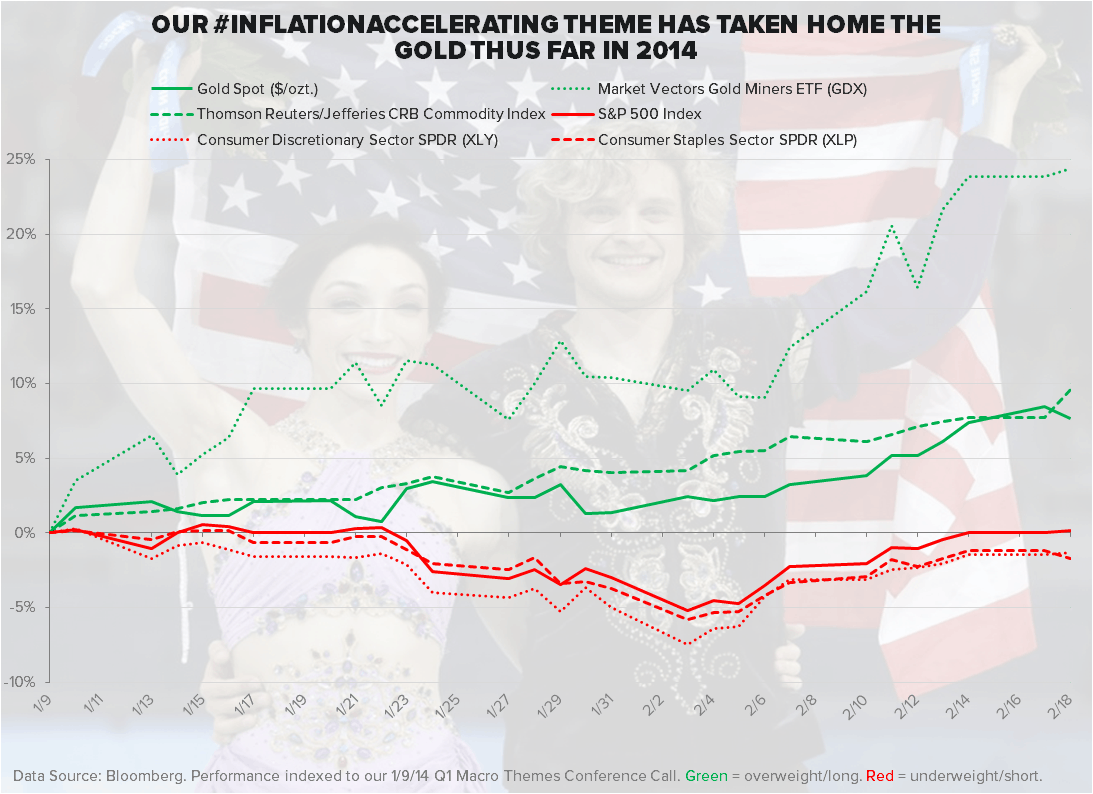

This morning in the Chart of the Day, I wanted to continue hitting on this ongoing paradox of reported versus actual inflation. As it relates to reported inflation, we do expect CPI to ramp and likely beat expectations in the U.S., but more importantly is the actual commodity inflation that is occurring. The chart shows Gold Spot, Gold Miners (GDX) and the CRB Index versus the SP500, Consumer Staples (XLY) and Consumer Discretionary (XLP).

As the chart emphasizes, commodity inflation has been on a tear since our January 9th Q1 Themes Call. Now, obviously, accelerating commodity inflation and input costs aren’t the reason that a number of our Best Ideas shorts, namely Weight Watchers (WTW) and Boardwalk Pipeline Partners (BWP), have underperformed so dramatically, but they are a reason that we continue to like the series of Best Idea shorts that our Restaurant team led by Howard Penney has added to the list.

This list of restaurant shorts includes Cheesecake Factory (CAKE), Bloomin’ Brands (BLMN), Potbelly Corporation (PBPB), and Panera Bread (PNRA). PNRA reported earnings least night and guided 2014 earnings estimates to $6.80 -> $7.05, which is below consensus estimates of $7.30. Certainly not a meaningful miss, and likely weather did play a part, but when a company trades at close to 25x forward earnings, expectations are, indeed, the root of all heartache. For more information on how to subscribe to restaurant sector research, please email .

Reverting back to inflation, the Congressional Budget Office released a recent report yesterday that had some rather interesting takeaways from President Obama’s proposal to raise the minimum wage (an inflationary pressure), specifically:

- President Obama's quest to raise the minimum wage to $10.10/hour would eliminate about 500,000 jobs by 2016 but also increase pay for 16.5M workers and lift 900K out of poverty;

- The report said benefits of an increase would be spread across a broad range of workers, with 19% of the increased wages going to Americans living below the poverty line. Close to 30% of the higher wages would go to people in families that earned more than three times the poverty level; and

- The report added that the increased cost of labor would encourage employers to upgrade technology or hire fewer, higher-skilled workers. That effect would be partially offset by higher earnings among low-wage workers who retained their jobs.

So, a proposed government policy that slows employment growth and creates inflation . . . that sounds eerily familiar.

This morning and through the duration of the week we will be getting a series of macro data points that will be critical to focus on, which include:

- Today - MBA Mortgage applications, PPI, Housing Starts and HSBC China Flash PMI.

- Thursday - CPI, Flash PMI, Eurozone Flash PMI and BOJ Minutes; and

- Friday - Existing home sales.

Paradoxically, the SP500 has been strong over the last two weeks or so, though it will be interesting to see how and if that strength sustains into an increased, and potentially negative, macro news flow. Conversely, as it relates to China, our view is fairly explicit. As my colleague Darius Dale emailed me this morning:

“Thus far in the YTD, the only data that has been supportive of a year-over-year acceleration in Chinese growth has been the credit data; even price-based leading indicators would suggest otherwise. All other data (i.e. PMI surveys) suggests sequential momentum is decidedly slowing. The market is clearly pricing in the expectation that the PBoC will have to ease [materially].”

Indeed.

Our immediate-term Macro Risk Ranges are now:

UST 10yr Yield 2.64-2.79%

SPX 1

VIX 11.79-15.93

Gold 1

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research