#Deceleration: Par for the 2014 Course

We profiled the deceleration in the Retail Sales data this morning - Here.

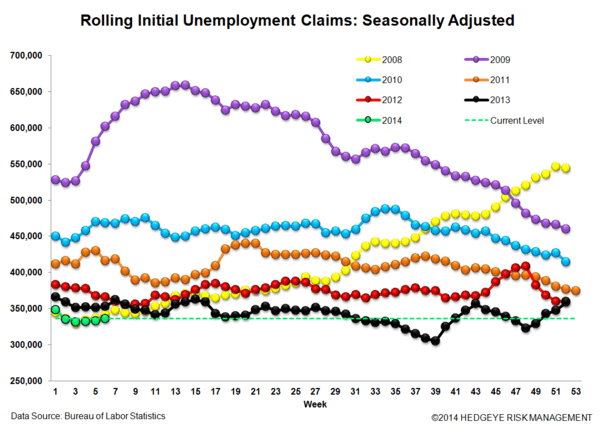

Inclusive of this week’s data, the trend in the high frequency labor market data is telling a similar story as seasonally-adjusted rolling claims rose again WoW and the rate of improvement in the rolling average of YoY non-seasonally adjusted claims decelerated 70bps to -5.0%.

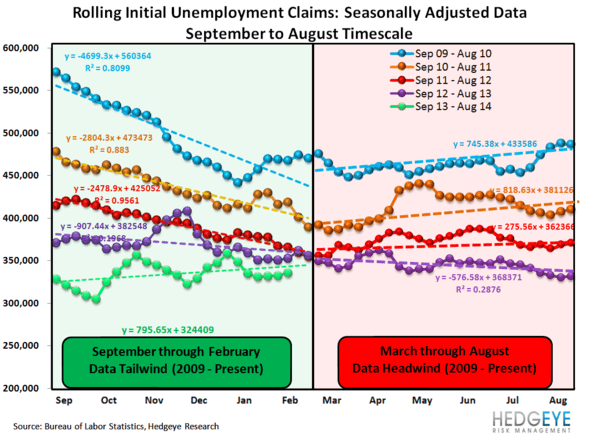

As we highlighted last week, its important to remember that initial claims can’t show “accelerating improvement” in perpetuity – the rate of improvement will inevitably converge towards zero as we approach the historical, frictional floor at ~300K in the seasonally adjusted series.

Its notable, however, that the claims data has deteriorated even as we’ve moved into the period of peak, positive seasonality. Any softness in the underlying trend will be (optically) exaggerated as seasonality again reverses into 2Q14.

Elsewhere, and on the constructive side, bloomberg’s weekly read on the consumer showed confidence ticking up 2.4 pts WoW to -30.7, the highest reading in a month. After a discrete breakout in 2013, confidence has been middling the last couple months with readings mixed mixed across the primary survey’s.

Dollar Down, Rates Down, Utilities leading and yield chase/inflation hedge assets (Gold/REITS/CRB) outperforming today….also par for the 2014 course.

Below is the detailed breakdown of this morning's claims data from the Hedgeye Financials led by Joshua Steiner. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

- Hedgeye Macro

--------------------------------------------------------------------------------------------------------------

INITIAL CLAIMS: The Labor Market Slows Further ...

Last week we profiled the labor market beginning to show modest signs of cooling off. This week's data marks a continuation of that trend. Our preference remains to look at the trend in the year-over-year rate of change in the rolling NSA initial jobless claims.

We look for signs of acceleration or deceleration and treat that as a referendum on the marginal strength of the economy. This week, that measure showed 5.0% y/y improvement. Here's how the last five weeks now look, ordered from oldest to most recent: -8.5%, -7.9%, -7.3%, -5.7%, -5.0%.

Clearly the trend over the past month has been one of a slowing rate of improvement. This doesn't mean that the economy isn't still progressing and jobs aren't still being added, but it does mean that the rate at which those things are happening is slowing down. Credit-sensitive financials should take note.

The Numbers

Prior to revision, initial jobless claims rose 8k to 339k from 331k WoW, as the prior week's number was revised down by 0k to 331k.

The headline (unrevised) number shows claims were higher by 8k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 3.5k WoW to 336k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -5.0% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -5.7%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT